Shares of Apple (AAPL) have been leading the markets higher over the past few weeks, now up around 21% from their bottom of around $129 per share. With quarterly earnings up ahead, it will be “make or break” for its latest relief rally. Fortunately, management already cautioned of supply-chain constraints as a result of China’s COVID-19 restrictions and the impact of lost sales from a Russian pullout.

Undoubtedly, Apple is a dominant force in the premium smartphone market. While the smartphone market’s growth isn’t as hot as it used to be, Apple has found a way to take meaningful share away from its rivals to keep its iPhone growth alive.

Over time, I expect Apple to continue taking share en route to becoming an even more dominant force in smartphones. Meanwhile, the company is hard at work on its next big device (likely an augmented-reality headset) that could gradually replace the smartphone as we know it.

Though the lower-cost, higher-value options have found a spot with cost-conscious consumers, it’s the higher-end where Apple is really starting to shine. Reportedly, Apple’s first-quarter share of the premium smartphone market (devices whose cost exceeds $400) has grown to 62%, up from 57% over the same period last year.

Apple is giving its competitors a squeeze, thanks to the rapid pace of innovation in hardware and the growing lineup of ultra-popular services.

Indeed, Apple is firing on all cylinders, and the pace of innovation could pick up with the rumored unveiling of its mixed-reality headset less than a year away.

Apple’s Services Push is Far From Over

Apple has done a marvelous job of bringing out the most of its services business. With the Apple One bundle, which includes fitness, music, video, cloud storage, news, video games, and other perks, the company offers those within its walled garden (or ecosystem), providing unmatched value.

In prior pieces, I noted that the services bundle was a thorn in the side of its competitors. Though Apple has come a long way with its services, it’s not about to slow down anytime soon. The company is on the cusp of squeezing various fintech firms with Apple Pay innovations. Apple Pay Later, other digital bank-like features, and a hardware-as-a-service subscription could take services to the next level.

Such “sticky” high-margin services could easily warrant even more multiple expansion on the stock. Today, AAPL stock trades at just shy of 25.5 times trailing earnings. Sure, its price-to-earnings multiple is near a historical high point. However, given how much its Services segment can grow, such a multiple may not be large enough.

Apple’s Pace of Hardware Innovation is Remarkable

Beyond services, Apple is making significant strides with its hardware iterations. Undoubtedly, the iPhone has not changed a heck of a lot over the past three years. The design is virtually the same, with the notch seemingly shrinking with new iterations.

Though the design of the latest and greatest iPhone hasn’t really had a big jump since the iPhone X was unveiled several years ago, there have been phenomenal innovations underneath the hood.

In terms of hardware, the iPhone continues to put many rivals to shame, with all-day battery life and A-series chips that raise the bar every single year. As Apple Silicon continues to widen the gap, the iPhone could leave competitors in the dust as it goes after the now mature smartphone market.

Apple’s profoundly powerful hardware doesn’t stop at the iPhone. Its M-series chips have made the Mac computer compelling again, even as the design took a blast from the past. The newest line of Macs did away with the problematic butterfly keyboard and swapped it for the traditional one.

Physical function keys also replaced the touch bar. The latest Macs certainly resemble the ones from many years ago, but underneath the hood, the Mac could not be more different. It’s easily one of the most powerful computers out there. As Apple continues raising the bar on per-watt performance, I’d look for the Mac to give PCs a bigger run for their money.

Finally, cutting-edge hardware will help Apple smoothen the transition into the metaverse. Its coming headset is rumored to be powered by the M2 chip currently in the latest Macs.

As Apple continues to deliver jaw-dropping performance with every iteration, it seems likely that the AR/VR headset market is for Apple to take. Watch out, Meta Platforms (META).

Wall Street’s Take on AAPL Stock

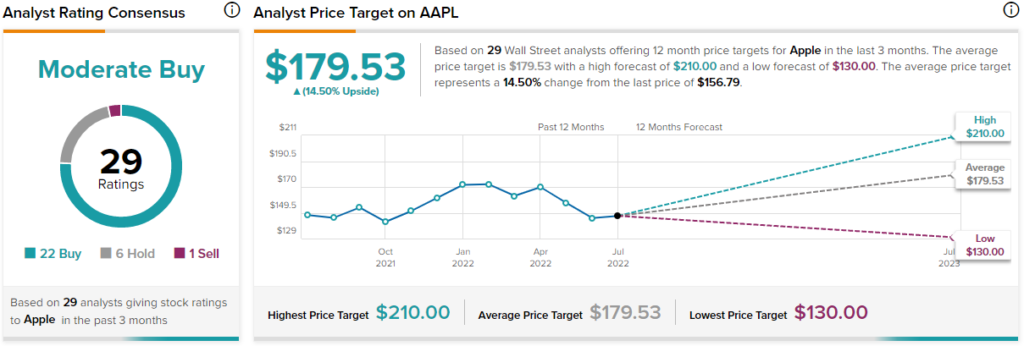

Turning to Wall Street, AAPL stock comes in as a Moderate Buy. Out of 29 analyst ratings, there are 22 Buys, six Holds, and one Sell.

The average Apple price target is $179.53, implying upside potential of 14.5%. Analyst price targets range from a low of $130.00 per share to a high of $210.00 per share.

Conclusion: High-Margin Growth Could Lead to a Valuation Expansion

Apple strives to offer the very best hardware, software, and services. On the hardware front, Apple’s iterations could lead to meaningful share-taking across all product categories. Further, an aggressive services push could lead to high-margin growth that calls for even more multiple expansion in the stock.

Finally, it’s not just existing hardware where Apple will be dominant. With the very best hardware, Apple could become a force to be reckoned with as it looks ahead to next-generation hardware – think mixed-reality headsets and electric vehicles (EV).

Apple is doing everything right. As the firm looks to pull the curtain on a headset in a potential recession year (2023), look for Apple to beat the S&P 500 (SPX) by leaps and bounds. Apple stock is the market leader again — and it deserves to be.