Hotels experienced improved demand last year following the easing of travel restrictions. However, will macro uncertainty, geopolitical tensions, rising interest rates, and labor challenges hamper the pace of recovery?

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

According to analytics firm STR, the Baird/STR Hotel Stock Index increased 2.2% in March to 5,882. Michael Bellisario, senior hotel research analyst, and director at Baird noted that hotel stocks were up in March but underperformed their benchmarks.

However, Bellisario highlighted that underlying hotel fundamentals continued to improve in March, and the outlook appears more favorable currently than a month ago despite all the background noise in the stock market and higher interest rates.

Bearing that in mind, we used the TipRanks stock comparison tool for hotel stocks to compare Wyndham, Hilton Worldwide, and Marriott and discuss which stock could yield better returns.

Wyndham Hotels & Resorts (NYSE: WH)

Wyndham is a leading hotel franchisor, with 9,000 hotels across nearly 95 countries. Its portfolio comprises 22 hotel brands, including Super 8, Days Inn, Ramada, Microtel, La Quinta, Baymont, Wingate, AmericInn, Hawthorn Suites, Trademark Collection, and Wyndham.

While Wyndham is essentially focused on the economy (48% of the chain) and midscale (44%) segments, it is also expanding its upscale presence (8%). It is worth noting that nearly 70% of bookings at Wyndham’s hotels are leisure-oriented, which makes the company’s hotel owners less reliant on business travel.

Wyndham’s revenue grew 20% to $1.57 billion in 2021, driven by a 47% increase in global RevPAR (revenue per available room) due to the recovery in travel demand and a 2% increase in system size. Excluding the impact of currency fluctuations, global RevPAR recovered to 88% of 2019 levels. Overall, adjusted EPS surged 207% to $3.16 in 2021.

As of December 31, 2021, Wyndham’s development pipeline consisted of over 1,500 hotels and more than 194,000 rooms. About 65% of the development pipeline is international, and over 80% is in the midscale and above segments.

Given the strength in the economy space and rising consumer demand for affordable extended-stay products, Wyndham is launching its first extended-stay brand for the economy segment. Per the company, economy extended-stay hotels are particularly resilient amid a downturn.

Under the working title of Project ECHO, an acronym for Economy Hotel Opportunity, Wyndham recently announced newly awarded contracts to develop 50 hotels for the economy extended-stay hotel brand.

Following virtual meetings with senior management, Jefferies analyst David Katz noted that ADRs (average daily rates) for the economy and midscale offerings are driving robust performance and should push FY22 U.S. RevPAR above 2019 levels. Management believes that rates are durable as their portfolio is heavily leisure-oriented.

Further, Katz is of the opinion that pent-up leisure demand should help rates stick in the near term. He believes that Wyndham’s leisure-oriented portfolio, growth into extended stay, stable cash flows, and capital returns “should drive valuation upside vs the group.”

Based on his optimism, Katz reaffirmed a Buy rating on Wyndham and a price target of $106.

Other analysts on the Street echo Katz’s bullish sentiment, with a Strong Buy consensus rating based on four unanimous Buys. The average Wyndham Hotels price target of $98 suggests 22.62% upside potential over the next 12 months.

Hilton Worldwide Holdings (NYSE: HLT)

Hilton, a leading global hospitality company, boasts a portfolio of 18 popular brands comprising more than 6,800 properties and over one million rooms in 122 countries. As of December 31, the company had 54 owned properties, 745 managed hotels, and 6,038 franchised hotels.

The rapid administration of COVID-19 vaccines and the easing of travel restrictions drove improvements in Hilton’s business last year. Specifically, Hilton’s revenue grew 34.4% to $5.8 billion in 2021. Adjusted EPS surged to $2.08 in 2021 from $0.10 in 2020.

On a comparable and currency-neutral basis, 2021 system-wide RevPAR and ADR increased 60.4% and 12.9%, respectively, from 2020. However, these key metrics were down 30% and 9.9%, respectively, compared to 2019. Meanwhile, occupancy rates improved 16.9 percentage points to 57.2% in 2021.

As of December 31, 2021, Hilton’s development pipeline comprised nearly 2,670 hotels and about 408,000 rooms in 115 countries, including 28 countries and territories where the company currently doesn’t have any presence.

Notably, 249,600 rooms in the pipeline were located outside the U.S. Overall, Hilton is focused on strengthening its international presence and the continued expansion of its luxury portfolio.

Despite short-term choppiness due to newer variants, the company is optimistic about accelerated recovery across all segments in 2022.

Reacting to management’s commentary on Q421 results, Deutsche Bank analyst Carlo Santarelli stated, “Strong demand and pricing trends across the lodging space are not a secret, and with 2023 adjusted EBITDA forecasts 20% above 2019 levels, we believe this “thematic recovery” is largely priced in.”

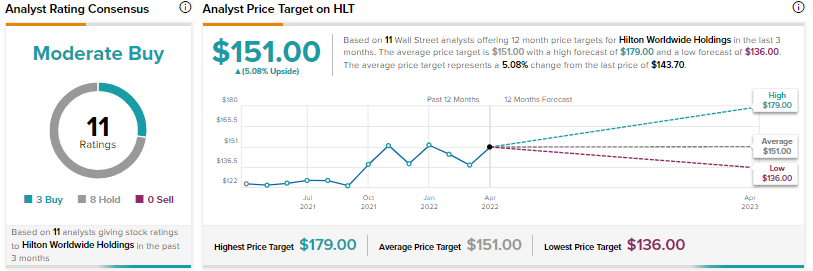

Santarelli maintained a Hold rating on HLT but increased his price target to $136 from $126 due to improved forecasts.

Meanwhile, the Street is cautiously optimistic on Hilton, with a Moderate Buy consensus rating based on three Buys and eights Holds. At $151, the average Hilton price target implies 5.08% upside potential from current levels.

Marriott International (NYSE: MAR)

Marriott International has an extensive presence in 139 countries with nearly 8,000 properties under 30 leading brands, including prominent names like JW Marriott, The Ritz-Carlton, St. Regis, Bvlgari, Marriott Hotels, and Sheraton. As of year-end 2021, Marriott had 64 owned properties, 1,943 managed properties, and 5,880 franchised and licensed properties.

Improved demand following the easing of COVID-19 restrictions drove a 31% rise in Marriott’s 2021 revenue to $13.9 billion. Comparable systemwide RevPAR and ADR improved 60.4% and 10%, respectively, from 2020, but were down 36.5% and 11%, respectively, from 2019 levels.

Worldwide occupancy rates came in at 51.3%, reflecting a 16.1 percentage points improvement from 2020 but was down 20.6 percentage points from 2019. Overall, cost control and higher demand helped Marriott deliver adjusted EPS of $3.19 in 2021, reflecting a significant jump from $0.18 in 2020.

As of December 31, 2021, Marriott’s development pipeline comprised 2,831 properties with nearly 485,000 rooms. Notably, over half of the rooms in the pipeline are outside the U.S. and Canada.

Marriott’s management feels that the reopening of additional markets and a return of employees to the office will drive robust ADR, sustained leisure demand, and improvements in business trips. The company also expects to benefit from growth in visits that blend business and leisure, and international travelers getting back on the road.

Following a recent meeting with Marriott’s management, Morgan Stanley analyst Thomas Allen told investors that management reiterated confidence about meaningful improvements in 2022 RevPAR compared to the 19% decline in 4Q21’s RevPAR vs. 2019.

The analyst stated, “The company is seeing extremely strong bookings into Europe from Americans this summer, Presidents’ Day RevPAR was up double digits, and group business is continuing to pick up. Blended trip purpose should help offset standalone corporate headwinds.”

Allen reiterated a Hold rating and a price target of $172.

The Street is also sidelined on Marriott, with a Hold consensus rating based on three Buys and nine Holds. The average Marriott price target of $177.36 implies 9.18% upside potential from current levels.

Conclusion

Revenues of Wyndham, Hilton, and Marriott improved in 2021 from 2020, but the figures are still below pre-pandemic levels.

While the three hotel stocks are down year-to-date, analysts are highly bullish on Wyndham, compared to Hilton and Marriott, and hence see higher upside potential in the stock over the next 12 months. Wyndham’s extensive presence in the economy and midscale hotels space, heavy dependence on leisure bookings, and lower exposure to business travel look favorable under current circumstances.

Discover new investment ideas with data you can trust.

Read full Disclaimer & Disclosure.