Shake Shack (NYSE:SHAK) has underperformed the broader market since its IPO in January 2015. Since then, the stock has returned 106% compared to the 199% returns of the S&P 500 (SPX). Further, many of SHAK’s gains have come in the last week following its stellar Q4 results (released on February 15), which caused the stock to gain 26%. I believe that after several years of underperformance, Shake Shack is positioned for a breakout year due to its steady revenue growth, widening profit margins, and focus on store openings.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

An Overview of Shake Shack

Operating in the fast-casual restaurant space, Shake Shack is known for its made-to-order beef burgers, crispy chicken, and homemade lemonades. The first Shake Shack store was opened in 2004 at the Madison Square Garden in New York City. Over the last two decades, it has expanded to 510 locations, which includes 330 domestic outlets in 33 U.S. states and 180 international locations across London, Hong Kong, Dubai, Singapore, Istanbul, and more.

How Did Shake Shack Perform in Q4 2023?

Shake Shack reported revenue of $286.2 million with adjusted earnings of $0.02 per share in Q4 2023. Comparatively, analysts expected sales of $280.2 million with earnings of $0.01 per share in the December quarter. Shake Shack increased its sales by 20% year-over-year in the quarter, as it opened 15 new restaurants in Q4.

The last year was a breakthrough year for Shake Shack, as it surpassed 500 outlets, allowing it to grow system-wide sales by 20% year-over-year to $1.7 billion. Despite a challenging macro environment, the company expanded its operating margin by 240 basis points to almost 20%.

Moreover, its adjusted EBITDA (earnings before interest, tax, depreciation, and amortization) more than doubled to $131.8 million in 2023, and it grew its adjusted EBITDA margin by 400 basis points in 2023.

What Does Shake Shack Expect in 2024?

In 2024, Shake Shack expects to grow total sales between 11% and 15%. It plans to open 80 new restaurants, allowing it to end the year with almost 600 locations, more than double the footprint in 2019. It also expects to grow its adjusted EBITDA by 21% to 29% year-over-year to reach between $160 million and $170 million.

Comparatively, analysts tracking Shake Shack stock forecast adjusted earnings to grow by 78.5% to $0.66 per share in 2024 and by 37% to $0.90 per share in 2025. So, SHAK stock is priced at 148x forward earnings, which is very steep, as the median sector earnings multiple is far lower at 15.9x.

However, growth stocks command a premium multiple, and Shake Shack is growing at a much faster pace compared to its peers.

Licensing Business Growth Is Strong

Shake Shack expects its Licensing business to remain a key driver of profit margins. In 2023, it grew Licensing sales by more than 25% year-over-year to $40.7 million. This business now accounts for 3.7% of sales, up from 3.5% in the year-ago period.

Shake Shack opened 44 new licensed Shacks in 2023 and nine outlets in Q4. It ended the year with 223 licensed Shacks in 17 countries, indicating an increase of 23%.

Licensing is a high-margin segment for the company, as revenue is derived as a percentage of sales from these outlets, in addition to certain fees such as territory fees and opening fees.

Focus on Customer Engagement and Brand Building

Shake Shack aims to target throughput improvement by reducing guest order times by 30 seconds or more at its locations. It will achieve this goal by revamping its kitchen flows, increasing real-time reporting and training its staff, enhancing the customer experience in the process.

Shake Shack also plans to strengthen its brand awareness in 2024 and build on its global brand appeal. While the company has almost doubled its locations in the last five years, it has massive room to grow, especially in regions such as Asia and the Middle East. Shake Shack is quite early in its growth journey if we compare it with peers such as McDonald’s (NYSE:MCD), Domino’s (NYSE:DPZ), and Restaurant Brands International (NYSE:QSR).

It currently spends just 1% of sales on advertising, much lower than its competitors. Shake Shack aims to increase ad spending going forward, especially if profit margins continue to expand.

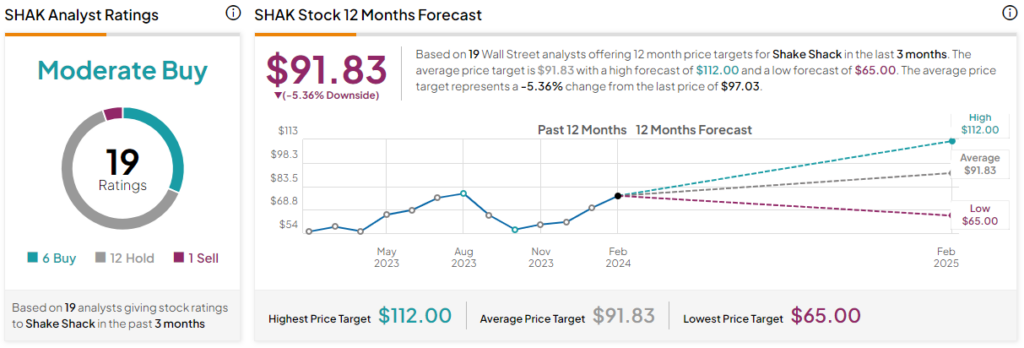

Is SHAK Stock a Buy, According to Analysts?

Out of the 19 analysts covering SHAK stock, six recommend a Buy, 12 recommend a Hold, and one recommends a Sell, giving it a Moderate Buy consensus rating. The average SHAK stock price target is $91.83, 5.4% below the current price.

The Takeaway

Shake Shack has showcased its resiliency amid an uncertain macro environment. While the restaurant space can be extremely competitive and brutal, Shake Shack continues to expand at an impressive pace in the U.S. and internationally. Its lofty valuation might make SHAK stock unattractive to most investors. However, if the company can meet its growth targets, it should deliver outsized gains in the upcoming decade.