By instinct, investors concerned about a possible recession on the horizon typically turn to discount retailers. Unfortunately, many businesses in this segment have been disappointing, except for a few outperforming entities like Ollie’s Bargain Outlet (NASDAQ:OLLI). What’s even more enticing is that Ollie’s has the right fundamentals to continue marching higher. Therefore, I am bullish on OLLI stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

A Terrible Irony Afflicts OLLI’s Rivals

One factor that benefits OLLI stock over its rivals is a cynical one: popular discount retailers have been spooking investors rather than reassuring them. It all centers on a terrible irony that afflicts Ollie’s competition.

From a topical glance, the discount retail segment should be thriving. While the U.S. economy managed to pick itself up from the worst of the COVID-19 crisis, soaring inflation remains stubbornly sticky, to borrow a phrase from TipRanks reporter Vince Condarcuri. Therefore, the Federal Reserve may have little choice but to be vigilant about its interest hiking campaign.

Of course, such a measure puts tremendous pressure on consumer sentiment. Generally, higher borrowing costs lead to disincentivized business expansion, in turn leading to layoffs. As a result, consumers themselves have every incentive to save money. So, it’s easy to see why OLLI stock has soared this year.

However, the same cannot be said about dollar-store operator Dollar General (NYSE:DG). It’s down sharply since the January opener, raising alarming questions. Fundamentally, the issue here stems from its declining gross profit margin. Pressured to compete against its direct rivals, Dollar General appears to have sacrificed profitability for revenue. Still, it’s the drive to provide discounts – the core business model of Dollar General – that has investors anxious.

The same can be said about Dollar Tree (NASDAQ:DLTR). Its gross margin has faded, likely in response to competitive challenges. Unfortunately, what seemed like a viable idea at the beginning of this year has turned out to be a trainwreck. On the flipside, OLLI stock managed to avoid the mess.

Where Ollie’s Bargain Outlet Distinguishes Itself

Naturally, the question that comes up is, why is OLLI stock performing so swimmingly, whereas its rivals are drowning? The answer comes down to gross profit margins. Ollie’s is able to generate robust demand without sacrificing key profitability metrics.

In the quarter ended July 2023, Ollie’s posted revenue of $514.51 million, up nearly 14% against the year-ago tally of $452.48 million. Its gross profit came out to about $197 million, leading to a gross margin of 38.2%. That’s significantly higher than the gross profit of almost $144 million or a gross margin of 31.7% in the year-ago quarter.

In contrast, investors are seeing gross margin contraction in Dollar Tree and Dollar General. That’s one of the main reasons why the market has difficulty trusting in DLTR or DG. If these companies continue to sacrifice profitability metrics for revenue growth, the business may become untenable.

As well, retailers – whether they serve premium or discounted products – must consider the total addressable market. If mass corporate layoffs continue to accelerate, fewer dollars will be available, even for critical goods. That’s why it’s not necessarily a great idea to sacrifice profitability. At the very least, it leaves such entities with less margin for error if circumstances really go awry.

A Critical Technical Standoff

Now, in all fairness, a key concern about OLLI stock is that it’s gone up so far, so fast. Since the beginning of the year, OLLI has gained about 62%. Naturally, prospective investors are worried about holding the bag.

To be sure, a critical technical standoff may be at play. Currently, shares trade at a little bit under $76. Therefore, the natural psychological target clocks in at $80. Coincidentally, open interest in the Oct 20 ’23 80.00 call option jumped sharply on September 18.

On the other side, a major trader wrote (writing refers to selling a contract without owning it) 801 contracts of said call option on the aforementioned date. Because the trader is writing the options, this party is taking the opposite side of the wager.

Should market forces drive OLLI stock above the $80 strike price significantly, the bearish trader would be obligated to sell OLLI at the strike, assuming the countervailing parties exercise the call. The higher OLLI swings up, the likelier a panic materializes to cover the liability. Thus, on a net basis, should emotions take over, that’s a positive for the stock.

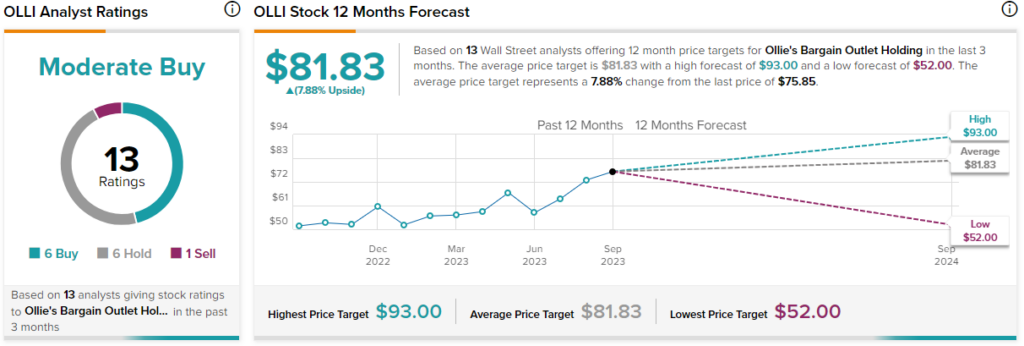

Is OLLI Stock a Buy, According to Analysts?

Turning to Wall Street, OLLI stock has a Moderate Buy consensus rating based on six Buys, six Holds, and one Sell rating assigned in the past three months. The average OLLI stock price target is $81.83, implying 7.9% upside potential.

The Takeaway

Unlike Ollie’s competitors, the company continues to build upon the top line and bolster the bottom through higher gross margins. That gives the retailer a significant cushion should economic circumstances worsen. Therefore, the prime positioning drives confidence in OLLI stock. Also, a technicality in the options market could cause OLLI stock to rise, assuming it gets past $80 first.