Uber’s (UBER) Q2 earnings report highlights why the recent dip in its share price presents a compelling buying opportunity. The company achieved record revenues and accelerated growth, significantly boosting profitability. With Uber efficiently scaling by growing its user base and improving unit economics, its earnings potential appears more robust than ever. While the stock is trading just 12% below its 52-week high, Uber’s impressive momentum and snowballing free cash flow make it an attractive investment at its current valuation. Given these factors, I am bullish on UBER stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Uber’s Revenue Growth Momentum Is Incredible

To further support my bullish view, Uber’s recent revenue growth has been nothing short of extraordinary. For context, I first grew interested in the stock in 2020, at a time when the pandemic had a notable impact on the company. Lockdowns and social distancing measures drastically reduced outdoor activities and travel, leading to declining demand for Uber’s ride-hailing services. As a result, the company’s revenues that year fell by 14.3% to $11.1 billion. However, Uber has since registered remarkable progress, with its revenues nearly quadrupling to over $40 billion in the past 12 months.

In addition, the company has maintained strong momentum, with its latest Q2 results indicating an acceleration in growth. Specifically, Uber’s revenues climbed 15.9% to a record $10.7 billion in its most recent quarterly report, marking an uptick both from the 14.8% growth reported in the previous quarter and the 14.3% growth seen in the same period last year.

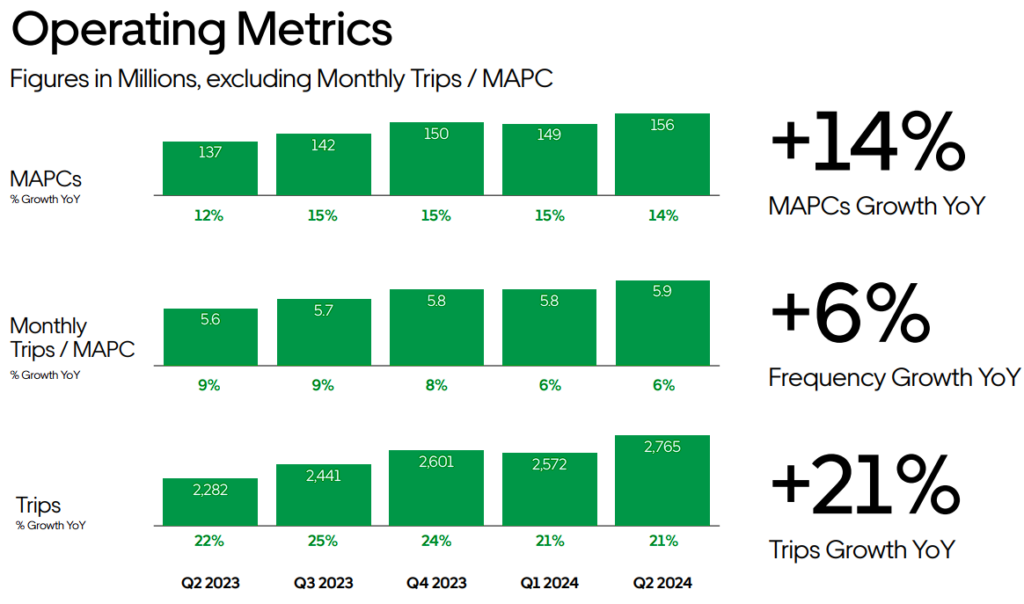

Furthermore, this rather impressive result was supported by a notable rise in gross bookings and trip frequency. Gross bookings surged by 21% on a constant currency basis, directly aligning with a 21% trip growth. Moreover, Uber also grew its audience by 14%, with the frequency of use increasing by 6%, backed by a global network of 7.4 million drivers and couriers. I think that the rising number of drivers and users joining and actively using Uber’s platform clearly demonstrates the company’s strong value proposition for all parties.

Interestingly, the delivery segment also contributed significantly to growth and showed strong performance, especially through Uber Eats. In particular, the number of first-time consumers in the U.S. hit its highest level in the past five quarters, also sustaining the narrative of accelerating growth.

Additionally, the grocery and retail sectors within the delivery segment showed exceptional growth, driven by consumers’ increasing preference for ordering their necessities anytime they want for added convenience. As a result, grocery ad spending on the platform more than tripled compared to last year, showcasing merchants’ heightened willingness to invest in ads to tap into this expanding demand.

Profitability Improvements Support the Current Valuation

Shifting the focus to profitability, the improvements in Uber’s delivery segment isn’t the only positive development adding to my bullish outlook. Investors have historically scrutinized Uber stock, particularly due to its lack of meaningful profitability and high levels of stock-based compensation (SBC), which clouded its investment case. However, with significant improvements in profitability and a decline in SBC as a percentage of revenue, the situation has changed. In fact, I believe Uber’s improved profitability now supports the stock’s current valuation.

In Q2, Uber’s profitability improved dramatically, with adjusted EBITDA rising by 71% to reach $1.6 billion. This figure represented 3.9% of Gross Bookings, a significant expansion from 2.7% last year. This increase was mainly powered by improving unit economics as the company scales. Further, advertising revenue, as mentioned earlier, also notably impacted margins. Uber’s ad revenue annual run rate has now exceeded $1 billion, and unlike deliveries/transportation, where Uber has to pay the drivers, ad revenue essentially flows to the bottom line.

Moreover, from a valuation perspective, focusing on Uber’s free cash flow is more insightful. Over the past 12 months, Uber’s free cash flow has surged to $4.75 billion, marking a 173% gain compared to the prior-year period. Of course, it’s essential to be cautious with free cash flow, as companies sometimes inflate it through SBC. However, Uber’s SBC has now decreased to just 4.7% of revenue, which seems quite reasonable.

Looking ahead, Wall Street forecasts Uber’s free cash flow to reach $5.74 billion this year and then grow by 35% to $7.75 billion next year. Therefore, Uber’s stock is currently trading at about 27 times this year’s free cash flow and 20 times next year’s. Given Uber’s rapid growth in free cash flow and overall vigorous momentum, I believe these P/FCF multiples appear quite attractive, signaling upside potential from the stock’s current levels.

Is UBER Stock a Buy, According to Analysts?

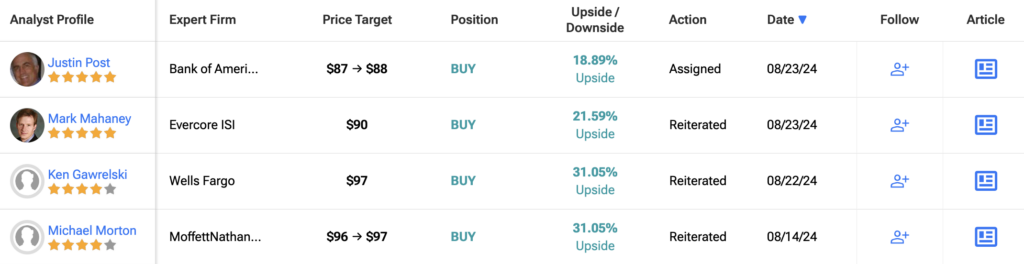

Looking at Wall Street’s view on the stock, Uber boasts a Strong Buy consensus rating based on 31 Buys and one Sell recommendation in the past three months. At $87.93, the average UBER stock price target suggests a 19.67% upside potential.

If you’re looking for the most accurate analyst to follow when buying and selling UBER stock, Eric Sheridan of Goldman Sachs (GS) is your top choice. Over the past year, his ratings have delivered an impressive average return of 44.29% and boast a remarkable 89% success rate.

Key Takeaway

Uber’s Q2 results paint a compelling picture for investors. The company’s record revenue, accelerating growth, improved profitability, and substantial free cash flow reflect its strong momentum and scaling capabilities. With the stock trading a bit below its 52-week high, I believe investors have the chance to buy Uber stock at rather attractive levels, especially given Wall Street’s optimistic free cash flow estimates.