The tech landscape has always been fast-changing, particularly in the digital world. It was 18 months ago that OpenAI launched ChatGPT, igniting our current wave of interest in generative AI – and tech firms of all types are rapidly shifting to use or adapt this shiny new thing.

The fast pace of digital changes is bringing new opportunities for investors, in the form of AI stocks and their adjuncts, but it’s also revitalizing older opportunities, such as the chip stocks, as they adapt to serve the AI expansion.

Covering the chip sector, Cantor Fitzgerald’s C.J. Muse, a 5-star analyst rated in the top 2% of the Street’s stock pros, sums up the current situation: “AI spending continues to crowd out other investments, and we continue to see a broadening of spend from CSPs to Sovereigns to Enterprises – certainly faster than expected 3-6mos ago. And as each iteration of acceleration technology results in increasing efficiencies and cost improvements, Jevons Paradox is clearly at play, driving a virtually insatiable demand for compute as we remain in the very early innings of this paradigm shift. So performance over the past few months may cause some to ask if the easy money has been made? And perhaps it has. But there is still plenty of room to go from here – with upside across numerous areas of the Semiconductor landscape.”

This provides firm support for the chip industry and sets the stage for plenty of investor interest. However, not all chip stocks are created equal, and some offer better opportunities than others. Against this backdrop, Muse has evaluated two of the largest chip stocks, Nvidia (NASDAQ:NVDA) and Intel (NASDAQ:INTC), and outlines which is the superior chip stock to buy ahead of their next earnings releases in the coming weeks. Let’s take a closer look.

Nvidia

First up, Nvidia has in the past year become the 800-pound gorilla of the chip sector. The company’s meteoric rise has been fueled by its powerful lead in supplying AI-capable processor chips, and the firm is now the world’s largest semiconductor maker when measured by market cap. Nvidia boasts a market cap of $2.10 trillion, making it not just the largest chip company, but also the third-largest publicly traded firm globally, and one of just six companies on Wall Street trading in the trillion-dollar-plus range.

As noted, Nvidia has powered its growth through its domination of high-capacity processor chips. The firm has always had a hand in this pot, as it was one of the early developers of the graphics processing units, the GPUs that are so essential for data center and AI use today. These chips were originally designed to meet the needs of hardcore gamers in their demand for ever-better graphics; GPUs were quickly adopted by professional graphics designers and web developers, and later, their high processing speeds and computing capacities made them the perfect fit for data centers and AI applications. Even before it released ChatGPT, OpenAI depended on Nvidia for its high-end semiconductors.

Nvidia is expected to release its financial results for fiscal 1Q25 toward the end of next month, and analysts are expected to see revenues of approximately $24.25 billion and earnings of $5.50 per share. Looking back at the last release, from fiscal 4Q24, will give some additional perspective.

In that last quarter, Nvidia had a top line of $22.1 billion, growing revenues an impressive 265% year-over-year and reaching a company record – and beating the forecast by $1.55 billion. $18.4 billion of the revenue total came from the company’s data center business, representing segment growth of 409% y/y, and comprising 83% of the total quarterly revenues.

On earnings, Nvidia reported a non-GAAP EPS of $5.16 in fiscal Q4, a figure that was up 28% from the previous quarter, 486% from the previous year, and was 52 cents per share ahead of the estimates. The company reported full-year fiscal 2024 revenues of $60.9 billion.

Cantor’s Muse has been duly impressed by Nvidia, and attributes the company’s success to its solid AI-related business. The top-rated analyst writes, “AI momentum remains strong and should drive another solid beat and raise. Adding on to the increasing breadth of AI applications and adoption, NVDA will benefit from the Blackwell product launch into 4Q24, which should drive revenue acceleration through 2025 – supportive of EPS tracking to $30-35. Trading at 29x the low-end of this range today, NVDA offers attractive valuation for THE key enabler and driver of all AI. Remains a clear top pick and expect earnings to act as a catalyst in the continued push higher.”

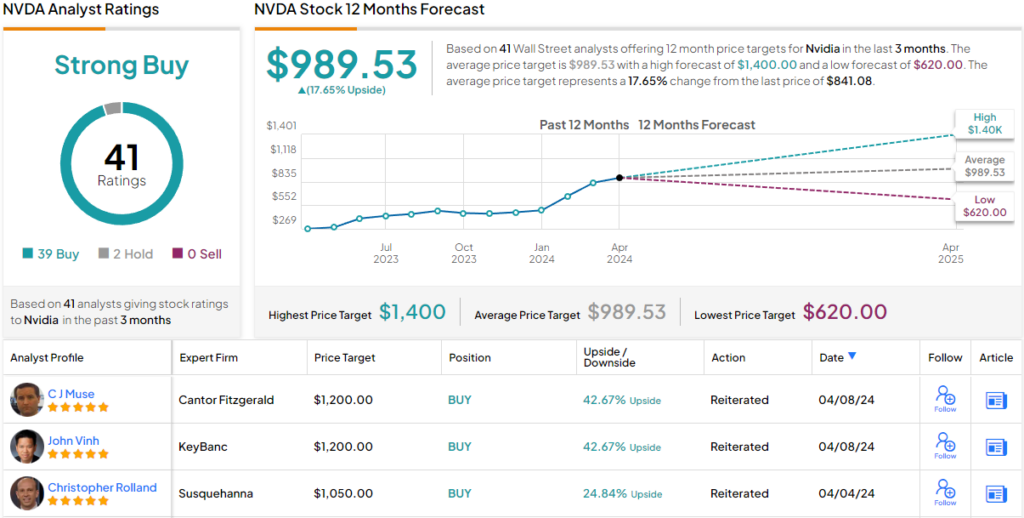

Quantifying his bullish stance, Muse puts an Overweight (i.e. Buy) rating on Nvidia’s stock, with a $1,200 price target that points toward a one-year gain of 43%. (To watch Muse’s track record, click here)

Overall, this AI leader has picked up 41 recent analyst reviews, and these show a highly lopsided split of 39 Buys to 2 Holds – for a Strong Buy consensus rating. The shares are trading for $843.14 and their average target price of $989.53 suggests ~18% one-year upside potential. (See NVDA stock forecast)

Intel

Now we’ll shift our gaze to Intel, another giant of the chip industry. Intel rose to prominence in the last decade as a leading supplier of CPU chips for the personal computer market, a niche that made it the industry’s leading chip maker in the 2010s. In fact, Intel still holds a leading market share, of approximately 63%, in the CPU niche, and has a market cap that exceeds $163 billion.

While Intel faced some delays in the development of AI-capable chips, it has recently introduced innovative product lines, including the fifth-generation Xeon server chips and the Gaudi3 processor. These products were designed to meet the needs of data centers and generative AI applications.

In the meantime, Intel has not abandoned its core competency, and the base of its success. The company is also releasing new models in its line of Core processors, the iCore chips that power so many of our desktop and laptop computers. And, in a move that bodes well for the mid-term, Intel stands to receive a large tranche of funds – as much as $8.5 billion – in Federal disbursements under the CHIPS Act, and will be able to access some $11 billion in Federally funded loans. Intel has already indicated that the Federal funding will support the company’s new chip factory planned in New Mexico.

Intel last reported earnings for 4Q23, and in that quarter, the company brought in revenues of $15.4 billion. This was $230 million better than the forecast and was up 10% year-over-year. Intel’s earnings in 4Q23, reported as a non-GAAP EPS, were 54 cents per share, 9 cents better than had been anticipated.

The company has guided toward revenue between $12.2 billion and $13.2 billion for 1Q24, which is scheduled to be reported on April 25.

Cantor’s Muse acknowledges that Intel has some strengths, but believes that they are somewhat overrated for now.

“While we do expect Intel management to reiterate continued excitement about a 2H24 rebound, we also think consensus estimates are too high for 2Q24. Normal seasonality is flat to down Q/Q, but we think Intel will guide revenues likely +3-4% Q/Q. Unfortunately, consensus is +7% Q/Q. Thus, we look for a modest beat followed by a modest miss. For the 2H, we look for a reiteration of reacceleration for both PC and Server revenues. For PCs, think units +LSD% combined with EOL Win10 driving greater mix of Enterprise, which carries 10-15% higher ASP vs. Client. In Data Center, we should see return to unit growth (think LSD% for Servers in CY24) and benefit of Higher Core Count (think +15-20%) which when partially offset by lower ASP could deliver DC growth of HSD-LDD% (though we would view this as the upside case today). Despite the sell off following Intel’s resegmentation presentation, we still view a challenged set-up.”

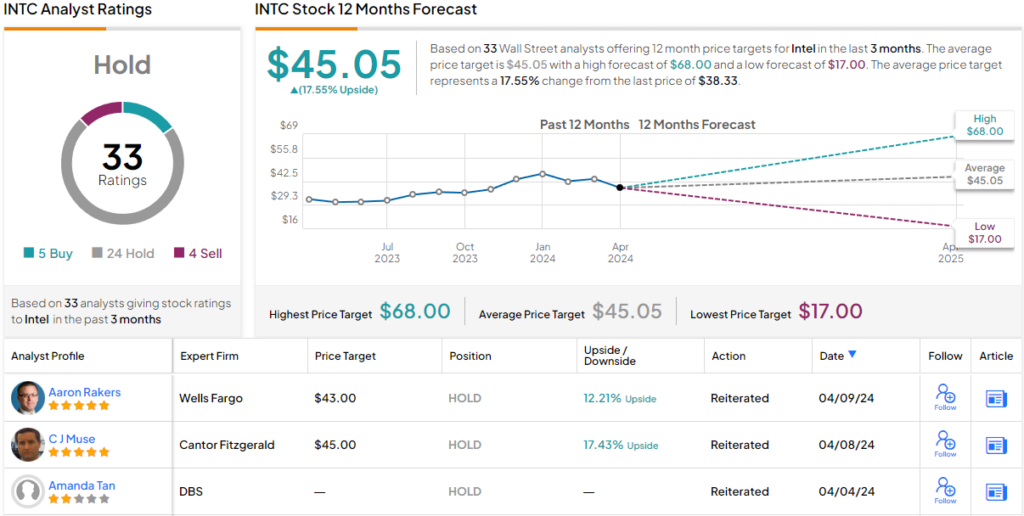

While Muse does not advise selling off INTC shares, he does put a Neutral rating on the stock. His price target, of $45, implies an upside of 17% on the one-year horizon.

Muse’s views are mainly in-line with the Street’s take on Intel. The stock has a Hold consensus rating, based on 33 analyst reviews that include 5 Buys, 24 Holds, and 4 Sells. The stock’s average price target of $45.05 basically matches Muse’s view, of ~17% upside from the current trading price of $38.33. (See INTC stock forecast)

And now it’s clear that Cantor’s top analyst picks Nvidia as the best chip stock to buy, a true leader in a crowded lane.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.