Energy producers face the challenge of transitioning to cleaner, more sustainable energy production while still maximizing the shareholder value of their more traditional fossil-based energy sources. Canadian power producer TransAlta (NYSE:TAC) finds itself at a crossroads, with analysts and investors keeping a close eye on its next steps. While the shares trade at a relative value, investors might want to hold off and get a more complete picture of the company’s direction from the next quarter (or two) of earnings.

About TransAlta

TransAlta is an independent power producer based in Alberta, Canada. It operates a diverse portfolio of electrical power generation assets spread across Canada, the United States, and Australia. With a generation capacity of 6,761MW, it predominantly uses gas (3,084MW) and wind and solar (2,084MW).

Despite its geographic diversification, the company’s revenues are concentrated mainly in Alberta, making it susceptible to economic shifts within this region. Also, current market conditions on the spot price of gas (that result in declining electricity prices), as projected for 2024, are likely to negatively impact the company’s revenues and operating results.

Meanwhile, the company recently approved a 9% increase to its common share dividend, a sign that management believes in the strength of the company and its ability to generate profits moving forward.

TAC’s Recent Financial Performance

TransAlta finished Q4 with a lower net loss of C$0.27 per share compared to a loss per share of C$0.61 in the prior-year quarter. Also, the company reported adjusted EBITDA of C$289 million and free cash flow of C$121 million for Q4 2023.

The company finished 2023 with a free cash flow of C$890 million, or C$3.22 per share, from record-setting revenues of C$3.4 billion. This performance was accompanied by an adjusted EBITDA of C$1.63 billion, matching last year’s benchmark record. The net earnings provided to shareholders were also a record, at C$644 million, showing a substantial increase of C$640 million from 2022.

Looking forward, TransAlta Corporation estimates its 2024 adjusted EBITDA to be within the range of C$1.15 billion to C$1.3 billion. The free cash flow prediction is also substantial, ranging from C$450 million to C$600 million. The company has set strategic growth targets to enhance its fleet’s capacity by up to 1.75 GW. This will be achieved via an estimated investment of about C$3.5 billion, which will be used to develop, construct, or acquire new assets by the end of 2028.

Investors will look for EPS to turn positive again in Q1 2024 and watch to see if the company can carry over the strong revenue generation and margin into 2024.

What is the Price Target for TAC?

Despite solid results for 2023, TAC stock has been trending lower and is down roughly 20% over the past year. It currently trades at the low end of its 52-week range of $6.22-$10.40 and continues to show negative price momentum.

However, the price slide has pushed the stock into a relative value territory. The P/E ratio of 3.7x is well below the Utilities sector average of 19.4x and the Independent Power Producers industry average of 8.4x. Believing its shares are currently undervalued, management has implemented an automatic share purchase plan to back up to 14 million shares.

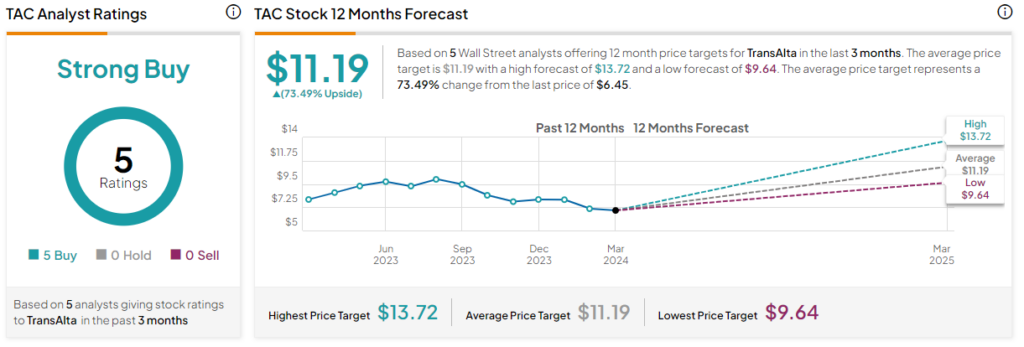

Analysts are bullish on TAC stock, and it is rated a Strong Buy based on five Wall Street analysts’ ratings issued over the past three months. The average price target for TAC stock is $11.19, representing 73.49% upside from current levels.

Final Thoughts on TAC

There are a number of things to like about TransAlta, including its strong performance last year, increasing dividend payout, and Wall Street’s bullish outlook. However, its undervaluation suggests there is something the market doesn’t like – such as the potential impact of fluctuating energy market conditions or the company’s geographic revenue concentration.

Investors might want to wait for a break in the negative price momentum and a more complete picture of TransAlta’s direction before making an investment decision.