Caterpillar stock (NYSE:CAT) can keep rising despite fears of a possible slowdown in growth. The heavy machinery, construction, and mining equipment giant had a phenomenal 2023, with the stock hitting new all-time highs once its full-year results came out. Following a year of impressive sales and earnings growth, 2024 is anticipated to be a period of consolidation for the company. However, this doesn’t rule out the possibility of further share price gains. For this reason, I remain bullish on CAT stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

FY2023: The Best Year in Caterpillar’s History

Before I discuss why Caterpillar stock may be poised for further upside, let me start by adding some color regarding the company’s recent performance. Fiscal 2023 wasn’t just a good year for the company but arguably the best in its history, as Caterpillar excelled across every aspect of the business.

In particular, last year witnessed Caterpillar achieving unprecedented milestones, including record-breaking sales, margins, profits, and capital returns to shareholders. All this was accomplished while navigating one of the most challenging macroeconomic environments in recent history.

To sum it up, for FY2023, the company posted:

- Record total sales of $67.1 billion, up 3% year-over-year, including Services revenues of $23 billion, also a record, up 5% year-over-year.

- A record gross profit margin of 31.7%, up from 26.2% in fiscal 2022.

- A record adjusted operating profit margin of 20.5%, a 510 basis point increase over the prior year.

- Record adjusted EPS of $21.21, a 53% increase over 2022.

- Record free cash flow of about $10 billion.

- Record capital returns to shareholders of about $7.5 billion.

Seeing such jaw-dropping numbers from a company that is typically subject to cyclical trends is quite remarkable, especially considering the heightened macro-related volatility experienced in 2023.

The truth, however, is that Caterpillar is enjoying robust industry tailwinds. The construction equipment and heavy machinery industry is benefiting significantly due to record infrastructure investment, mainly backed by unprecedented government spending. In turn, this is driven by the 2021-approved $1.2 trillion bipartisan infrastructure bill, which mainly concerns infrastructure projects. Being the largest player in the industry, Caterpillar appears to be the main beneficiary of this trend.

Can Caterpillar’s Momentum Last in 2024?

The first question you have as an investor seeing such spikes across Caterpillar’s financials is whether this momentum can be sustained. Based on management’s outlook for the year, it appears that extraordinary demand for Caterpillar’s machinery and equipment is set to be sustained, fueled by continued spending on infrastructure. However, it also seems that headwinds are set to offset some of Caterpillar’s strengths.

Caterpillar’s management laid out all potential factors in its most recent earnings call, which I have summed up for your convenience.

In particular, on the one hand, management expects the following tailwinds:

- North America’s construction industries to remain healthy, driven by strong government infrastructure spending,

- Latin America to see increased construction activity due to improved financial conditions,

- The Middle East to contribute strongly to machinery demand,

- The overall trend of the energy transition to support long-term growth opportunities,

- Reciprocating engines and services in oil and gas to show a slight increase,

- High-speed marine transportation sector to experience a slight increase as well.

On the other hand, these catalysts are likely to be offset by some road bumps. These include:

- Economic softening in Asia Pacific,

- China’s above-10-ton excavator industry remaining at a low level,

- Economic uncertainty in Europe,

- Anticipated decrease in machine volume, especially in off-highway and articulated trucks,

- Lower order rates, as customers exercise capital discipline,

- Softening industrial demand in the Energy & Transportation division of the company,

- Short-term moderation in well servicing in North America’s oil and gas sector.

As a result, while the main catalyst driving Caterpillar’s revenues and earnings to such great levels isn’t going away (infrastructure spending), any potential favorable developments might be counterbalanced by certain headwinds.

Thus, consensus revenue and EPS estimates for 2024 point toward $67.4 billion and $21.01, implying a change of 0.5% and -0.6%, respectively. Essentially, Wall Street anticipates flat numbers year-over-year.

Is a Stagnation in Sales and Earnings Growth Bad for the Stock?

While Caterpillar’s sales and earnings growth is expected to slow down/stagnate this year, this is not necessarily bad for the stock. Sure, top and bottom-line growth are always solid catalysts for a stock to rise. But it’s not further growth that could fuel the upside in this case. Rather, it’s the stock’s attractive valuation.

Caterpillar’s stock, as strange as it may sound, hasn’t surged to the extent of becoming overvalued. While the stock rallied by 23.4% in the previous calendar year, its adjusted EPS surged by a far more substantial 53% during the same period.

Even in the face of Caterpillar’s robust performance in the year-to-date rally of 2024, the stock is still trading at a reasonable 15 times this year’s anticipated earnings. One could argue that this is a hefty multiple for a cyclical company during a peak earnings cycle.

However, strong industry catalysts, including the outlook that strong infrastructure investments will last for several years, indicate the potential for a mega-cycle. Thus, earnings are poised to remain at or near record levels over the medium term. Coupled with robust capital returns, I believe that the stock is primed for further upside.

Is CAT Stock a Buy, According to Analysts?

Regarding Wall Street’s view on the stock, Caterpillar has a Moderate Buy consensus rating based on seven Buys, nine Holds, and two Sells assigned in the past three months. At $314.76, the average Caterpillar stock forecast implies 0.6% downside potential.

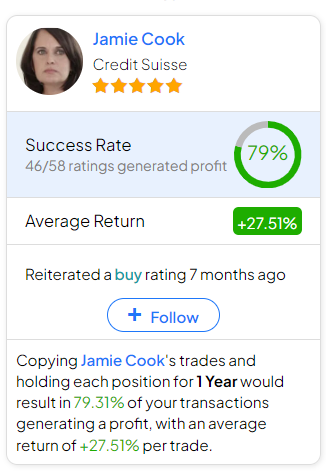

If you’re wondering which analyst you should follow if you want to buy and sell CAT stock, the most accurate analyst covering the stock (on a one-year timeframe) is Jamie Cook from Credit Suisse, with an average return of 27.51% per rating and a 79% success rate.

The Takeaway

In wrapping up, Caterpillar had a stellar 2023, achieving record-breaking sales and profits despite a rather tough macro environment. Moving into 2024, the company might face some headwinds in some markets, but with infrastructure spending set to remain robust, its earnings should remain near record levels.

Even if growth takes a breather, the stock’s current valuation seems fair. So, while we might not see the stock repeat its previous rally, I’m staying optimistic about its future returns.