Booking Holdings stock (BKNG) has recorded a notable decline recently, likely due to investor concerns about a perceived slowdown in the company’s latest growth figures. Along with a broader market sell-off, BKNG stock has wiped out its year-to-date gains within a matter of days. Nevertheless, these concerns appear exaggerated when viewed in the proper context. Booking, a leading online travel services company with global operations, has been up against challenging comps from previous years. Further, its earnings growth prospects continue to be robust. Accordingly, I remain bullish on BKNG stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Booking’s Q2 Results Need to be Viewed in the Right Context

Assessing Booking’s Q2 results within the proper context is crucial to avoid misinterpreting what appears to be a slowdown in growth compared to Q1. Specifically, Booking reported a revenue increase of just 7.3% in Q2, marking the fifth consecutive quarter of decelerating revenue growth and a notable slowdown compared to the previous quarter’s 16.9% and the previous year’s 29.2%.

However, this perceived slowdown is primarily a natural adjustment following the dramatic ups and downs of the post-pandemic era. The travel industry had been severely impacted, followed by a massive rebound in subsequent years, which now seems to be stabilizing. Booking’s Q2 numbers are measured against exceptionally high growth figures from previous quarters, which followed even more remarkable growth in prior years.

For context, Booking’s revenues grew by 61.3% in FY2021, 51.6% in FY2022, and 25.0% in FY2023. Hence, some normalization in FY2024 after three years of excessive travel spending (driven by the post-pandemic “revenge travel” trend) is to be expected and not necessarily alarming.

Industry Conditions Remain Excellent, Will Keep Fueling Growth

The fact that Booking’s growth remains positive, surpassing the record levels set in recent years following outsized growth, clearly demonstrates that industry conditions remain ideal. This trend was a key highlight of the company’s Q2 report, showcasing strong performance across every critical business metric.

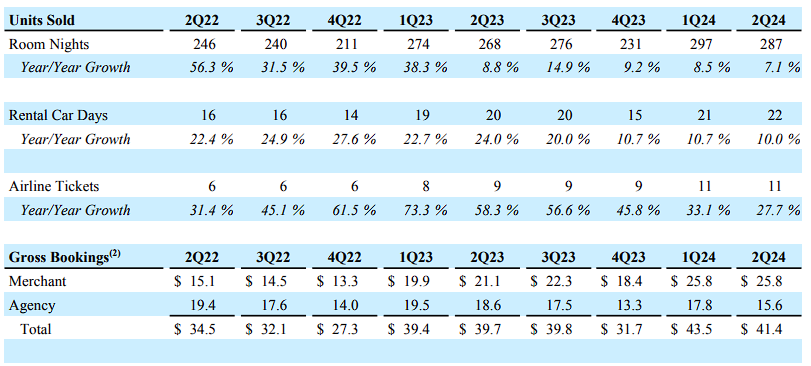

To give an overview, travelers booked 287 million room nights during the quarter, marking a 7% increase compared to the previous year. This uptrend was particularly notable in regions such as Asia, which saw mid-teens growth, and the U.S., which experienced a slight improvement.

Even Europe, which showed a mild moderation, still contributed significantly to the overall performance, backed by Booking’s leading market position in the region. Performance in rental car days also remained rather strong, registering double-digit growth, as you can see below.

Another sign of favorable industry conditions was evident in alternative accommodations, an area in which Booking has focused intensely lately as it attempts to compete directly with Airbnb (ABNB). Specifically, due to the rising trend towards unique and non-traditional lodging options, Booking expanded its alternative accommodation listings by 11% year-over-year, reaching approximately 7.8 million. This boosted alternative accommodation room nights booked by 12%.

The last catalyst I want to mention, which not only played a notable role in driving Booking’s revenues but also reflects a thriving travel industry, is the 28% increase in air tickets booked mainly through Booking.com and Agoda. This surge, credited by management to Booking’s enhanced flight options and robust travel demand, resulted in increased platform bookings and drew new customers who, according to the company, frequently explored other services offered by Booking, such as car rentals.

Overall, it’s clear that the travel industry is thriving, and Booking is leveraging key trends to its advantage. Wall Street shares this optimism, projecting a 7.6% increase in revenue for the full year, reaching nearly $23 billion. This growth is then expected to accelerate to 8.1% in FY2025 and 9.3% in FY2026, confirming the earlier notion that this year’s results, while still strong, are being impacted by tough comps.

Booking’s Valuation Is Quite Attractive

Given Booking’s current valuation following the recent drop in share price, it’s challenging to justify a bearish stance. The stock appears undervalued in relation to its earnings growth potential. Specifically, this year’s anticipated revenues, coupled with the favorable economics of the company’s business model, are expected to drive earnings per share (EPS) growth of 15.5% to a record $175.78.

This translates to a forward price-to-earnings (P/E) ratio of just 19.3x, which seems to be particularly low, given that consensus EPS estimates project double-digit growth throughout the rest of the decade. I agree with these estimates, as Booking’s asset-light business model should continue to deliver strong earnings growth, even with modest revenue increases. In any case, these estimates suggest that Booking is attractively priced today.

Is BKNG Stock a Buy, According to Analysts?

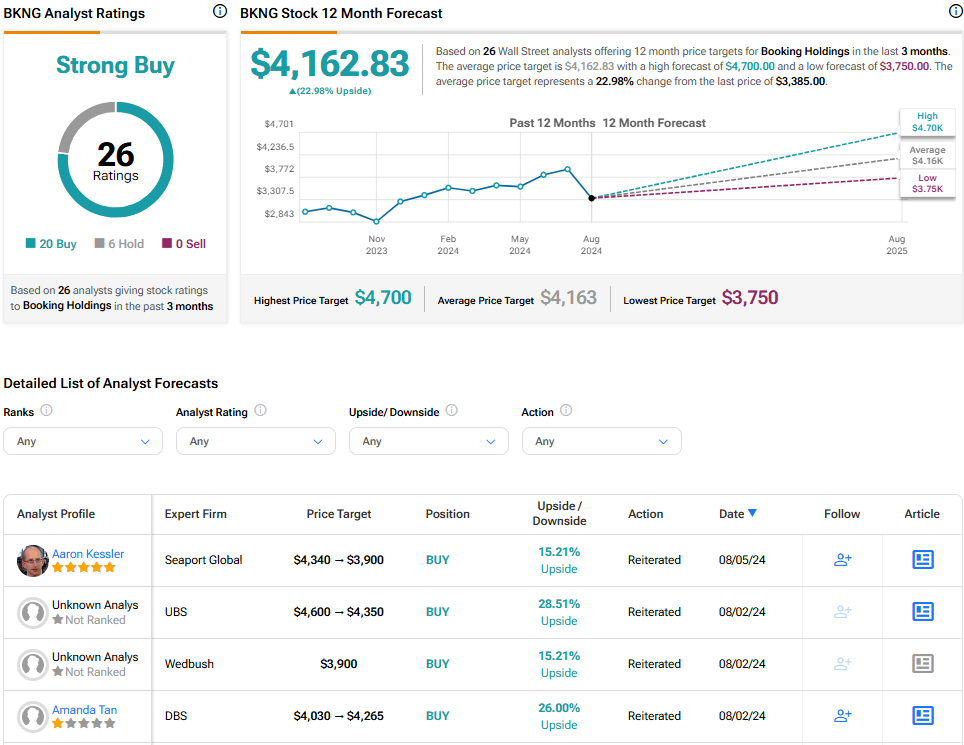

Looking at Wall Street’s view on the stock, Booking Holdings has a Strong Buy consensus rating based on 20 Buys and six holds assigned in the past three months. At $4,162.83, the average BKNG stock price target implies 23% upside potential over the next 12 months.

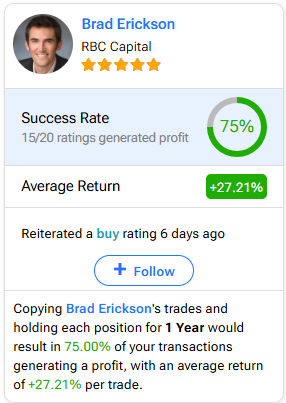

If you’re wondering which analyst you should follow if you want to buy and sell BKNG stock, the most accurate analyst covering the stock (on a one-year timeframe) is Brad Erickson of RBC Capital, with an average return of 27.21% per rating and a 75% success rate. Click on the image below to learn more.

The Takeaway

In summary, Booking’s recent share price decline seems overstated when considering the context of normalized growth post-pandemic and robust industry conditions. Despite a slowdown in Q2 revenue growth compared to previous years, the travel sector remains strong, and Booking’s key performance indicators, including rising room and flight bookings, highlight its resilience.

In the meantime, with an attractive valuation and continued earnings growth potential, Booking’s stock seems to present a compelling investment opportunity at its current levels.