C3.ai, Inc. (AI) provides enterprise AI software for digital transformation. The company recently posted better-than-expected performance for the second quarter, with revenue increasing 41% year-over-year to $58.3 million, thanks to a jump in subscription revenue.

Q2 Performance & Updated Guidance

Furthermore, the remaining performance obligations of the company increased to $465.5 million from last year’s $267.4 million. AI’s customer count also surged to 104, clocking a 63% year-over-year growth. Meanwhile, Net loss per share widened to $0.26 from $0.23 a year ago.

Notable, AI has expanded its relationship with Baker Hughes (BKR) extending its terms to six years from five, and increasing the contract value by $45 million to $495 million.

The company has also upped its revenue guidance for fiscal 2022, projecting 35% to 37% growth against 17% growth in fiscal 2021. Total revenue is expected to be in the range of $248 million to $251 million for fiscal 2022.

With these developments in mind, let us take a look at the changes in AI’s key risk factors that investors should know.

Risk Factors

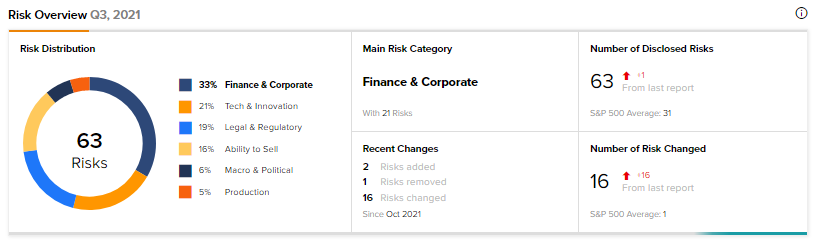

According to the TipRanks Risk Factors tool, AI’s top risk category is Finance & Corporate, contributing 33% to the total 63 risks identified. In its recent quarterly report, the company has added two key risk factors.

Under the Finance & Corporate risk category, AI highlighted that its financial results could see an adverse impact due to changes in accounting standards and subjective assumptions, estimates, and judgments made by management associated with accounting matters.

Under the Legal & Regulatory risk category, AI noted that there is more focus from investors, regulators, and other corporate stakeholders on corporate policies related to environmental, social, and governance matters. (See Insiders’ Hot Stocks on TipRanks)

The possibility remains that these stakeholders may not be satisfied with AI’s existing practices on these matters, or with the pace at which any revisions are made to the company’s practices, or those of its customers or partners.

Additionally, these stakeholders may also object to the societal and ethical costs or implications related to the use of the company’s products by any of its customers. The risk also remains that AI may incur increased costs, and may need additional resources related to corporate disclosure obligations in the future.

Compared to a sector average of 17%, AI’s Legal & Regulatory risk factor is at 19%.

Wall Street’s Take

On December 3, Deutsche Bank analyst Patrick Colville reiterated a Hold rating on the stock and decreased the price target to $36 from $50. The analyst noted that AI’s second-quarter subscription revenue and customer additions fell short of the Street’s expectations.

Consensus on the Street is a Hold based on 4 Buys, 2 Holds, and 2 Sells for the stock. The average C3.ai price target of $55.13 implies a potential upside of 62.19% for the stock. That’s after a 45.3% drop in AI’s share price over the past six months.

Related News:

ExxonMobil Targets Net Zero Emissions in Permian Basin by 2030

Stitch Fix: Q1 Results Top Estimates, Q2 Revenue Guidance Disappoints

ChargePoint Books Wider-than-Expected Q3 Loss; Shares Drop After-Hours