Every savvy investor seeks out the golden opportunities within the market. One effective strategy involves investing in an essential commodity or product, something that the economy cannot do without. It’s a common-sense way to find companies that are sure to generate steady revenues.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

In today’s world, few products are more essential than the silicon semiconductor chip. Found in everything from wristwatches to smartphones and tablets to automobiles to jet airliners, these chips make almost all modern technology possible.

The surge in generative AI technology that has powered the tech industry’s gain in recent months rides on the back of high-end, high-capacity processor chips. That surge has also been helped along by government policy. The Biden Administration pushed hard for the CHIPS Act, to subsidize reshoring of the US semiconductor industry, and the first tranche of that money hit the chip scene at the end of last year.

This gives firm support to the chip industry, and sets the table for plenty of investor interest. But not all chip stocks are created equal, and some offer better opportunities than others. This is where Goldman Sachs comes into play.

The investing giant has taken the measure of the largest chip stocks, and lays out just which ones are right to buy. Nvidia (NASDAQ:NVDA) and Intel (NASDAQ:INTC), in particular, have caught Goldman’s interest, and for good reason. Nvidia, one of the Magnificent 7 tech leaders, is one of the half-dozen trillion-dollar-plus companies on Wall Street and holds the title of the world’s largest chip maker by market cap. Intel, with a smaller market cap, still maintains its position in the top ten of the chip space and has long been a leader in the field.

So, let’s delve into Goldman’s insights to determine which chip stock emerges as the top pick for investment.

Nvidia

We’ll start with Nvidia. This company, as noted, has in recent years reached the top rungs of the trading world – and a market cap valuation of $1.78 trillion. This makes the chip maker the fifth-largest publicly traded firm on Wall Street.

Nvidia reached these heights on the back of a massive surge in share value over the past year or more. Some numbers will paint the picture: in the last 3 years, Nvidia’s stock is up almost 400%. The 12-month gain is 215%; in just the first few weeks of 2024, NVDA has continued to gain, tacking on another 45%.

The company’s huge rise in share price has been accompanied by similar gains in revenues and earnings. Nvidia has seen huge success, especially in its GPUs. These high-performance chips were originally designed to meet the demands of online gamers for better graphics, but the chips themselves quickly found other applications and are also in high demand by professional graphic designers, AI developers, and especially the data center industry.

That last part has been a bright spot for Nvidia’s business, and the company boasts a market share of approximately 70% in that industry. Supplying chips to the data center sector accounted for as much as 80% of Nvidia’s business in its last reported quarter, 3Q23, and reached a total of $14.51 billion in revenue. That marked a 279% year-over-year increase for Nvidia’s data center sales.

Nvidia had other solid successes in that quarter – notably among gamers and automotive developers – and saw total revenues of $18.12 billion, setting a company record, a 206% year-over-year increase, and a $2 billion beat of the forecast. Nvidia’s Q3 bottom line came to $4.02 per share by non-GAAP measures, a figure that was 63 cents per share better than had been expected.

Looking ahead, Wall Street expects to see Nvidia’s top line at or near $20.27 billion when it reports 4Q23 results later this month, with a non-GAAP EPS of $4.53. Nvidia has been showing sequential gains at both the top and bottom lines since 4Q23.

Turning to Goldman’s view on this dominant chip company, we find 5-star analyst Toshiya Hari, recognized among the top 1% of Wall Street analysts by TipRanks. Hari presents compelling arguments for investors to take a bullish stance on Nvidia.

Highlighting the resilience of the data center segment, Hari notes, “Based on recent conversations, most investors appear to have a good sense as to what Nvidia could earn in CY2024 and are rather focused on the trajectory of the Data Center business into CY2025. While we model 14% yoy growth in Data Center revenue in CY2025 as our central case, we acknowledge that forecasting revenue beyond the current year for such a nascent and dynamic business is challenging.”

The analyst goes on to explain just why this stock, despite its high price, makes a good value for buyers: “For this reason, we believe solving for potential upside or downside to the stock under various scenarios is an effective way to gauge NVDA’s current risk/reward profile… Our analysis indicates attractive risk/reward with the most bullish and bearish cases pointing to 119% potential upside and 60% potential downside, respectively.”

For Hari, all of this supports a Buy rating on NVDA stock. His price target, set at $800, suggests that the chipmaker will gain another 11% in the coming year. (To watch Hari’s track record, click here)

Overall, Nvidia has a Strong Buy rating from the analyst consensus, based on 38 recent recommendations that include 34 Buys to just 4 Holds. However, the shares are currently trading for $721.33, and their recent surge in value has pushed that price above the average target price of $684.84, implying a 5% downside in the next 12 months. It’ll be interesting to see if the analysts tweak their targets after Nvidia’s earnings report. (See Nvidia stock forecast)

Intel Corporation (INTC)

Intel, the second chip maker that Goldman is looking at, is a perennial member of the industry’s ‘top ten,’ but just a few years ago, it held the number one spot. Developments in recent years, however, have been hard on Intel, and knocked it off that throne. The company’s size – it still has a market cap of $180 billion – has provided some insulation, as has its reputation for quality and its strong presence in the PC segment. Intel’s particular strength is its dominance of the PC processor market.

But AI is the wave of the future, especially for semiconductor chip makers, and Intel simply did not have an AI-capable chip on the market in 2022 or 2023. The company lost ground and faces a challenge in recouping some of those losses.

A look at Intel’s last earnings release, covering Q4 and full year 2023, shows some of the problems – and paradoxes. The company beat the forecasts on revenue and earnings for the quarter. Q4 revenue came to $15.4 billion, up 10% year-over-year and beating the estimates by $230 million. The bottom line, a non-GAAP earnings-per-share of 54 cents, was 9 cents better than had been expected. But for the full year, the revenue total of $54.2 billion was down 14% from 2022, and the non-GAAP full-year EPS of $1.05 was down 37% from the $1.67 reported for 2022.

The real problem, however, came from Intel’s guidance numbers. Intel provided Q1 revenue guidance in the range between $12.2 billion and $13.2 billion, where analysts had hoped to see a prediction of $14.25 billion.

Intel is following several paths to regain a leading position among chip makers. The company is working on new AI-capable chips, in an effort to expand beyond the base of its legacy PC business; however successful, that base cannot fold the company up forever. New chips include the Core Ultra in the Windows PC and laptop segment, but also the fifth-gen Xeon server chips and the Gaudi3, which was designed to power generative AI software.

In addition, Intel has been pushing hard to tap into the CHIPS Act largesse as part of a general expansion in manufacturing capabilities. The company last month announced the opening of its Fab 9 chip factory in New Mexico, a cutting-edge facility for the manufacture of advanced semiconductor technologies. Also, Intel has entered into an agreement with UMC, a leading global foundry, for the design and manufacture of a 12-nanometer semiconductor process platform.

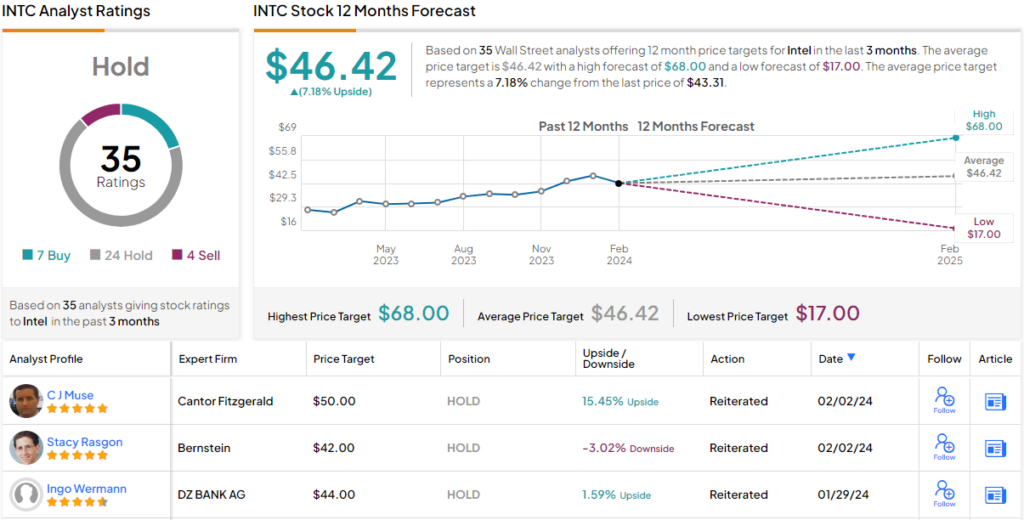

Turning again to Toshiya Hari, to get the Goldman Sachs view of Intel, we find the top-ranked analyst taking an upbeat view of Intel’s recent moves to boost its business. However, he remains cautious on the stock, and is not recommending a purchase.

“While we are encouraged by the various strategic actions taken by management over the past 12-18 months and believe increased clarity on CHIPS Act funding could boost sentiment on the stock in the near-term, we maintain our Sell rating on INTC and continue to await signs of share stabilization in Data Center Compute and/or material progress in its external Foundry strategy,” Hari opined.

Getting to his own bottom line here, Hari writes, “Similar to last year, we expect the large cloud hyperscale customers to prioritize capital spending on accelerated compute (vs. general-purpose compute) in 2024, and for market share within general-purpose compute (or traditional servers) to shift in favor of AMD and Arm-based custom processors (e.g. AWS Graviton).”

The Goldman Sachs Sell rating comes with a $39 price target that points toward a one-year downside potential of 10%.

Ultimately, the word on the Street points to a sidelined majority on Intel. In the last three months, the chip maker has landed 7 ‘buy’ ratings, 24 ‘holds’ and 4 ‘sells.’ That said, the consensus average price target points to $46.42, or nearly 7% upside potential for the stock. (See Intel’s stock forecast)

The verdict is clear: Goldman Sachs has come down in favor of Nvidia as the right chip stock for investors to buy now.

To find good ideas for AI stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.