In this article, I will outline why I hold a neutral outlook on Robinhood (NASDAQ:HOOD) while maintaining a bullish stance on Interactive Brokers (NASDAQ:IBKR).

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

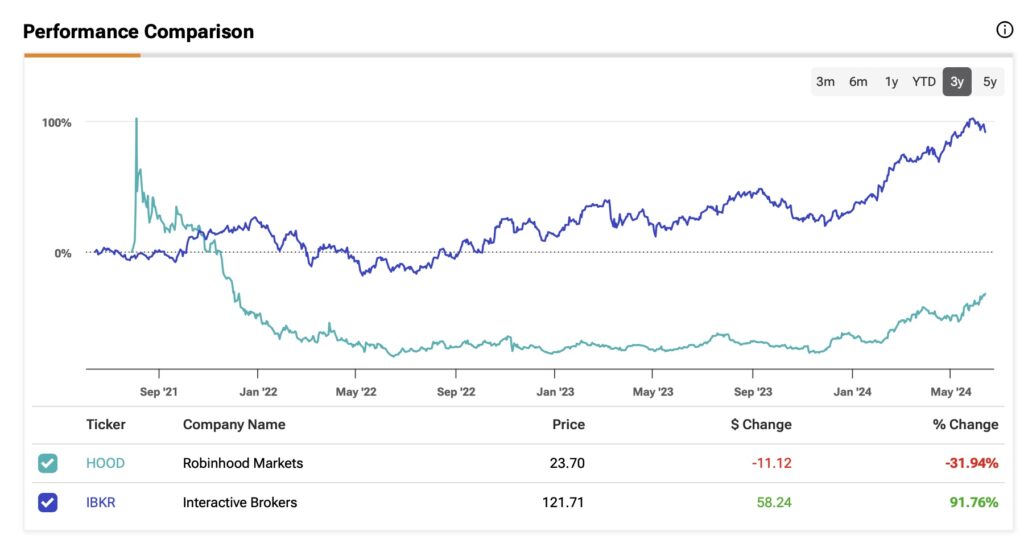

While both companies are major players in the brokerage industry, Robinhood and Interactive Brokers have distinct business models, target different audiences, and show different levels of financial stability. From my perspective, Interactive Brokers adopts a significantly more defensive strategy compared to Robinhood, making the latter highly vulnerable to market volatility. This stark contrast is reflected in the performance of their stocks (as shown by TipRanks’ Comparison Tool), which have shown minimal correlation over recent years.

Robinhood vs. Interactive Brokers: A Tale of Two Strategies

Robinhood was founded with the mission of democratizing the markets, providing easy access primarily to retail investors through a user-friendly platform without charging commissions.

To generate revenue without commissions, the platform sells its clients’ orders to market makers for a few pennies, a practice known as payment for order flow (PFOF), and this accounted for 75% of the company’s total revenue last year. Other less significant revenue sources included interest on cash balances and margin lending.

While this business model tends to attract a large number of new accounts, it also makes Robinhood more vulnerable to volatility in its asset base, as users may withdraw funds for various life milestones.

In contrast, Interactive Brokers focuses on more experienced investors and financial advisors, offering advanced trading tools and an institutional-grade platform. The broker generates revenue primarily through a combination of commissions and interest income.

IBKR’s diversified business model, which is less dependent on a single revenue stream, enhances its resilience to market fluctuations. Over the past three years, spanning a bull market in 2021 and a bear market in 2022, the company has achieved a revenue growth CAGR of 21.5% and a net income CAGR of 34.8%.

Robinhood’s performance, on the other hand, tends to be more directly influenced by market sentiment. Shortly after its IPO in August 2021, Robinhood reached a market cap of ~$46 billion, with revenues nearly doubling from $958 million in 2020 to $1.815 billion in 2021, driven by rapid growth in new users and revenues during the COVID-19 pandemic and a bull market in the first half of 2021, bolstered by high demand for cryptocurrencies.

However, as macroeconomic conditions deteriorated, Robinhood struggled to sustain its growth, with revenues dropping to $1.35 billion in 2022, leading to a market cap decline to ~$6 billion by mid-2022.

During the same period, IBKR’s stock performance remained relatively stable, demonstrating the benefits of its diversified business approach.

The Key Difference Between Robinhood and Interactive Brokers

The big difference between Robinhood and Interactive Brokers is that the latter, by gearing its platform toward providing the best services at the best costs for qualified investors, consequently attracts high-value clients. This results in higher margin loans and more revenue per customer compared to its peers, especially Robinhood.

This contrast becomes evident when considering that Robinhood boasts around 24.4 million accounts, nearly 10 times more than IBKR’s 2.8 million. However, when we look at assets under management (AUM), Robinhood manages approximately $105 billion (calculated as assets under custody subtracted by cash held by customers), whereas IBKR manages around $465 billion.

This translates to a significant difference in the average asset value per account: each Robinhood account holds about $4,300 in assets, while each IBKR account holds approximately $166,000.

These disparities ultimately reflect in their financial performance. For instance, IBKR’s commission revenues have remained relatively stable since 2021, hovering around $1.35 billion to $1.36 billion in 2023. Meanwhile, its non-interest expenses have increased from $927 million in 2021 to $1,271 million in 2023, ensuring consistent profitability.

On the flip side, Robinhood is still striving for profitability, although the company is expected to report its first annual profit this year. If we look at “transaction-based revenues,” the commission-free broker generated $1.4 billion in 2021, $814 million in 2022, and $785 million in 2023. Meanwhile, its operating expenses were nearly three times its transaction-based revenues.

Is HOOD Stock a Buy, According to Analysts?

Even though Robinhood’s Q1-2024 transaction-based revenues surged 59% year-over-year, fueled by another crypto boom, this hasn’t convinced some of Wall Street’s firms.

Citi (NYSE:C) believes that the stock’s rally this year is largely attributed to the rising prices of Bitcoin (BTC-USD), and it is skeptical about the company’s potential for significant wins until its PFOF model shows more steady growth and consistency. Citi sees potential headwinds in a possible pull-back in Bitcoin prices as well as a gradual decrease in retail investor engagement. The firm has a Sell rating on Robinhood, which is reflected in the Hold consensus for HOOD.

The average HOOD stock price target of $21.27 implies 3% downside potential.

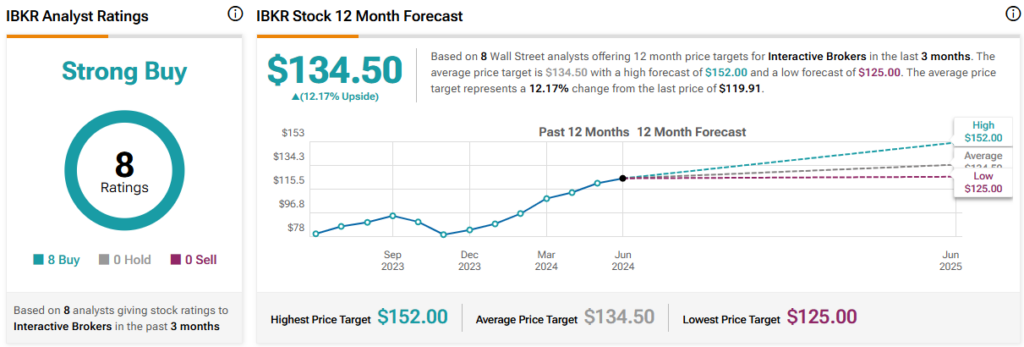

Is IBKR Stock a Buy, According to Analysts?

On the other hand, Citi sees IBKR in a strong position. Citi highlighted the strong organic growth momentum and potential moving forward (especially with IBKR’s standout features), including its account growth rate, which accelerated to 29% annualized growth in the first quarter of 2024, and its robust trading activity and margin lending. In light of this, the firm has a Buy recommendation on IBKR, reflected in the Strong Buy consensus for the stock.

The average IBKR stock price target of $134.50 implies 12.2% upside potential.

How Do Their Valuations Compare?

When we look at the valuations of these two brokers, Robinhood, which the market estimates will report an annual net profit this year, trades at a 27x forward price-to-earnings (P/E) ratio compared to IBKR’s 18x multiple. This discrepancy is significant.

However, when comparing price-to-book (P/B) ratio multiples, Robinhood trades at 3x, which is at a discount compared to IBKR’s P/B multiple of 3.5x.

In my view, the premium at which IBKR trades relative to its book value does not indicate overvaluation but rather reflects the market’s confidence in the company’s diversified business model, high-quality asset base, stable profitability, and growth prospects.

The Bottom Line

Based on my analysis, Robinhood’s business model, heavily reliant on market volatility and retail investor engagement, hasn’t proven to be sustainable yet. This raises questions about its long-term prospects, making the stock deserve its Hold rating.

Conversely, I maintain a bullish stance on Interactive Brokers. It is a defensive player, demonstrating resilience to market volatility with a target audience that consistently supports profitability. Moreover, the company shows promising growth prospects and trades at a discounted valuation compared to HOOD.