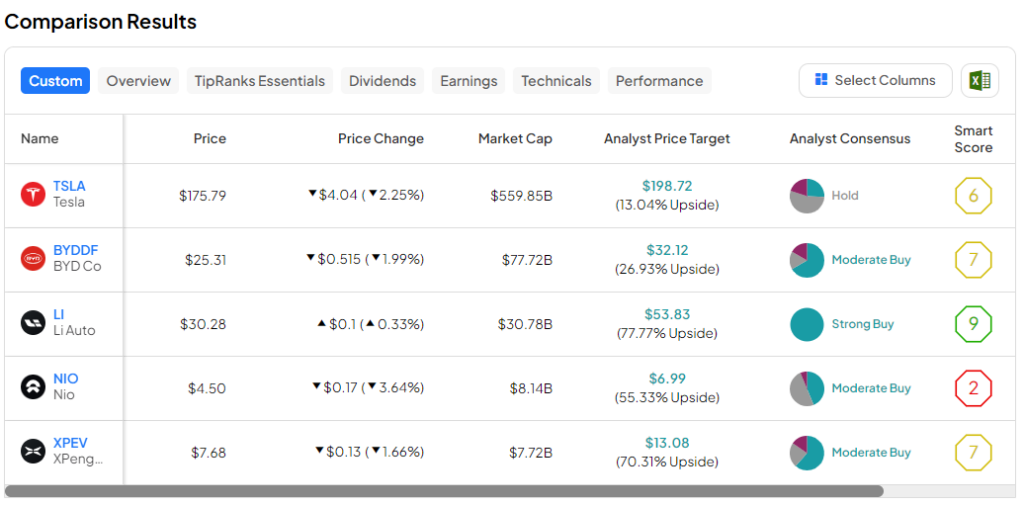

Cathie Wood once said that Tesla (NASDAQ:TSLA) was in a prime position to dominate the EV market. However, things are changing, and Wood may have been wrong. Tesla is no longer the world’s leading EV producer, and it’s getting harder to argue that Tesla deserves its valuation premium. Tesla is trading at 58.8x forward earnings, making it incredibly expensive versus its profitable Chinese peers like BYD (NASDAQ:BYDDF) and Li Auto (NASDAQ:LI).

On a price-to-sales basis, it’s also more expensive than NIO (NYSE:NIO) and XPeng (NASDAQ:XPEV). Of the four listed in the headline, only BYD and Li Auto have turned a profit, but they’re both trading at much lower multiples than Tesla, at 15.6x forward earnings each. This is why I’m bearish on Tesla. See how the five stocks compare below using TipRanks’ comparison tool.

Growth Slowing

One of the biggest challenges when trying to justify Tesla’s lofty multiples is its slowing growth. While deliveries grew by 20% in Q4 2023, total revenue growth slowed to just 3%. It goes without saying that a company trading at 58.8x earnings should be growing revenue faster than 3%.

It’s also worth noting that in both Q1 2023 and Q3 2023, Tesla’s revenues were sequentially down quarter-over-quarter. Gross profit also fell, down 23% year-over-year. Behind all of this were falling margins. Tesla said that its total GAAP gross margin declined 612 basis points from 23.8% in Q4 2022 to 17.6% in Q4 2023.

These falling margins haven’t been enforced but simply reflect the company’s aggressive pricing strategy, which aims to increase market share while putting pressure on peers like BYD, Li, NIO, and XPeng. But arguably, the results haven’t been overwhelmingly positive, with Tesla losing its leading position — in terms of units sold — to BYD and other companies like Li Auto boasting stronger margins than Tesla.

Valuation Conundrum

My biggest concern about Tesla’s valuation relates to its price-to-earnings-to-growth (PEG) ratio. Currently, the PEG ratio stands at 3.8. Given that a ratio of 1.0 is considered fair value, we can deduce that Tesla is overvalued, at least for the medium term, as the PEG ratio is formed from analysts’ expectations for the next three to five years. In fact, this ratio of 3.8 is one of the highest I’ve come across for a non-dividend-paying stock.

The caveat, of course, is that the PEG ratio is formed using analysts’ medium-term forecasts. As we know, forecasts can be incorrect, and these figures don’t take into account the potential for growth beyond the medium term. Should autonomous vehicles get widespread regulatory approval, Tesla could once again be in a prime position to dominate this new and exciting sector. The issue is that many analysts don’t see this happening until at least the end of the decade.

According to those following the topic closely, we’ll start seeing autonomous vehicles more widely available around 2030. These are vehicles that can travel some highways and some city streets, or parts of a city, entirely on their own. However, entirely autonomous vehicles (Level 5 vehicles) that can get you from your home to your destination, perhaps just using your smartphone, likely won’t be a reality until 2040. This means that Elon Musk’s dream of a fleet of autonomous Tesla taxis won’t be a reality anytime soon.

By comparison, Tesla’s peers look like they present better value in the medium term. For example, Li Auto has a forward P/E ratio of 15.6x and a PEG ratio of 0.8, and BYD also has a forward P/E of 15.6 and a PEG ratio of around 0.75. Meanwhile, XPeng and NIO, which are yet to turn a profit, also have attractive metrics relative to Tesla. XPeng’s forward EV-to-sales ratio is 0.69x, NIO’s is 0.88x, and Tesla’s is 4.79x. These Chinese firms have more attractive valuations, but they also carry more political risk.

Is Tesla Stock a Buy, According to Analysts?

Tesla stock has a Hold rating according to the consensus opinion of analysts covering the stock. There are nine Buy ratings, 19 Hold ratings, and seven Sell ratings. The average Tesla stock price target is $198.72, inferring 13% upside from the current share price. The highest share price target is $320, while the lowest share price target is just $23.53. It’s interesting to note that all of the last five updates from analysts have seen Tesla assigned a Hold rating.

The Bottom Line

Tesla stock looks vastly overvalued compared to Chinese peers when we focus on near and medium-term valuations. Of course, we should recognize and take into account the fact that Chinese companies carry more political risk and tend to trade at lower multiples, and thus may never actualize fair value even if the companies perform well.

However, it remains hard to justify Tesla’s premium to its Chinese peers. While there is clearly a huge amount of promise in driverless vehicles, investing in Tesla for its potential to generate revenues from the sector in five, 10, or 15 years’ time is somewhat speculative.