After a much-touted SPAC merger, VinFast Auto (NASDAQ:VFS) stock is now available for trading. Don’t expect to hit the jackpot, though, as VinFast Auto isn’t in an ideal financial position. All in all, I am neutral on VFS stock and am waiting for the process of price discovery to play out before considering a long or short position.

Are electric vehicle (EV) SPAC stocks a thing of the past? Apparently not, as VinFast Auto debuted on Wall Street recently to much fanfare. VinFast Auto is based in Vietnam, and it’s another member of the growing list of EV manufacturer start-ups that were thrust into the spotlight after a quick share-price surge.

VinFast Auto doesn’t have any analyst ratings to rely on Wall Street’s opinion yet (though Wedbush analyst Daniel Ives and Canaccord analyst George Gianarikas did ask questions at a recent VinFast conference call). Still, I managed to unearth one analyst’s commentary on VinFast. As we’ll discover, that commentary isn’t highly positive, and VinFast’s revenue growth isn’t enough to declare the company a likely winner in the highly-competitive EV space.

Pay Attention to VinFast Auto’s Balance Sheet

If you only look at a company’s revenue growth and nothing else, you may end up losing a lot of money on a stock. A start-up business like VinFast Auto, for example, can expand quickly on a percentage-wise basis because it’s starting off on a very small scale. At the same time, the company might only be selling a relatively small number of vehicles and losing large amounts of money.

Let’s delve into VinFast Auto’s second-quarter 2023 results so you can see what I’m talking about. After converting from Vietnamese Dong (VND) to U.S. dollars, VinFast generated $334.1 million in revenue, up 131.2% year-over-year and 303.3% quarter-over-quarter. That certainly looks impressive, but again, VinFast is a tiny company that only sold 1,789 EVs in 2022’s second quarter.

Thus, the company’s exponential revenue growth might not be as impressive as it looks, percentage-wise. Plus, I must reiterate that sales growth doesn’t provide the full financial picture. After all, the bottom line is truly the bottom line.

As it turns out, VinFast Auto’s bottom line is improving but is still in questionable condition. The company’s Q2-2023 net loss of $526.7 million is 8.2% better than the net loss from the year-earlier quarter, but it’s still not something to be proud of. I usually give some leeway to start-up businesses, but VinFast’s quarterly $526.7 million loss is particularly troubling when the company’s balance sheet only showed cash and cash equivalents totaling $67.3 million as of June 30, 2023.

On the other hand, it’s been reported that VinFast received a $2.5 billion liquidity injection from its parent company, Vingroup. Will this be enough to keep VinFast afloat for a while? It’s too early to tell, but this looks like a company to watch rather than wager your hard-earned money on, if you ask me.

VinFast Auto Gets Attention from an Analyst…but It’s Not Positive

VinFast Auto might not have ratings from well-known analysts on Wall Street quite yet. However, Third Bridge analyst David Byrne did conduct his due diligence on VinFast and offered up some commentary.

It’s not positive commentary, though – and I don’t want to put words in his mouth, but Byrne seemed to lean decisively bearish on VinFast Auto’s future prospects. For instance, the Third Bridge analyst observed that VinFast “bungled the launch of the VF8 [SUV] in the US…[which] had to be recalled.”

When an analyst uses the word “bungled,” it’s fair to assume that he isn’t super bullish. Next, Byrne calculated that, based on available public data, VinFast Auto has over 1,500 units in inventory in the U.S., approximately 750 of which have been in inventory for over six months.”

In other words, VinFast Auto’s vehicle production-to-delivery ratio might not be ideal. Additionally, Byrne forecasted, “Cash commitments VinFast received from Vingroup of approximately $2 billion will last the company approximately 12 months at the current rate of burn.”

I don’t want to jump to any conclusions here, but it sounds like the $2.5 billion capital infusion from Vingroup might be a real lifesaver for VinFast. The company’s shareholders should hope that Vingroup uses that money wisely, though, and makes it last.

Conclusion: Should You Consider VFS Stock?

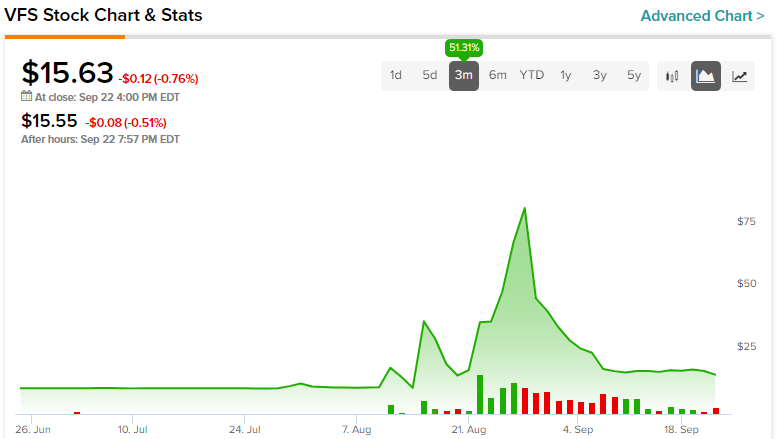

Check VFS’ stock chart above, and you’ll see a distressing pop-and-drop pattern. It’s a familiar arc that you may have already witnessed with other EV SPAC stocks that spiked and crashed.

I’ve even heard that VinFast’s SPAC backers are backing out. Overall, VinFast Auto’s revenue growth is its primary selling point, but even that is somewhat deceptive. Therefore, I’m choosing to stay away from VFS stock while the market figures out an appropriate price for it. Until then, I believe cautious investors would be better off not investing in VinFast Auto.