Shares of Intel Corp. slipped about 9.4% in extended trading on Thursday after the semiconductor giant’s data-center group’s sales of $5.9 billion fell short of analysts’ expectations of $6.2 billion and declined 7% year-over-year.

Intel’s (INTC) 3Q revenues declined 4% year-over-year to $18.3 billion but surpassed the consensus estimates of $18.2 billion. Meanwhile, its 3Q EPS slumped 22% to $1.11 and came in in-line with the Street estimates.

The company raised its 2020 guidance for both revenues and earnings. Intel now expects full-year revenue to grow by 5% to $75.3 billion, which is higher than the earlier forecast of $75 billion and analysts’ estimates of $75.1 billion. The company anticipates 2020 adjusted EPS to be $4.90, topping the earlier forecast and consensus estimate of $4.85.

As for 4Q, Intel forecasts revenue of $17.4 billion, which is lower than the Street estimate of $18.2 billion. However, it expects 4Q adjusted earnings to be $1.10 per share, compared to the analysts’ expectations of $1.07 per share. (See INTC stock analysis on TipRanks).

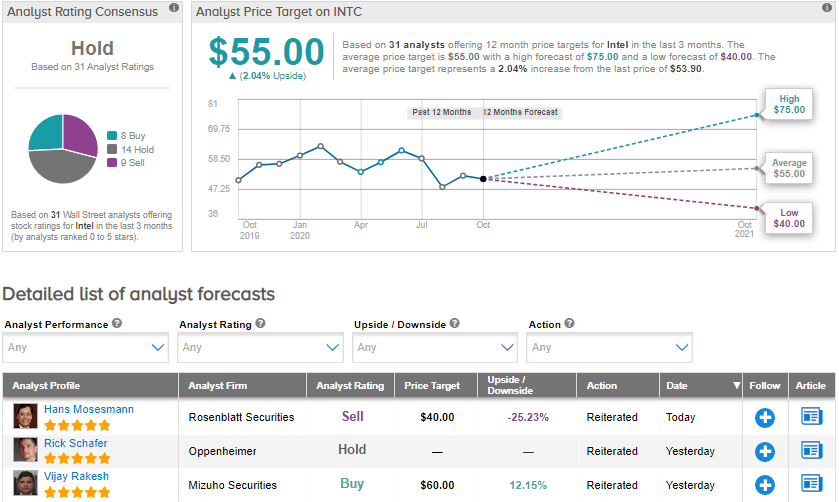

Following the results, Rosenblatt Securities analyst Hans Mosesmann lowered his price target to $40 (25.8% downside potential) from $45 and maintained a Sell rating. He believes the company’s “gross margins will be under pressure at least until 2H21.” The analyst also remains concerned about the delay of its 10nm Ice Lake Xeon scalable into 1Q21 and relentless competition from other semiconductor peers.

Currently, the Street is sidelined on the stock. The Hold analyst consensus is based on 14 Holds, 8 Buys and 9 Sells. The average price target of $55 implies upside potential of about 2.0% to current levels, with shares having already declined by 9.9% year-to-date.

Related News:

Intel To Sell Memory Unit To SK Hynix For $9B

NXP Semi Pops 5% On Q3 Guidance Boost; Analyst Says Hold

AMD Could Ink $30B Xilinx Deal As Soon As Next Week- Report