Are the markets heading up or down? Frankly nobody knows, with some experts saying the next leg is down again and others calling for further upside. Finding the solution to this conundrum, one financial prognosticator thinks the markets will do both. Wells Fargo’s head of equity strategy Chris Harvey thinks the S&P 500 could reach 4,200 this year, but not before it posts a decline from current levels to around 3,400. That’s a 15% drop, but from there it will swing 20% higher.

Harvey’s outlook is based on the idea that we are in something more akin to an “economic malaise” rather than a full-on recessionary environment, believing that what’s to come is “not something that’s going to be horrific.” So, essentially, plenty of volatility followed by a big move up.

Meanwhile, Harvey’s analyst colleagues at Wells Fargo have been tracking down the equities that are primed to flourish in such an environment. They have homed in on two names they like the look of. Are other analysts feeling the same way? We’ve ran these tickers through the TipRanks database to find out. Here are the details.

O-I Glass, Inc. (OI)

Our first Wells Fargo pick is glass bottle maker O-I Glass. The company is one of the world’s largest glass container manufacturers with roughly half the glass containers across the globe made by O-I, or one of its affiliates and licensees. Tracing its roots all the way back to the early 1900’s, the company operates throughout the Americas, Europe, and Asia Pacific, catering to clients in the food, beer, wine, spirits and non-alcoholic beverages segments.

Glass packaging might not sound like much of an exciting sector but that will matter little to investors as the stock entirely sidestepped last year’s bear, generating handsome gains of 38% in the process.

In the last reported earnings – for 3Q22 – revenue climbed by 5.6% year-over-year to $1.7 billion, beating the Street’s call by $50 million. Adj. EPS of $0.63 also came in ahead of the $0.61 consensus estimate. Beating Street expectations on the profitability profile has become something of a habit over the past couple of years – the company has achieved this feat in nine of the last 10 quarters. For Q4, OI raised its adjusted earnings outlook from the range between $0.20 and $0.30 per share to the range between $0.28 and $0.33. The Street was looking for $0.30.

While in the past the company was not known for its operational excellence, after a period of transformation and restructuring, that is no longer the case, notes Wells Fargo analyst Gabe Hajde.

“We believe OI has re-earned credibility over 2022 (really, the last 24-36 months), displaying solid execution (despite several external headwinds) and achieved key initiatives including: (1) finalized legacy asbestos liab.; (2) exceeded targeted margin expansion initiatives in 2022; (3) completed $1.5B portfolio optimization (deleveraging ahead of plan); and (4) executing on capital expansion plans. In addition, we highlight several regions (Europe + Brazil) that are capacity-constrained, enabling a constructive pricing environment (expected to persist in 23/24). Lastly, OI is proactively managing energy disruption risk in Europe,” Hajde explained.

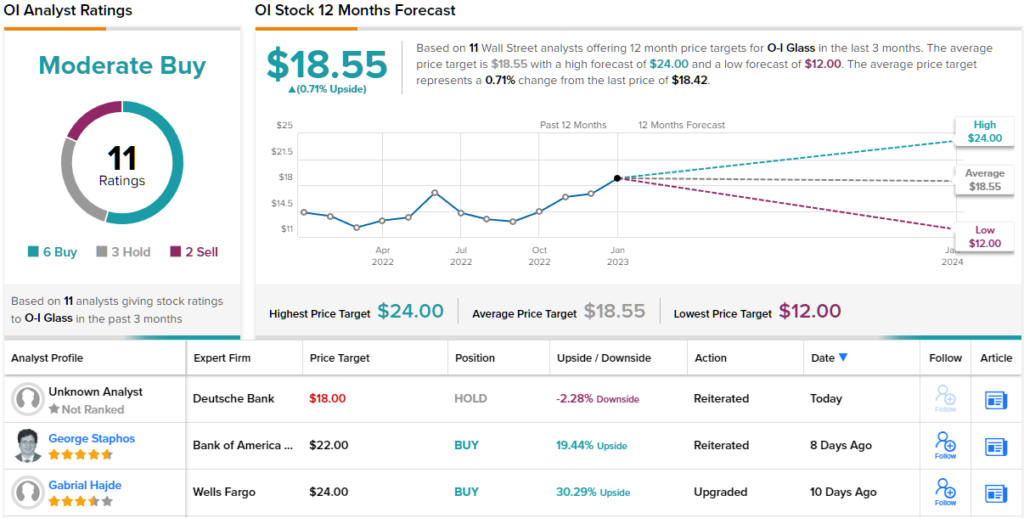

Expecting further consistency from the company, Hajde rates OI shares an Overweight (i.e. Buy), while his $24 price target makes room for additional gains of 26% in the year ahead. (To watch Hajde’s track record, click here)

Looking at the consensus breakdown, opinions on OI are more split. The bulls come in slightly ahead, with 6 Buys compared to 3 Holds and 2 Sells received over the previous three months. (See OI stock forecast)

Travere Therapeutics (TVTX)

The next Wells Fargo-backed stock we’ll look at offers an entirely different value proposition. Travere Therapeutics is a biopharma company whose goal is to discover, create, and commercialize life-changing treatments for people suffering from rare diseases.

Travere has already accomplished the feat all biotech companies are hoping to achieve – getting a drug to market. The company has several approved products in the U.S., including Thiola and Thiola EC, a tiopronin tablet used as a therapy for homozygous cystinuria and Chenodal, a synthetic oral form of chenodeoxycholic acid used to treat radiolucent gallbladder stones.

The company recently pre-announced 4Q22 product sales of $52 million and anticipates FY22 revenue will be roughly $212 million, slightly above consensus at $211.35 million.

Product sales aside, with small biotechs it’s all about catalysts and here Travere has a big one coming up. This year, the company expects the first regulatory approvals in the U.S. and Europe for sparsentan, the first and sole Dual Endothelin Angiotensin Receptor Antagonist (DEARA) being developed to treat rare kidney disorders. The FDA is currently assessing the New Drug Application (NDA) for sparsentan as a therapy for IgA nephropathy (IgAN) and a PDUFA date has been set for February 17. Should the regulatory body give the go ahead, Travere anticipates a Q1 launch for what will be the only non-immunosuppressive treatment indicated to treat IgAN.

Based on the drug’s potential, Wells Fargo’s Mohit Bansal lays out the bull case.

“We think [the company’s] lead drug sparsentan and its potential in kidney disease are underappreciated,” the analyst said. “The Street is only giving ~65-70% credit to its ~$1B sales potential, which we think is low… Investors are worried about liver monitoring, but we see likely chance of regulators agreeing to quarterly monitoring, which KOLs think is manageable… Sparsentan could see a strong go-to-market, as we see revenue potential for the first 12 months of launch exceeding that seen for Tarpeyo.”

“Furthermore,” Bansal added, “the confirmatory PROTECT eGFR data (expected 2H23) could support use of sparsentan over follow-on therapies in IgAN, improving visibility for a $1B+ product. We suggest these dynamics represent a straight forward path to improved sentiment as TVTX unlocks the value of sparsentan.”

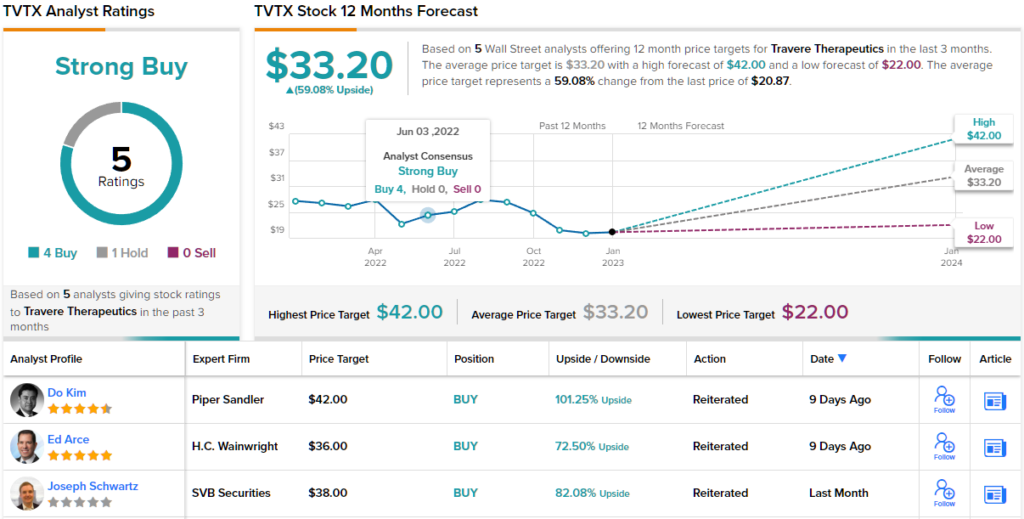

Accordingly, Bansal rates TVTX shares an Overweight (i.e. Buy) to go alongside a $28 price target. This figure conveys his confidence in TVTX’s ability to climb ~35% from current levels. (To watch Bansal’s track record, click here)

Bansal’s target is actually on the low side of expectations; the Street’s average stands at $33.20, making room for one-year returns of 59%. Reflecting that confident outlook, the stock scores a Strong Buy consensus rating based on 4 Buys vs. 1 Hold. (See TVTX stock forecast)

Subscribe today to the Smart Investor newsletter and never miss a Top Analyst Pick again.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.