5G or the fifth generation of wireless technology is in demand due to its higher speed and lower latency (the time required for a set of data to travel between two points). While macro pressures might impact near-term demand, long-term prospects look bright due to increased opportunities for artificial intelligence and Internet of Things (IoT) on 5G. We used TipRanks’ Stock Comparison Tool to place network providers Verizon (NYSE:VZ), AT&T (NYSE:T), and T Mobile US (NASDAQ:TMUS) against each other to pick the most attractive 5G stock.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Verizon Communications (NYSE:VZ)

Verizon recently reported Q4 2022 adjusted earnings per share (EPS) of $1.19, which was in line with analysts’ expectations but declined 10.5% from the prior-year quarter. It expects wireless service revenue growth between 2.5% and 4.5% in 2023, reflecting a slowdown compared to 8.6% in 2022.

Verizon’s wireless postpaid phone net additions came in at 217,000 (down 61% year-over-year) in Q4, of which 176,000 were from the Business group. Meanwhile, the Consumer business reported 41,000 wireless postpaid phone net additions following losses in the first three quarters of 2022 due to intense competition. Meanwhile, the company lost 175,000 wireless retail prepaid customers in Q4.

On the positive side, total broadband net additions were a solid 416,000, including 379,000 fixed wireless broadband net additions. Given challenging business conditions, the company aims to drive more efficiencies and deliver cost savings in the range of $2 billion to $3 billion annually by 2025.

Is VZ a Good Stock?

Following the print, RBC Capital analyst Kutgun Maral lowered his price target for Verizon stock to $40 from $42 but maintained a Hold rating. Maral noted that Q4 results and 2023 guidance point to growing headwinds across wireless service and wireline revenue, margins, and free cash flow.

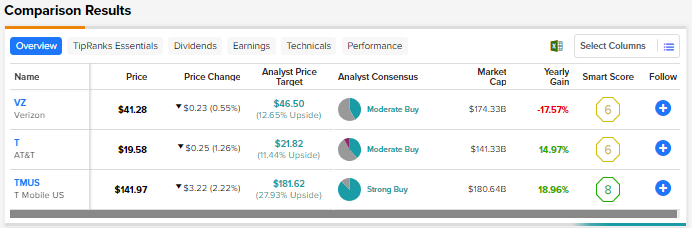

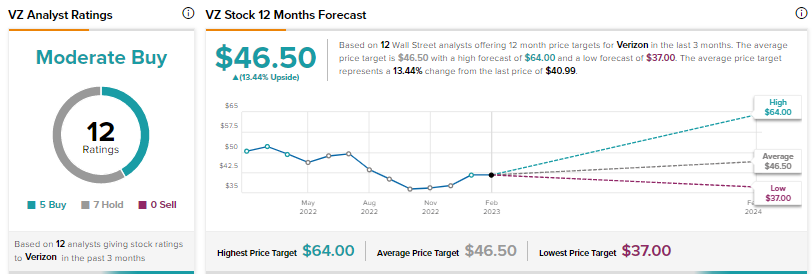

Wall Street is cautiously optimistic about Verizon, with a Moderate Buy consensus rating based on five Buys and seven Holds. The average VZ stock price target of $46.50 implies 13.4% upside potential. Shares have advanced nearly 5% so far in 2022.

AT&T (NYSE:T)

AT&T delivered market-beating Q4 2022 earnings, with adjusted EPS increasing 9% to $0.61. Revenue grew 0.8% to $31.3 billion but slightly lagged estimates. The company expects to generate free cash flow of at least $16 billion in 2023, up from $14.1 billion in full-year 2022. AT&T’s domestic wireless service revenue grew 5.1% in 2022 and the company expects to deliver a growth of 4% or higher this year.

AT&T reported 6.4 million wireless net additions in Q4, including 1.1 million postpaid net additions. The quarter saw 656,000 postpaid phone net additions. During the Q4 earnings call, the company highlighted that its postpaid phone base has increased by nearly 7 million to 69.6 million subscribers over the past 2.5 years.

The company intends to continue its 5G expansion, reaching over 200 million people with mid-band 5G by 2023-end. It also assured investors that it is on track to achieve $6 billion plus cost savings run rate target by the end of this year.

Is AT&T a Buy, Sell, or Hold?

Ahead of the results, Wells Fargo analyst Eric Luebchow upgraded AT&T to a Buy from Hold and raised the price target to $22 from $17. The analyst views the U.S. telecom sector as a relatively defensive play for 2023 and called AT&T his top wireless pick. Luebchow is bullish about the company as he sees upside potential to EBITDA and free cash flow consensus estimates, improving balance sheet, and reasonable valuation compared to Verizon.

Wall Street’s Moderate Buy consensus rating for AT&T is based on five Buys, seven Holds, and one Sell. The average AT&T stock price target of $21.82 suggests 11.4% upside potential. Shares are up 6.2% year-to-date.

T Mobile US (NASDAQ:TMUS)

T Mobile’s Q4 revenue fell 2.5% to $20.3 billion and missed analysts’ expectations. However, the company’s EPS jumped to $1.18 from $0.34 in the prior-year quarter and topped the Street’s estimates. Postpaid net customer additions were 1.8 million in Q4 2022.

It’s worth noting that the company’s postpaid phone net customer additions came in at 927,000 in Q4, outperforming Verizon and AT&T. Furthermore, prepaid net customer additions were 25,000 and high-speed internet net customer additions were 524,000. The company’s 5G network now covers 325 million people or 98% of Americans, while it’s Ultra Capacity 5G reaches 265 million people nationwide.

T Mobile expects postpaid net customer additions in the range of 5 million to 5.5 million this year, hoping to lead the industry for the 9th consecutive year. The company expects cost savings of $7.2 billion to $7.5 billion this year due to synergies from its 2020 merger with Sprint.

What is the Target Price for TMUS Stock?

Following the Q4 results, Morgan Stanley analyst Simon Flannery reiterated a Buy rating for T Mobile US and a price target of $175, citing the company’s “encouraging” outlook for 2023. The analyst stated that the company remains his Top Pick in the telecom services space.

Flannery highlighted that T Mobile US continues to see “significant runway for growth from rural, enterprise and FWA [fixed wireless access] opportunities, while providing reassurance around industry slowdown, macro pressures and potential fiber ambitions.”

Wall Street’s Strong Buy consensus rating for T Mobile US is based on 14 Buys and two Holds. The average TMUS stock price target of $181.62 suggests nearly 28% upside potential. Shares are up by a modest 1.4% so far in 2023 but have outperformed Verizon and AT&T over the past year.

Conclusion

Macro headwinds could hurt 5G companies over the near-term and subscriber additions could slow down this year. Nevertheless, long-term prospects for 5G companies seem solid. Unlike T Mobile US, Verizon and AT&T offer attractive dividend yields of 6.3% and 5.7%, respectively. That said, analysts are more bullish about T Mobile US than Verizon and AT&T and see higher upside potential in the stock.