The ‘Magnificent 7’ stocks, the seven mega-cap tech firms that have dominated headlines and market gains for the better part of the last 15 months, are still making waves. These companies – Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla – ran significantly hotter than the overall markets last year, but there are questions now as to whether investors should continue buying in, or start looking elsewhere.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The basic fact is that these tech stocks, while all leaders in the broader tech field, are not created equal. The companies do different things, and come from different angles, and they will react to changing conditions with different share performance results. For investors, this means that some due diligence is in order.

Wells Fargo’s stock analysts have kickstarted that process by conducting an extensive analysis of both Microsoft (NASDAQ:MSFT) and Tesla (NASDAQ:TSLA), and they’ve chosen one as still being truly ‘Magnificent.’ Let’s take a closer look.

Microsoft

We’ll start with Microsoft, one of the computing world’s iconic brands. Microsoft recently broke above the $3-trillion market cap figure, it is valued at $3.1 trillion now, making it the world’s most valuable publicly traded company.

While its software is the base of its success, Microsoft has not rested on that one segment. The company is branching out, expanding its work field to take advantage of new openings in the larger computing industry, and to ensure that the Microsoft name retains its leading position. In particular, the company is moving into AI.

We all remember how generative AI burst onto the scene in November 2022 when OpenAI released ChatGPT. What is hardly a secret is that Microsoft was an early backer of OpenAI, with a multi-billion dollar investment deal in the smaller company. Microsoft’s investment in AI is paying dividends; the company is integrating OpenAI’s generative technology into its Bing search engine and has recently launched an AI-powered online assistance program called Copilot for Windows and Office.

In addition to its AI integrations, Microsoft also has a heavy presence in cloud computing. The company’s Azure platform competes with the likes of AWS and Google Cloud, and offers users more than 200 software products. Subscribers can pick and choose from those them, to find the exact software tools they need for the job at hand. The Azure cloud service has a rapidly growing audience and is one of Microsoft’s more important revenue drivers.

How important a revenue driver is Azure? Well, in Microsoft’s last quarterly release, for fiscal 2Q24, the company’s Intelligent Cloud, which includes Azure, saw revenues jump 20% year-over-year to reach $25.9 billion. This was almost 42% of the company’s total revenue, which was reported at $62 billion. That total revenue figure was up 18% from the prior-year period, and came in $890 million above expectations. At the bottom line, Microsoft saw earnings of $2.93 per share, 16 cents per share over the forecast.

In his coverage of Microsoft for Wells Fargo, analyst Michael Turrin is careful to note the company’s recent rapid growth, and its strong AI presence, as a solid foundation.

“Upon closer examination of FQ2 results and review of upcoming price increases, we see further incremental tailwinds forming that should benefit both 2H24 & FY25 growth as MSFT aims to capitalize on its early lead in AI… MSFT grew fastest among the hyperscalers for the 2nd straight qtr in 2Q, increasing its market share to 34% (from 30% in Mar’21) & AI now at least $3.3B run rate (~5% of total). Though not updating its Azure outlook for 4Q, we expect 4Q results remain stable or accelerate from 3Q levels, given greater-than-expected AI contributions and easing compares heading into FQ4 (3Q comps ease by 7 points, 4Q by another 4 points),” Turrin wrote.

Turrin goes on to point out some reasons why investors should expect that MSFT will continue to grow, saying, “While we expect duration is benefiting overall bookings activity (similar to rest of enterprise software), a closer look at the underlying bookings trends for MSFT suggests that 1) trend lines continue to improve and 2) easing compares, a larger expiry base, & an AI-led purchasing cycle in upcoming 2H is likely to result in ‘healthy’ (mid-teens or greater) growth in 3Q/4Q commercial bookings – in turn benefiting FY25 visibility/growth prospects.”

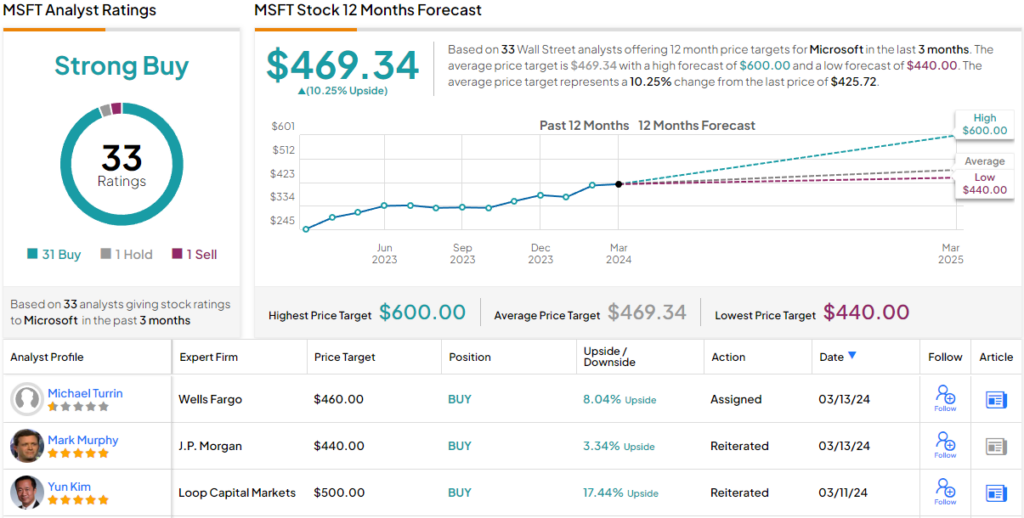

These comments support the analyst’s Overweight (i.e. Buy) rating on this stock, along with a $460 price target that suggests an 8% share appreciation from current levels. (To watch Turrin’s track record, click here)

Overall, the 33 recent analyst reviews of Microsoft shares show a lopsided split of 31 Buys, 1 Hold, and 1 Sell, for a Strong Buy consensus rating. The stock does not run cheap; it is priced at $426 and its $469.34 average target price implies that a 10% gain is in store this year. (See Microsoft stock forecast)

Tesla

Next up, we’ll look at Tesla. This is, arguably, the world’s leading firm in the electric vehicle market, and it was the first automaker in decades to move from concept to large-scale, profitable, global production and distribution – pushed there by the controversial visions of billionaire entrepreneur Elon Musk. Tesla’s success has been the stuff of legend; the company was founded in 2003, and has already become the world’s largest automotive firm by market cap, with a valuation of $520 billion.

The company has built its success on a simple, basic premise – high-tech factories turning out high-quality vehicles that customers enjoy driving. It doesn’t matter if the vehicles in question have combustion engines or electric motor drive trains; an automotive company must clear that bar if it is to succeed. Musk has insisted on that formula, and is reaping the rewards.

That doesn’t mean that Tesla has had clear sailing. The company is facing headwinds in the form of slowing demand, and even after price cuts, its cars remain expensive. Musk has already admitted that Tesla is setting its pricing based on customer demand for vehicles – which means that the price cuts which have cut into Tesla’s margins may indicate that demand is softer than management wants to admit.

For now, the company’s production and delivery numbers are strong. Tesla reported 495,000 vehicles built in 4Q23, the last period reported, along with 484,000 vehicles delivered to customers. For all of 2023, those numbers came to 1.85 million and 1.81 million. These 2023 numbers were a marked increase from 2022, with production up 35% year-over-year and deliveries up by 38%.

Despite these increases in its base business, Tesla’s Q4 revenue and earnings both missed expectations. In the final quarter of 2023, Tesla reported a top line of $25.17 billion, a figure that was up 3% from the prior year but was also $590 million below the forecast. The company’s bottom line was a non-GAAP EPS of $0.71 per share; this was down 40% year-over-year and was 3 cents less than had been anticipated.

Wells Fargo analyst Colin Langan sees plenty of caution signs here, and doesn’t hesitate to say so. In his coverage of Tesla, he notes that the company’s growth is slowing, on signs of softening demand.

“We have an Underweight rating on TSLA. We see moderating delivery growth driven by lower demand & diminished return on price cuts. We are cautious on margins given likelihood of more price cuts & lower volumes. Moreover, we are concerned about Model 2 demand & margins. We also see risks around increased US regulation on Autopilot & risk to the rollout of previously promised technologies (Dojo, Optimus, true FSD, etc)… While an EV & battery tech leader, TSLA screens poorly relative to Mag 7 peers, trading at 58x PE vs. peers at 31x.”

Langan’s Underweight (i.e. Sell) rating is accompanied by a price target of $125, showing the analyst’s belief that the shares will depreciate by 23% in the year ahead. (To watch Langan’s track record, click here)

Wall Street, generally, has a Hold (i.e. Neutral) consensus rating on TSLA, based on 35 recent reviews that include 10 Buys, 18 Holds, and 7 Sells. Tesla shares are priced at $162.88, and their average target price of $205.22 implies a one-year upside potential of ~26%. (See TSLA stock forecast)

What it comes down to is simple – the stock pros at Wells Fargo have soured on Tesla, but are all-in on Microsoft, which in their view is still a ‘Magnificent’ stock.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.