Twilio (NASDAQ:TWLO) stock has been underdelivering for some time, and that’s reflected in the company’s share price. The stock is down just 1.8% over the past 12 months, but it’s down as much as 85% from its 2021 all-time high. However, it’s a leader in an emerging tech niche called communications platform as a service (CPaaS), and it’s evidently trying to make its operations more streamlined in an effort to improve returns and please shareholders.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

I’m bullish on Twilio despite its performance in recent years and hope to see it deliver soon.

What Is Twilio?

Twilio can be thought of as a toolbox for developers who want to add communication features to their applications. Imagine you’re building an app for ride-hailing. You’d want and need a way for riders and drivers to connect easily. With Twilio, app developers can easily integrate features like voice calls and text messages directly into their app. Twilio provides the building blocks, in a similar way to WordPress providing the solutions for building content and websites.

Twilio is something of a world leader in this CPaaS market. In addition to the simple communication features mentioned above, Twilio offers tools for more advanced video chatting and email integration, and it can even integrate communications through other platforms such as WhatsApp. Twilio is by no means the finished product, but it’s a company that provides developers with the tools to make communication features in other applications run smoothly.

Twilio’s Transition

Twilio’s affordable and easy-to-use solutions have helped it grow revenue at a significant rate, with revenue generation moving from $1.76 billion in 2020 to $4.15 billion in 2023. Earnings have been continually positive since Q4 2022. However, investors had been hoping for more — hence the 85% drop in the share price since its peak during the pandemic.

Now, under pressure from activist investors, Twilio is undergoing a transition. Management has committed to several rounds of job cuts, with the workforce shrinking at a rapid pace. In late 2022, Twilio had 7,800 employees, and according to Twilio’s Q4-2023 earnings release, Twilio had just 5,867 employees. This is a clear indicator of trying to streamline operations and reduce personnel expenses, which should have a positive impact on future earnings.

Twilio also seems to be prioritizing its core communication platform offerings — voice, text, video, and developer tools — in an effort to maximize earnings. This suggests a potential shift away from less central business areas. Notably, TWLO has made several divestments in recent years, including Zipwhip.

There’s also a change at the top. Co-founder and CEO Jeff Lawson recently stepped down from his position to be replaced by Khozema Shipchandler, who had served as President of Communications. Management changes can prove positive, and we all certainly hope that’s the case here, but they can increase risks. Nonetheless, Shipchandler’s previous experience with the company should make the transition easier.

Is Twilio’s Valuation Attractive?

Twilio hasn’t been an investor favorite since the latter stages of the pandemic. I’m sure, to some extent, investors have had their fingers burnt and don’t wish to get burnt twice, and I do wonder whether this has contributed to the company’s relatively attractive valuation metrics.

Twilio is currently trading at 22.5x forward earnings, but this falls to 18.8x in 2025 based on analysts’ projections. Moving forward to 2026, analysts suggest the company is trading at 15.7x earnings. Finally, the price-to-earnings ratio falls to 14.6x at the end of the forecasting period in 2027.

In fact, based on expected earnings growth, Twilio trades with a very attractive price-to-earnings-to-growth ratio of 0.75x. With 1.0x being the benchmark for fair value, we can deduce that Twilio’s growth expectations are significantly undervalued. Moreover, it has a strong financial position with $4 billion in cash and less than $1 billion in debt. Collectively, these metrics suggest that Twilio is undervalued.

There is, of course, a caveat. These price-to-earnings ratios and price-to-earnings-to-growth ratio are based on projected earnings for the medium term. Forecasts can be wrong. While Twilio doesn’t always underperform on a quarterly basis, over the long run, it has disappointed investors. Moving forward, I’m hoping for better.

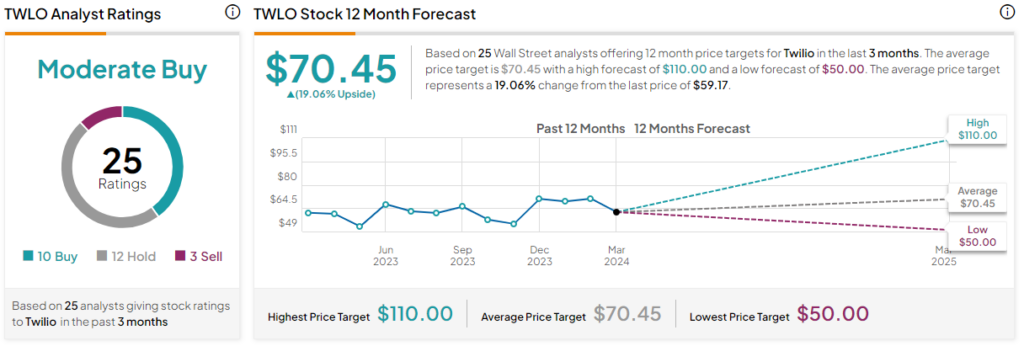

Is Twilio Stock a Buy, According to Analysts?

Twilio stock comes in as a Moderate Buy based on 10 Buys, 12 Holds, and three Sells assigned in the past three months. The average TWLO stock price target is $70.45, with a high forecast of $110.00 and a low forecast of $50.00. The average price target represents a 19.1% change from the last price of $59.31.

The Bottom Line on TWLO Stock

Twilio has struggled in recent years. It has disappointed investors, and it hasn’t delivered the earnings growth that many would have expected a few years ago. However, TWLO has implemented a transition with a new boss at the helm and several rounds of job cuts to make the company leaner. Earnings forecasts, and they are only forecasts, suggest that the stock is currently undervalued significantly. This may be the opportunity to pick up Twilio shares on the cheap.