As Abercrombie & Fitch (ANF) gears up for its second-quarter earnings report, there’s a lot of anticipation around the company’s expected strong performance. However, with high expectations and significant bullish momentum, the market reaction could be volatile—leading me to maintain a “Hold” stance on the stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Abercrombie Demonstrates Impressive Performance

Abercrombie & Fitch’s impressive performance over the past year, despite challenging market conditions, is a key reason why I am neutral rather than bearish on the stock. The company’s success in aligning its styles with consumer preferences and effectively managing inventory has been remarkable, with last quarter’s 20% sales increase highlighting its strengths.

However, as we approach the Q2 earnings report on August 28th, I maintain a neutral stance because the stock has surged to near all-time highs following a substantial triple-digit gain in less than a year. While the company’s strong performance is commendable, these high expectations are likely already priced into the stock. Consequently, even if Abercrombie & Fitch reports impressive results, it may not be sufficient to propel the stock further, leading me to adopt a cautious outlook.

Abercrombie & Fitch Turns Around From Challenges

Although I currently hold a neutral stance on Abercrombie & Fitch ahead of its earnings report, it’s important to take a step back and understand how the company’s remarkable turnaround has enabled it to accelerate its sales significantly and maintain such strong bullish momentum.

If you had invested in Abercrombie & Fitch exactly one year ago, your return would have surpassed even that of Nvidia (NVDA), the tech stock of the moment. Indeed, Abercrombie & Fitch has become one of the most remarkable turnaround stories, not just in retail but in the stock market overall, with its stock price soaring over 235% in the past twelve months.

But stepping back a bit, over the last five years, Abercrombie & Fitch faced several challenges, including declining profits and brand confusion due to the similarities between its Abercrombie and Hollister products, which led to cannibalization. The company’s management responded by shifting focus from younger, trend-driven consumers to targeting an older demographic, specifically young Millennials.

The company also adeptly navigated the pandemic’s challenges by closely monitoring and adjusting its inventory. This approach allowed Abercrombie & Fitch to significantly reduce its stockpile and quickly adapt to changing market trends. By moving away from traditional storefronts and adopting a consumer-centric approach, Abercrombie & Fitch achieved a strong comeback, reporting its highest quarterly net sales in over a decade by May 2023.

Historically, Abercrombie & Fitch’s sales growth was modest, with a 3% average growth in the past five years. However, this shifted dramatically to 15.8% in 2023. The company also managed to increase its pricing, raising the operating margin from 3.8% in 2019 to a trailing 13.1%.

Now, zooming in on the most recent quarter (Q1), Abercrombie & Fitch posted a standout 21% year-over-year sales increase, up from the 16% growth in Q4 and the 3% growth in Q1 of the previous year.

Given these developments, the management’s revised FY2024 revenue guidance of 10% year-over-year growth—up from the previous guidance of 5%—seems reasonable. This new guidance builds upon the impressive 16% growth seen in 2023.

ANF’s Momentum May Be Challenging to Sustain

Much of my neutral stance on Abercrombie & Fitch ahead of its earnings report stems from the stock’s strong bullish momentum, which may be challenging to sustain.

Nevertheless, the optimism surrounding Abercrombie & Fitch’s upcoming earnings report, is largely driven by the company’s robust guidance for both quarterly and annual sales growth. To beat market expectations, Abercrombie & Fitch will need to report EPS above $2.22 and revenues exceeding $1.1 billion.

Management expects net sales for Q2 to increase in the mid-teens compared to the $935 million reported for the same period in fiscal 2023. In addition, on the profitability front, Abercrombie & Fitch projects an operating margin between 13% and 14%, up from 9.6% in Q2 2023.

Moreover, a key point to consider is the company’s strategy of raising Average Unit Retail (AUR) prices—essentially, selling prices—which began in Q2, along with intensifying customer acquisition across various demographics. If executed successfully, these strategies could boost profitability and support long-term growth. Nonetheless, careful execution will be necessary to avoid alienating existing customers or misjudging market demand. Listening to management’s insights on these strategies during the Q2 report will be crucial.

Given the high stakes of the upcoming earnings report—especially after the stock has surged by triple digits over the past year—Abercrombie & Fitch trades at a price-to-sales ratio of 1.94x, more than double its average over the last five years. Although this multiple may be justified by recent impressive results, it leaves less room for error.

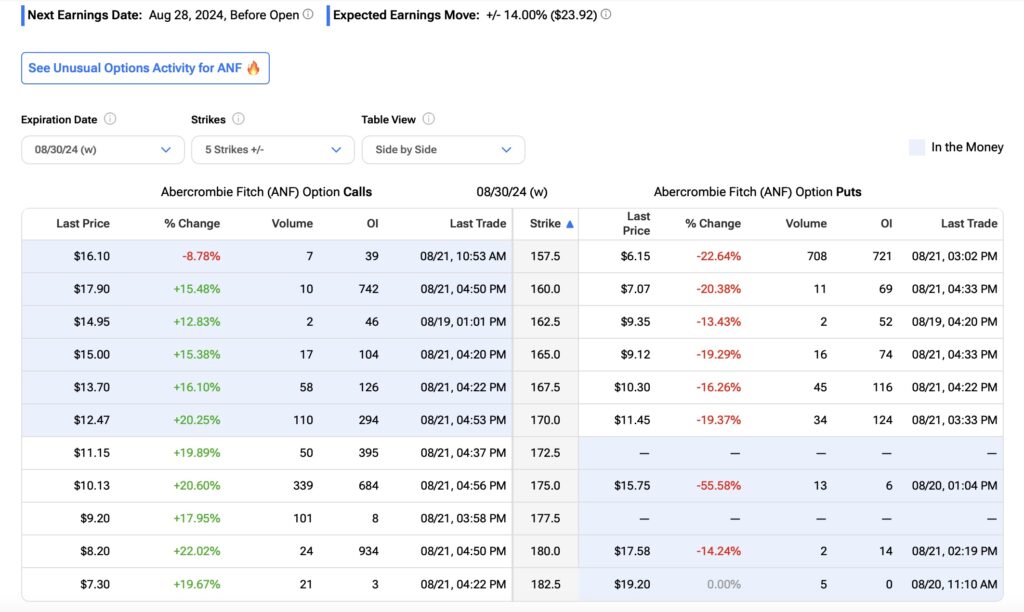

This cautious sentiment is reflected in Abercrombie & Fitch’s options chain. The “at-the-money” straddle for the options closest to expiration after the earnings announcement implies a potential 14% move, either up or down, for ANF stock. This is based on a $170 strike price, with call options priced at $12.47 and put options at $11.45.

Is ANF a Buy, According to Wall Street Analysts?

Despite the “Moderate Buy” consensus rating among Wall Street analysts, there are more neutral than bullish stances on Abercrombie & Fitch. Five out of eight analysts have a “Hold” rating on ANF, while the remaining three have a “Buy” rating.

Notably, even the neutral analysts, such as Citi’s (C) Paul Lejuez, have raised their price target ahead of the earnings report, increasing it from $150 to $190. Overall, the average ANF price target is $186.29, which suggests an upside potential of 10.23% from the current price level.

Key Takeaways

In summary, while I maintain a “Hold” stance on Abercrombie & Fitch, the company is expected to deliver strong Q2 earnings that could sustain its bullish momentum. However, given the stock’s significant surge and the high expectations already priced in, volatility poses a considerable risk. With current elevated valuations, any investment at this point ahead of earnings may be speculative, in my view.