Nvidia posted a record sales quarter fueled by a surge in online gaming and as the work-from-home shift spurred demand for the chip company’s semiconductors.

Despite the blowout quarterly performance, the stock dropped 2.2% in Wednesday’s after-market trading after Nvidia’s (NVDA) chief financial officer Colette Kress told investors data center sales are expected to grow in the “low-to-mid single digit” percentage range in the fiscal third quarter, versus the previous quarter.

Total revenue in the second quarter rose 50% to $3.87 billion year-on-year, beating analysts’ estimates of $3.65 billion. Gaming revenue grew 26% to $1.65 billion ahead of expectations of $1.41 billion. The chip company’s data center revenue jumped 167% in the three months ended July 26 to $1.75 billion exceeding estimates of $1.71 billion.

On an adjusted basis, Nvidia earned $2.18 per share in the reported quarter surpassing the consensus of $1.97 per share.

“Adoption of NVIDIA computing is accelerating, driving record revenue and exceptional growth. Growth in GeForce gaming accelerated as gamers increasingly immerse themselves in realistic virtual worlds created by NVIDIA RTX ray tracing and AI,” said Nvidia CEO Jensen Huang. ““Despite the pandemic’s impact on our professional visualization and automotive platforms, we are well positioned to grow, as gaming, AI, cloud computing and autonomous machines drive the next industrial revolution around the world.”

Looking ahead, the US chip company guided investors with third-quarter revenue of $4.40 billion, compared with analysts’ expectations of $3.97 billion.

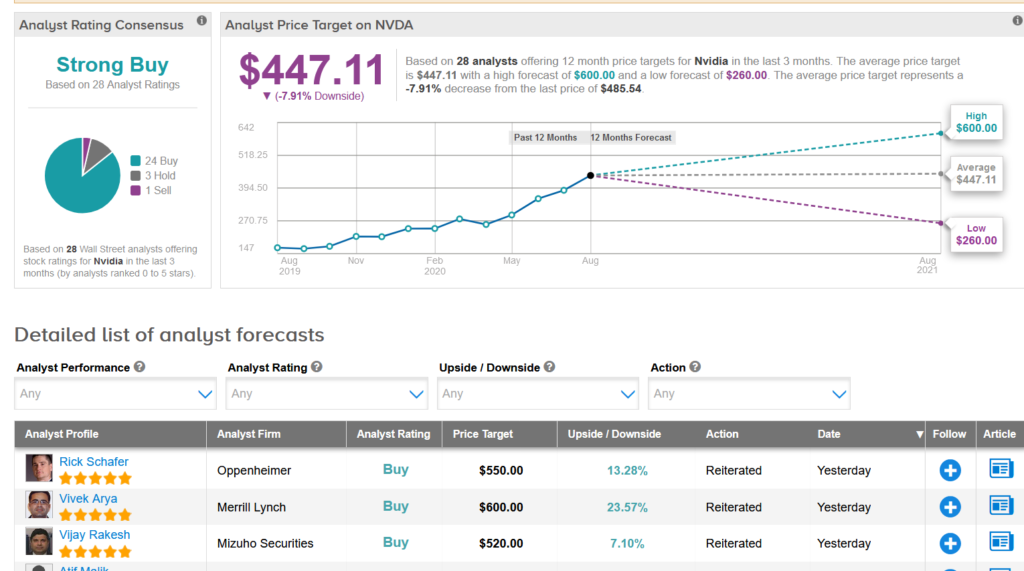

Shares in Nvidia have been on a winning streak this year soaring a stellar 107% so far this year. Nonetheless, Oppenheimer analyst Rick Schafer ramped up NVDA’s price target to $550 (13% upside potential) from $500 saying that several sustained tailwinds driving outsized top-line growth justify the stock’s “premium valuation”. (See Nvidia stock analysis on TipRanks).

“Gaming is poised for an exceptional 2H. Net, structural growth drivers appear intact, and we see room for additional capital deployment,” Schafer wrote in a note to investors following the financial results. “We remain LT [long-time] buyers.”

The analyst added that “NVDA trades 40x (ex-cash) our CY22E EPS, in line with its 3-year historical trading range.

Nvidia has strong backing from the rest of the Street, too. The stock boasts 24 Buys versus 3 Holds and 1 Sell adding up to a Strong Buy analyst consensus. In view of this year’s big rally, the $447.11 average price target implies about 8% downside potential to current levels.

Related News:

Intel’s New Transistor Technology To Boost Chip Performance By 20%

Facebook Barks At Apple For Refusing to Waive 30% Fee On New Tool

Susquehanna Lifts Nvidia’s PT To ‘Street High’ Ahead of Tomorrow’s 2Q Results