It’s not just red-hot AI stocks that have been helping investors gain lately. A handful of consumer-packaged goods (CPG) stocks — like GIS and KLG — have been really picking up traction lately, even with most Wall Street analysts having their backs turned on them.

Undoubtedly, consumer-packaged goods plays can be incredibly boring, especially if you’ve just taken profits off a technology sector high-flyer. Still, given how beaten down some of the least-loved CPG plays were (think the breakfast cereal top dogs), it should come as no surprise to see them marching higher following the mildest of positive developments.

However, the Wall Street community still says to “Hold.” But I consider the following two cereal companies to be value buys, if not for their dividends, for their potential to continue to gain should value begin to outdo growth. Indeed, maybe less than three rate cuts for 2024 spark such a rotation. In any case, less-loved value plays, including the cereal firms, strike me as being just a wholesome part of a balanced portfolio.

Therefore, let’s use TipRanks’ Comparison Tool to compare GIS and KLG and see which stock looks better.

General Mills (NYSE:GIS)

General Mills stock shed more than 31% from peak to trough last year as the blow of inflation began to be felt, causing many consumers to “trade down” to store-owned private label brands in most aisles at the grocery store.

Beyond inflation, various other headwinds have beaten down the cereal companies, including the rise of appetite-curbing GLP-1 (weight-loss) drugs and limited pricing power, even for General Mills’ most iconic brands. And, of course, the rotation back into tech stocks likely caused many to ditch GIS stock for one of the sought-after AI plays.

Despite the list of pressures, I’m inclined to stay bullish on GIS stock as it looks to impress with its Accelerate strategy. This strategy may just be able to help General Mills build enough momentum to beat estimates.

The Accelerate plan may be laying the stage for a glorious rebound, as the company aims to bring out the best in its brands to fire back at generics. Thus far, the plan has given an early hint of success. If management can execute, the best may have yet to come.

As inflation peaks out and consumers go out of cost-cutting mode, perhaps they’ll reach for those Honey Nut Cheerios over the Walmart (NYSE:WMT) Great Value alternative. Given that many private labels seem to have nailed down the quality factor (in addition to the price factor), my guess is that the branded CPG companies will need to get creative to win consumer dollars back.

As General Mills hikes bets on product innovation and digital capabilities (think targeted marketing) as part of its Accelerate plan (think its line of Mini cereals and Veggie Blends, just to name a couple), perhaps consumers will be intrigued enough to pay a bit more to try such new products.

Either way, the bar is low, with GIS shares trading at 15.8 times trailing price-to-earnings, below the CPG industry average of 20.2 times. The 3.3% dividend yield is a nice bonus as shares look to continue adding to their recent gains.

What Is the Price Target for GIS Stock?

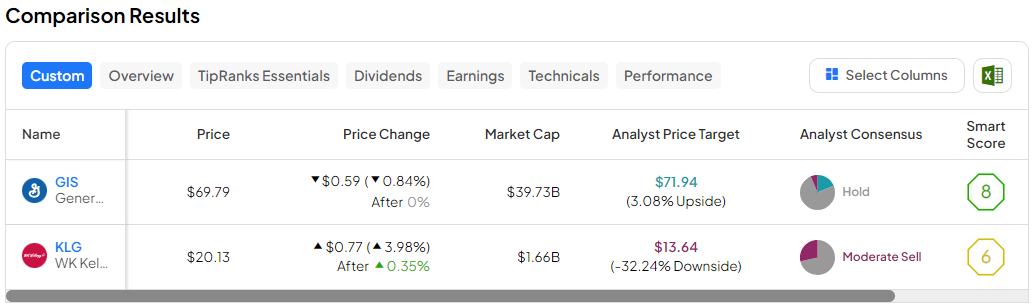

GIS stock is a Hold, according to analysts, with two Buys, 12 Holds, and one Sell assigned in the past three months. The average GIS stock price target of $71.13 implies 1.9% upside potential.

W.K. Kellogg (NYSE:KLG)

W.K. Kellogg, the cereal company that spun off from the original CPG kingpin Kellogg, was counted out by many investors and analysts as it quietly went live on the public markets last October. Indeed, cereal isn’t a high-growth industry.

It’s an “unsexy” business for sure, but the price of admission was also incredibly depressed at the time, when shares went for around $10 and change. Today, the stock is above $20. W.K. Kellogg stock may have been a “cigar butt” type of investment for some, but it has proven to be a wise bet for the deep-value investors who stuck with the firm and management’s turnaround efforts.

For the fourth quarter, W.K. Kellogg easily topped estimates, clocking in earnings per share of $0.30, well ahead of the $0.21 analyst estimate. The company also raised its adjusted EBITDA growth forecast, now expecting the number in the $265-270 million range, up ever so slightly from the original forecast of $255-265 million.

Despite enduring the same inflationary headwinds as most other CPG companies, W.K. Kellogg was able to pull off a great result, thanks in part to modest estimates and impressive new product launches. With intriguing health-conscious and protein-rich products, like the Eat Your Mouth Off brand, W.K. Kellogg seems to be resonating with consumers in this somewhat harsh industry environment.

Personally, I think far too many discounted the capabilities of management right off the bat. After a wonderful run out of the gate, it’s about time to put the cereal darling back atop one’s watchlist before analysts find enough reason to upgrade their recommendations. Indeed, it looks like the Kellogg spin-off is already beginning to bear fruit. The 3.2% dividend yield itself also looks quite nourishing.

What Is the Price Target for WLK Stock?

KLG stock is a Hold, according to analysts, with zero Buys, six Holds, and two Sells assigned in the past three months. The average KLG stock price target of $13.56 implies 32.6% downside potential.

The Bottom Line

The most impressive disruptive innovators have captured the hearts of growth investors. Though growth can continue to run in 2024, I can’t help but notice how high expectations (and analyst estimates) have risen.

Eventually, expectations may grow too high, and not even a cutting-edge innovator can beat the mark. In such a scenario, I’d much rather gravitate to companies with such low estimates that it doesn’t take too much effort to move the needle higher.

In the case of General Mills and W.K. Kellogg, expectations remain so modest that even subtle successes with their respective turnaround plans may be enough to continue their recent rallies.

Between the two stocks, I have to go with W.K. Kellogg. But do be warned, as it has zero Buys on Wall Street, even after the recent success of its new products and its recent beat. Perhaps it’s time for analysts to revisit the drawing board as management looks to continue proving its doubters wrong.