The temptation to ride along with Uber Technologies (NYSE:UBER) stock is strong after its powerful rally in 2023. However, value-focused stock traders might question whether it makes sense to invest in Uber Technologies now. I like the company’s prospects for the very long term, as it’s a market leader, but for right now, I am neutral on UBER stock.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Uber Technologies offers ridesharing and delivery services. Uber stock has been in and out of favor on Wall Street over the past few years, but it rallied sharply last year, likely due to the company achieving GAAP profitability and optimism about interest-rate cuts.

Sure, profitability is great, and interest-rate cuts would probably spur the U.S. economy, which could benefit Uber. Yet, as we’ll discuss in a moment, there’s a government-level change afoot that may have a negative impact on Uber. Plus, even though a prominent Wall Street expert likes Uber’s valuation, a glance at the data might cause prospective investors to think twice.

Gig-Work Policy Could Affect Uber’s Business

You might or might not be interested in public policy concerning gig work. However, if you’re a current or prospective UBER stock investor, you’ll definitely need to pay attention to the headlines.

According to a Reuters report, the U.S. Department of Labor just enacted a rule that will require companies to “treat some workers as employees rather than less expensive independent contractors.” That’s probably good news for some gig workers, but it’s not necessarily beneficial for Uber Technologies’ bottom line.

Furthermore, research indicates that when workers are classified as employees, they “can cost companies up to 30% more than independent contractors.” Uber is a textbook example of a business that heavily relies on gig workers, so it will be interesting to see if the Labor Department’s new rule will force Uber to reclassify a large number of its workers.

I wouldn’t call this a deal-breaker for UBER stock investors right now. Yet, it’s certainly an ongoing development that should be monitored, especially if it starts to affect Uber’s financials this year.

Uber and the “Rational Duopoly”

Here’s a concept to consider. Some industries in the U.S. are, for better or for worse, largely controlled by exactly two companies. When that’s the case, it probably makes sense to invest in the more dominant of the two companies, which, in the ridesharing market, would be Uber Technologies.

In second place is Uber’s chief U.S. rival, Lyft (NASDAQ:LYFT). Analysts are mostly lukewarm about LYFT stock, rating it a Hold on average. In contrast, as we’ll discuss later, analysts are generally bullish on UBER stock.

While Uber seems to be more favored by the analyst community than Lyft is, Uber also controls a much bigger portion of the U.S. ridesharing market. Wells Fargo (NYSE:WFC) analyst Ken Gawrelski estimated, “We’re roughly [at] 70/30 market share, a couple points here or there. Uber with the leadership share, Lyft at the number two spot.”

Gawrelski called this situation a “pretty rational duopoly,” perhaps suggesting that it’s a sustainable market-share balance. That’s a fair assessment, but as an investor, you might ask yourself which company really deserves your investable capital. I mean, it’s 70% Uber versus 30% Lyft. It sounds to me like the smart money should bet on UBER stock rather than LYFT stock.

Does UBER Stock Offer a “Compelling Valuation”?

So far, I’ve addressed a negative point and a positive point concerning Uber. As a value-focused investor, however, the tipping point for me is Uber’s valuation. Is it reasonable or too high?

To my surprise, Wedbush analyst Dan Ives recently declared that the “valuation’s compelling” for Uber, expecting the company to have a great year. Maybe Uber will continue to grow as a business enterprise in 2024. Yet, even if Uber’s revenue and income expand this year, it seems that the market has already priced in the company’s future growth.

Consider that Uber’s GAAP-measured trailing 12-month price-to-earnings (P/E) ratio is around 128x. This doesn’t strike me as “compelling,” especially when the sector median P/E ratio is slightly more than 22x.

Is UBER Stock a Buy, According to Analysts?

On TipRanks, UBER comes in as a Strong Buy based on 36 Buys and one Hold rating assigned by analysts in the past three months. The average Uber Technologies stock price target is $66.56, implying 4.7% upside potential.

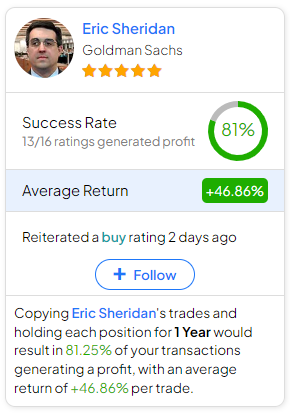

If you’re wondering which analyst you should follow if you want to buy and sell UBER stock, the most profitable analyst covering the stock (on a one-year timeframe) is Eric Sheridan of Goldman Sachs (NYSE:GS), with an average return of 46.86% per rating and an 81% success rate. Click on the image below to learn more.

Conclusion: Should You Consider UBER Stock?

I believe Uber will have to demonstrate exponential growth acceleration in 2024 to justify its current valuation. Plus, Uber may encounter difficulties this year in the wake of a new rule concerning gig workers.

Sure, Uber Technologies is the dominant leader in U.S. ridesharing. There’s no denying this, but value-conscious investors might take issue with Uber’s trailing multiple. Consequently, even though I appreciate the company’s “rational duopoly” with Lyft, I’m not currently considering a long position in UBER stock.