Truly game-changing technologies seem to appear once every couple of decades. The personal computer appeared on the scene in the early ’80s, and the internet came into its own in the late ’90s. And now, AI is all the rage.

AI technology has taken the digital world by storm, finding its way into applications as varied as automation systems, marketing, and language translations. The introduction of generative AI at the end of 2022, with its potential to forever alter the way we interact with machines, has added another application as well as the promise of more intuitive use. In short, AI is this generation’s shiny thing.

The tech is here to stay, and that’s opening up opportunities for investors. Analyst Brent Thill, from Jefferies, has dipped into the workings of the AI sector, and tagged several big-name tech firms as long-term winners.

Outlining his criteria, Thill writes, “Investments centered on the ‘picks and shovels’ of AI have continued to outperform… We believe AI spend will spread to other infrastructure providers and to app vendors that enable enterprises to take advantage of Gen AI. Our AI KIS basket represents the companies we see capturing the most of this transformational opportunity. We advocate for investors to position themselves before enterprise adoption ramps in late ’24 into ‘25, providing a better line of sight to rev uplift.”

Thill’s choices include some of the Magnificent 7 mega-cap tech stocks, firms that are already deeply connected to the AI expansion: Microsoft (NASDAQ:MSFT), Alphabet (NASDAQ:GOOGL), and Meta Platforms (NASDAQ:META). Let’s take a closer look at these big names, and at Thill’s comments on them.

Microsoft

We’ll start with the stock that Thill describes as the ‘Top AI Winner,’ Microsoft. We all know this company; Microsoft’s particular combination of popular products and sound management has brought it to the pinnacle of the tech world – and in some ways, of the economy generally. The company is currently the highest-valued publicly traded firm on Wall Street, with a market cap exceeding $3 trillion.

The key point for this discussion, however, is Microsoft’s deep involvement with AI. The company is a long-time backer of OpenAI, the developer of the ChatGPT chatbot that launched the current wave of generative AI technology. Microsoft has been a backer of OpenAI since 2019, and earlier this year invested an additional $10 billion in the company. We should note here that ChatGPT has, in recent months, seen a strong gain in usage; a survey from Pew showed that 23% of US adults had used the bot in some way, marking a jump from 18% seven months prior.

In backing OpenAI, it’s not just that Microsoft has chosen a winning horse; Microsoft has also gained access to the AI chatbot technology, which it is integrating into its Bing search engine, and into its Windows operating system and Office software. In recent software updates, Microsoft has released an AI-based online assistant, Copilot, to provide real-time user assistance in Windows.

In a move that is likely more important for users, Microsoft’s integration of AI into its Azure cloud platform is notable. Azure already offers subscribers over 200 software tools and products to meet almost any online need. Adding AI into the mix will add value to the product and increase its ability to compete with peers like AWS and Google Cloud. Azure already generates $25.9 billion in quarterly revenue, as of Microsoft’s fiscal 2Q24 report.

That report showed a total top line of $62 billion, a figure that was up 18% year-over-year and came in $890 million better than anticipated. The company’s bottom line was an EPS of $2.93, 16 cents per share ahead of the forecast.

For Thill, Microsoft’s full embrace of AI is a key point, one that make the stock attractive for investors.

“We believe MSFT, due to its partnership with OpenAI, has positioned itself as a key beneficiary of Gen AI. While we are in the early innings of AI adoption, we continue to be bullish on MSFT’s Copilots’ ability to drive rev uplift in CY24 and beyond. We highlight that enterprise interest continues to build with a majority of MSFT’s Copilots generally available today. We suspect Azure’s AI contribution will grow tangibly in CY24 as companies put more models & tools into production, continuing to support Azure’s growth and market share gains. Further, we believe AI products, due to their strong pricing power, will be accretive to margins overtime,” Thill opined.

Unsurprisingly, Thill rates MSFT stock as a Buy, and his $550 price target implies a one-year upside potential of 30%. (To watch Thill’s track record, click here)

Big Tech always attracts the Street’s analysts, and MSFT has 35 recent reviews on record, including 33 Buys, 1 Hold, and 1 Sell – all for a Strong Buy consensus rating. The shares are priced at $421.44 and their $471.71 average price target indicates a potential gain of 12% in the year ahead. (See MSFT stock forecast)

Alphabet

The next stock we’ll look at is Alphabet, best known as the parent company of Google – and the firm that Thill describes as the ‘most underrated’ AI stock play. Like Microsoft, Alphabet is a trillion-dollar mega-cap company, with a market cap of $1.9 trillion making it the world’s fourth-largest publicly traded company.

While Alphabet has built itself up through its successful development of internet search and the consequent monetization derived from that niche, the company is not ignoring recent developments in AI. Alphabet’s other subsidiaries include an autonomous vehicle venture, Waymo, that is heavily dependent on AI technology to control its self-driving cars – which have already appeared on the streets of San Francisco. Alphabet is also using AI in the creation of the Large Language Modules on Google Cloud; these are an online translation service, and use both AI and natural language processing to deliver clear text translations and facilitate writing new texts in multiple languages.

Of particular interest to investors, the company is also integrating AI into the Google search engine, introducing the Performance Max tools – that use generative AI tech – into the search engine’s ad campaign functionality. This has the potential to enhance returns on Google ad campaigns, increasing the profit per dollar spent.

The company’s AI moves have not all gathered laurels. Alphabet recently rebranded its Bard chatbot as Gemini – and picked up headlines for all the wrong reasons. The generative AI chatbot delivered amusing wrong misinterpretations of its users’ requests, and seemed completely unable to generate images of white people.

That was a serious glitch, but it is fixable, and Alphabet has been quick to move on the fixes – and while AI is the future, for now Alphabet’s main revenue driver is Google, which was not harmed by the setback.

In quantitative terms, Alphabet can rest on solid revenues, $86.3 billion in the fourth quarter of 2023, up 13% year-over-year and more than $1 billion better than had been expected. The company saw solid earnings in Q4 too, at $1.64 per share in GAAP measures, beating the forecast by 4 cents.

Analyst Thill recognizes Alphabet’s strong position in online search as a cornerstone for the company’s future, particularly as it embraces generative AI technology. He writes of the stock, “We believe GOOGL is a leader in AI/ML technology and is best-positioned to benefit from the consumer opportunity by introducing Gen AI to its billions of users. Though Gen AI is perceived to impact traditional search, we believe GOOGL will continue its dominance, already adapting to this shift with its new search generative experience (SGE). Further, GOOGL’s Performance Max AI targeting tool is already boosting advertising ROI, especially for SMBs, and should help produce operating leverage going forward. While GCP is still a distant 3rd in Public Cloud, we believe that Gen AI gives GOOGL an opportunity to close the gap.”

These comments back up Thill’s Buy rating on GOOGL, and his $175 price target points toward a one-year upside of 13%.

Overall, GOOGL’s Strong Buy analyst consensus rating is based on 37 recent reviews that break down to 27 Buys and 8 Holds. The shares are currently trading for $154.56 and their $165.37 average target price suggests they will add another 7% in this coming year. (See GOOGL stock forecast)

Meta Platforms

Last on our list of Jefferies AI picks is Meta, the parent company of Facebook, Instagram, Messenger, and WhatsApp – and another of the market’s trillion-dollar tech mega-caps. Meta is currently valued at $1.27 trillion, making it the sixth-largest company on Wall Street.

Meta’s greatest asset is its scale – the company’s 4Q23 report, the last released, showed solid user numbers. Closing out 2023, Meta had 3.19 billion ‘family daily active people’ (DAP), and 3.98 billion ‘family monthly active people’ (MAP). Those numbers count users across all of the company’s platforms, and indicate that Meta can reach nearly half of the total global population.

Meta’s leading platform, Facebook, accounts for the largest portion of the company’s total audience, with a daily active user (DAU) total of 2.11 billion in December 2023, and a monthly active user (MAU) number of 3.07 billion. We should note that Meta’s platform user numbers likely include a high level of overlap between platforms. Even so, the company has a reach that few others, of any type, can match.

On the AI front, Meta is beginning to work with the technology in multiple applications. These include marketing and device linking, but one of the most important may turn out to be the company’s AI-based seamless communications, designed to facilitate multiple-language translations. The applications of such technology to social media platforms, which are already built to accommodate multiple languages, is obvious. Meta has also created the Llama models, an open-source AI development tool, created for multiple applications.

Meta reported solid earnings numbers in its last quarterly release. That release covered 4Q23 and showed revenue of $40.11 billion and earnings of $5.33 per share. The top-line figure was up 25% y/y and beat the forecast by $940 million, while the EPS was 39 cents per share better than had been estimated.

Turning one last time to analyst Brent Thill, we find him laying out a clear path for Meta toward long-term gains – based in large part on the company’s AI potential: “We believe META has a unique opportunity to introduce Gen AI tools to the almost 4 billion users across its family of apps. META has already leveraged AI to boost user engagement and advertiser ROI. We note that META is already introducing Gen AI advertiser tools, which, per our checks, are already leading to increases in performance. Additionally, META, with its Llama models, has become a backbone of the open-source community, putting META in an excellent position to benefit from its rise.”

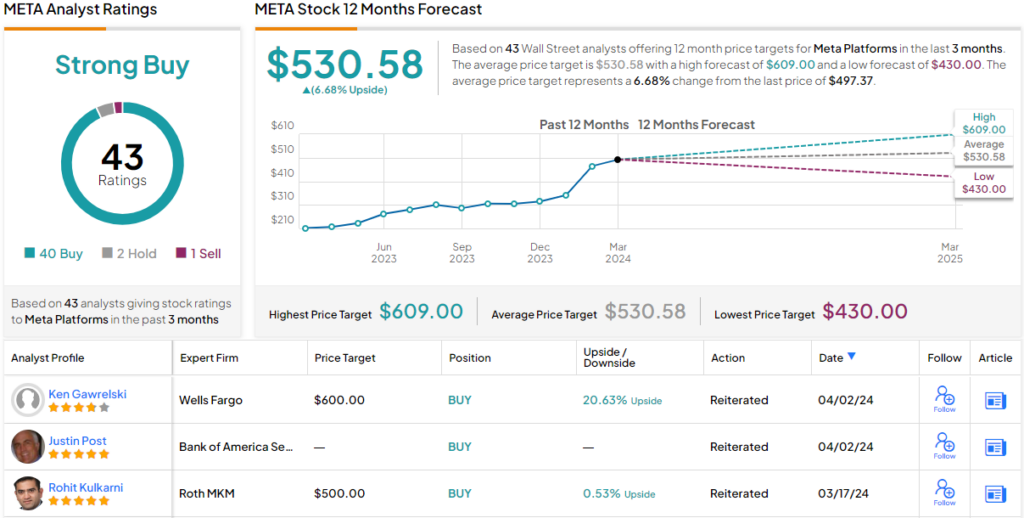

To this end, Thill rates META shares as a Buy, and he gives the stock a price target of $550, suggesting it will show a one-year gain of nearly 11%.

All in all, Meta is currently trading for $491.35 and its $530.58 average target price implies it will increase in share value by almost 7% by year’s end. The stock’s Strong Buy consensus rating is based on 43 recent analyst reviews – indicating high interest in the stock – that break down to a lopsided 40 Buys, 2 Holds, and 1 Sell. (See Meta stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.