Software as a service (SaaS) is big these days. How big? The global market size is estimated at over $270 billion and is estimated to reach $1.2 trillion by 2030, reflecting a compound annual growth rate (CAGR) of 19.7%. In the dark of night, while we were sleeping, old-school performance training company Franklin Covey (NYSE:FC) evolved into a SaaS provider, unlocking tremendous growth potential and making the stock an intriguing investment for long-term growth investors.

Training on Demand

Franklin Covey is primarily involved in improving organizational performance on a global scale. The company offers time management and effectiveness solutions for individuals and corporations through online training, in-person workshops, and events.

The company utilizes several platforms to achieve its objectives. However, the All Access Pass, a subscription platform that aids in the better deployment of content, services, technology, and metrics to deliver behavioral impact at scale, is the real SaaS game-changer for the company.

Franklin Covey is also aggressively ramping up its Education Division, recently adding a record number of schools and hitting all-time highs in education subscription revenue.

Franklin Covey’s Outlook

Franklin Covey recently announced financial results for Q2 FY24. The company achieved revenue of $61.3 million, slightly missing expectations of $62.02 million, and posted an EPS of $0.06, beating the Street’s estimate of $0.04.

Looking ahead, management anticipates a slower subscription service sales recovery, which will likely affect sales growth in the upcoming third and fourth quarters. The economic environment, which has provoked hesitation and created a challenging sales backdrop during the first half of Fiscal 2024, has also led the company to anticipate an adjusted EBITDA of $54.5 million for the year, which is at the lower end of its guidance range.

That said, FC heads into the second half of the year expecting a positive shift. Management predicts that despite the first half’s hurdles, the company is optimistic about hitting record levels of revenue, adjusted EBITDA, and free cash flow in Fiscal 2024.

What is the Price Target for FC?

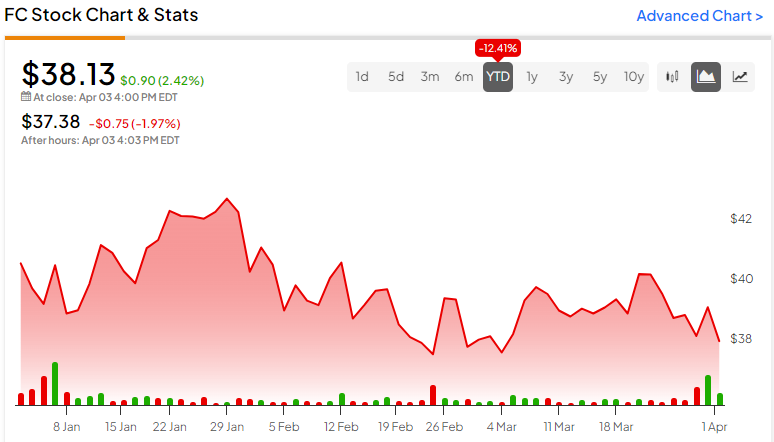

FC stock currently trades at the lower end of its 52-week price range of $32.19-$48.76 and demonstrates negative price momentum trading just below the 20-day and 50-day moving averages of 38.84 and 39.33, respectively.

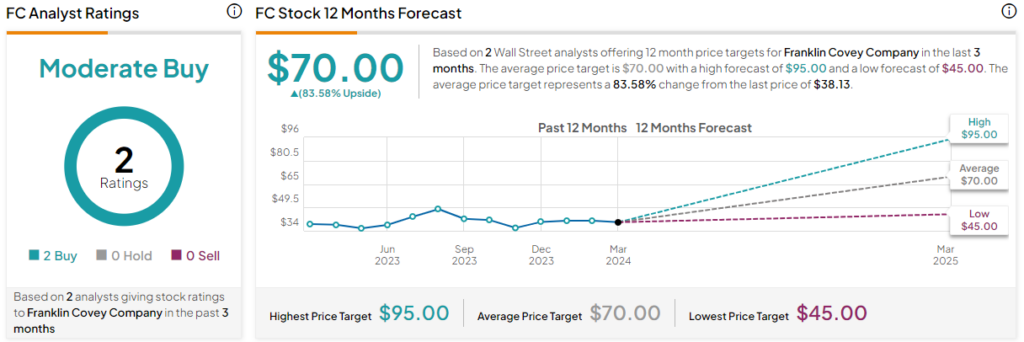

The company is thinly followed by Wall Street, though the analysts covering it are bullish on the stock. Barrington analyst Alexander Paris recently lowered the price target from $55 to $45 while keeping a Buy rating on the stock. He sees the pullback in the stock due to the company’s guidance on near-term softness as a potential buying opportunity for long-term capital appreciation.

Overall, Franklin Covey is rated a Moderate Buy based on the Buy recommendations of two analysts in the past three months. The average price target for FC is $70, which represents an 83.58% upside from current levels.

Final Thoughts on FC

Franklin Covey’s evolution into a SaaS provider underscores a compelling opportunity for long-term growth investors. The company’s foray into delivering organizational improvement, primarily via its All Access Pass subscription platform, has positioned it uniquely in the thriving SaaS market.

While the immediate financial outlook presents a nuanced picture, the long-term growth potential is promising, suggesting the near-term softness may offer an appealing entry point for investors.