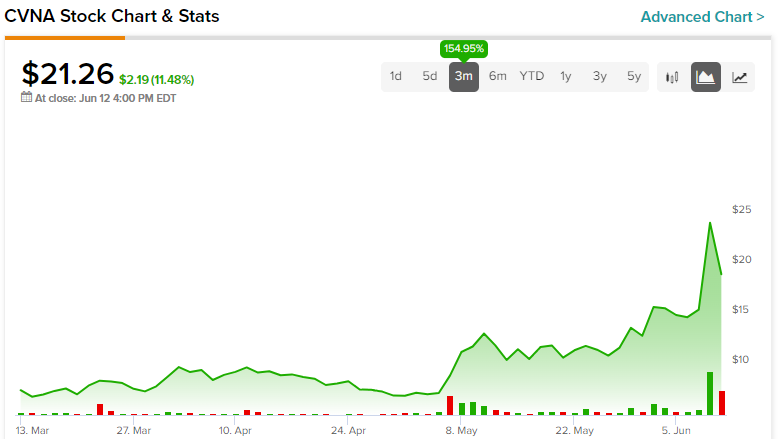

Simply judging by last Thursday’s 56% pop in Carvana (NYSE:CVNA) shares, investors might assume the online used-car retailer stands poised for a comeback. While the bullishness centered on management’s upgraded second-quarter outlook, the encouraging disclosure might not substantively change the broader narrative. Therefore, I am bearish on CVNA stock.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

CVNA Stock Seems Enticing on the Outside

Without diving into the details, a cursory look at CVNA stock suggests a justification for believing in its sustained upside trajectory. After all, from the beginning of the year, shares have skyrocketed by over 350%. Moreover, the renewed enthusiasm for Carvana has reversed its trailing-year loss, with the stock now sitting on a 1% gain for that period.

Further, the details of its Q2 outlook lift warrant consideration. As TipRanks reporter Shrilekha Pethe stated, management raised expectations for adjusted EBITDA to above $50 million. In addition, the leadership team projects that adjusted total gross profit per unit (GPU) will land above $6,000. Not only would this forecasted tally represent a 63% year-over-year gain, but it would also be a new company record.

Carvana Founder and CEO Ernie Garcia stated, “Our record-breaking 2023 first quarter is evidence that our strategy is working, and our updated Q2 2023 outlook demonstrates that our progress continues to positively impact the business even faster than expected.”

While impressive, it’s also worth noting that at around $21 per share, CVNA stock sits well below its all-time high of above $370. Not only that, but just before the pandemic, CVNA stock stood at around $110. Basically, Carvana will need plenty of things to go just right to regain lost credibility.

However, moving forward, CVNA stock faces substantial headwinds. Primarily, the consumer economy suffers from stubbornly-high inflation along with elevated borrowing costs. Naturally, these two factors will cut into buyer sentiment for expensive products like vehicles.

To be fair, personal transportation is a must-have in many regions. Nevertheless, Carvana must charge a premium for its online service convenience, putting it at a competitive disadvantage.

One Good Quarter Likely Won’t Change Everything

Undeniably, it’s far better for Carvana to issue an outlook upgrade than the other way around. However, assuming that the company does make good on its raised guidance, one good quarter probably won’t change everything. Moreover, it’s important to realize that just a little over a year ago, the company succumbed to accepting unfavorable financial terms just to stay afloat.

According to an April 2022 report by The Wall Street Journal, Carvana – after struggling to sell bonds – turned to Apollo Global Management (NYSE:APO) for a $1.6 billion financing agreement. According to the news agency, the yield on the underlying bonds came out to 10.25%, well above average for most junk bonds.

Just as problematic, Carvana struggles with a massive debt load. Based on its balance sheet as of Q1 2023, the company has $7.05 billion of long-term debt on its books. On the other hand, its cash and cash equivalents amount to only $1.01 billion.

Moving forward, Carvana will face competition from both traditional auto dealerships along with private sellers. Since neither entity must deal with deliveries as a core part of their business, they can undercut Carvana. Further, the online auto specialist lacks the pandemic-related catalyst that dramatically incentivized the contactless nature of its main business model.

An Additional Credibility Woe to Consider

Interestingly, a recent Reuters report noted that “Carvana has been trimming inventory and slashing advertising expenses to help move closer to profitability and attain positive free cash flow.” However, achieving positive free cash flow (FCF) may be easier said than done.

From 2020 to 2021, the red ink on Carvana’s free-cash-flow line expanded unfavorably from $968 million to $3.15 billion. True, in 2022, the loss in FCF came down to $1.79 billion. As well, in Q1 2023, the metric was down to a loss of $86 million. However, as Carvana plows headfirst in troubling economic circumstances – such as mass layoffs involving high-paying jobs – the ambition for positive FCF may be illusory.

Is CVNA Stock a Buy, According to Analysts?

Turning to Wall Street, CVNA stock has a Hold consensus rating based on two Buys, 14 Holds, and one Sell rating. The average CVNA stock price target is $12.67, implying 40.4% downside risk.

The Takeaway: CVNA Stock Must Win the Season, Not Just a Game

While the raised guidance for Q2 buoyed sentiment, it’s critical to remember that CVNA stock has a long road ahead. Primarily, Carvana entered into an unfavorable financing agreement that may prove costly. In addition, the underlying consumer economy isn’t of much help. Therefore, investors should approach this story with extreme caution.