PayPal shares are falling 3.9% in pre-market trading today as the company’s 4Q earnings outlook lagged analyst expectations.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The payment platform’s 3Q revenue surged 25% Y/Y to $5.46 billion as the pandemic fueled digital transactions across the world. Also, PayPal’s (PYPL) adjusted EPS increased by about 41% to $1.07 driven by 377 basis points Y/Y expansion in the adjusted operating margin to 27.2%. PayPal exceeded analysts’ revenue and EPS expectations of $5.43 billion and $0.94, respectively.

Meanwhile, the company added 15.2 million net new active accounts and ended the quarter with 361 million active accounts, marking a 22% growth. Total Payment Volume or TPV on the company’s platform increased 38% to $247 billion.

Following the strong 3Q numbers, PayPal raised its full year revenue growth guidance to the range of 20%–21% from the prior outlook of about 20% growth. Also, it now predicts adjusted EPS growth between 27%–28% compared to the previous forecast of about 25% growth.

For 4Q, the company anticipates revenue growth of 20%–25% and adjusted EPS increase of 17%–18%. Analysts were expecting adjusted EPS growth of about 24%. Speaking about the 4Q guidance on the conference call, the company highlighted the uncertainty related to COVID-19, the US presidential election and potential social unrest.

With regard to the 4Q guidance, BTIG analyst Mark Palmer noted, “PYPL’s guidance of 4Q20 adjusted EPS growth in a range of 17% to 18% was far below the 41% growth rate it reported in 3Q20, and it translates to an adjusted EPS range of $0.97 to $0.98 versus the consensus estimate of $1.07. Management said PYPL’s outlook was impacted in part by incremental investments during 4Q20.”

The analyst reiterated a Hold rating for PayPal saying, “Our non-consensus view on the stock is based on our belief that PYPL’s valuation already reflects much of the good news the company reported today and that questions about the sustainability of its growth trajectory in a post-pandemic world are likely to seep into discussions about the stock. As such, we would look for a better entry point before re-engaging with PYPL shares.” (See PYPL stock analysis on TipRanks)

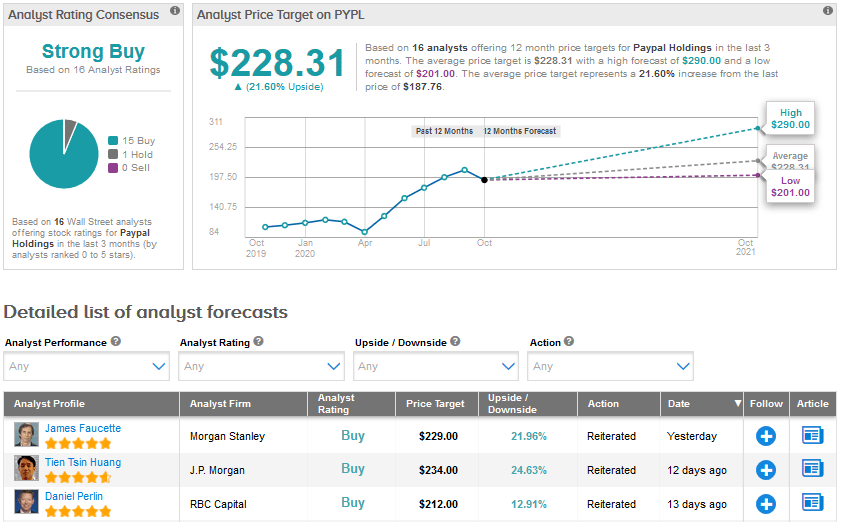

The Street is bullish about PayPal with a Strong Buy analyst consensus based on 15 Buys versus just one Hold. The average analyst price target of $228.31 indicates an upside potential of 21.6% in the coming months. Shares have risen by an impressive 73.7% year-to-date.

Related News:

Skyworks Sees Upbeat 2021 Guidance After A Blowout 4Q

Coupa Software Snaps Up LLamasoft For $1.5B; Analyst Sticks To Buy

Twitter’s Ad Revenues Drive 3Q Sales Beat