US cannabis stocks have been on a tear recently, finally shaking off a difficult year which has seen share prices plunge across the board since the year’s early highs.

However, the rally has excluded the cannabis industry’s leading SaaS provider WM Technology (MAPS). Moreover, the company’s disappointing Q3 results saw the stock go against the recent trend, with shares nosediving by 20% following the release of the quarterly statement.

While non-GAAP EPS of $0.04 came in above the consensus estimate of $0.01, revenue hit $50.9 million, below the Street’s call for $51.7 million, and amounting to 9% year-over-year growth, slowing down from 21% in the prior quarter.

There was also deceleration for US revenue growth which dropped sequentially from 55% to 46%, driven by legal operators struggling to compete against illicit operators, particularly in California.

This is also having an impact on the outlook; the company expects Q4 adjusted EBITDA of $3.0 million-$5.0 million and revenue between $50 million to $52 million. Consensus had $59.4 million.

“Despite the negative impact of the shift toward illicit markets in certain states,” says JMP’s Patrick Walravens, “WM Technology still grew its U.S. business 46% in 3Q, and the company guided to full-year 2022 growth in the high-30% range, which we believe underscores a number of attractive elements of this story.”

These include the fact that the company’s two-sided marketplace for consumers and dispensaries, Weedmaps, is the leading offering for the legal cannabis industry while the company also boasts its connected solution for businesses, WM Business.

There is also a large TAM (total addressable market) to cater to and one that will only expand; from $2.2 billion at present, according to Walravens, to $5.7 billion by 2025.

Additionally, in a heavily regulated industry, there’s ample opportunity for a cloud-based solution that abides by federal, local, and state regulations. Walravens is also a fan of CEO Chris Beals and CFO Arden Lee’s “thoughtful professional leadership.”

“Most importantly,” says the 5-star analyst, “While the implementation is messy at times, the increasing legalization of cannabis should be a powerful growth driver for WM Business over time, with states like New York and New Jersey recently legalizing cannabis and with a potential new Republican-led bill seeming to increase the chances of the federal legalization of marijuana.”

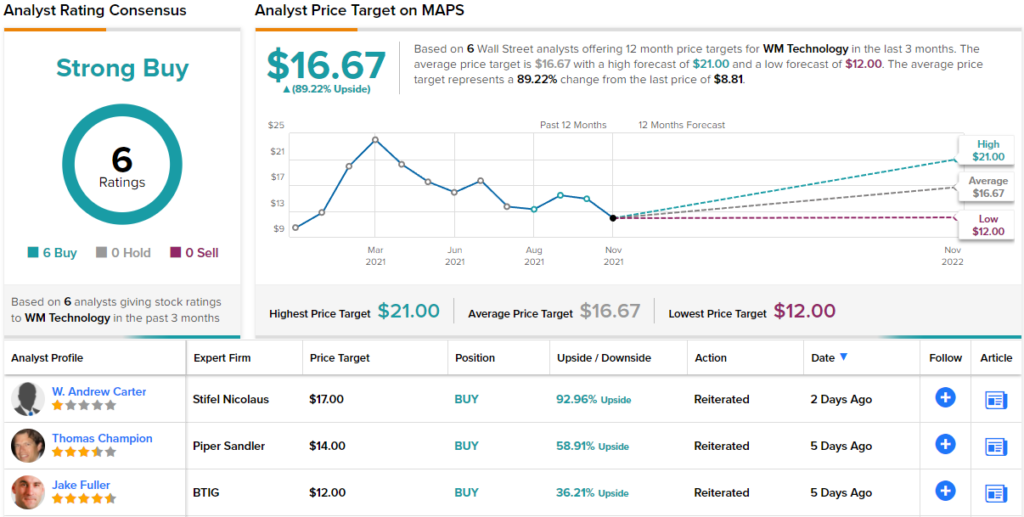

To this end, Walravens reiterated a Buy rating on WM Technology shares, backed by a $21 price target. Investors stand to score ~138% gain, should Walravens’ thesis go according to plan in the year ahead. (To watch Walravens’ track record, click here)

Walravens’ colleagues unanimously agree; all 5 other recent reviews are positive, culminating in the stock’s Strong Buy consensus rating. While the average target is not as exuberant as the JMP analyst’s, at $16.67, the figure still offers 12-month upside of 89%. (See MAPS stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.