Transocean (NYSE:RIG) shares closed more than 15% higher yesterday following better-than-expected Fiscal Q3-2022 results aided by robust demand and pricing for the company’s drilling market globally. Despite the stock’s rally recently, investors can consider buying the stock given its impressive backlog levels and huge demand for oil globally.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Based in Switzerland, Transocean is a leading global provider of offshore contract drilling services for oil and gas wells.

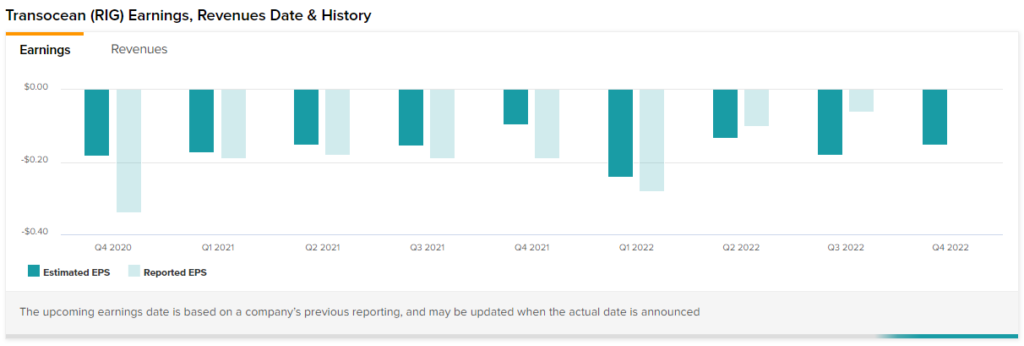

A Snapshot of Transocean’s Q3-2022 Results

The company reported an adjusted loss of $0.06 per share, easily beating the estimates of a $0.18 per share loss. Further, it was superior to the loss of $0.19 per share reported in the prior-year period. Meanwhile, total contract drilling revenues gained 10% year-over-year to $691 million.

The company recorded a contract backlog of $7.3 billion as of its October 2022 Fleet Status Report. Revenue efficiency came in at 95.0% during the quarter compared to 97.8% in the prior quarter. For reference, the company defines revenue efficiency as “actual operating revenues, excluding revenues for contract terminations and reimbursements, for the measurement period divided by the maximum revenue calculated for the measurement period, expressed as a percentage.”

Sharing his optimism, CEO Jeremy Thigpen commented, “We remain encouraged by the sustained strength in the offshore drilling market globally and expect demand for the increasingly scarce high-capability drilling rigs Transocean owns and operates to remain strong for the foreseeable future, resulting in higher utilization and dayrates.”

Is RIG Stock a Good Buy, According to Analysts?

Wall Street analysts are cautiously optimistic about Transocean stock and have a Moderate Buy consensus rating, which is based on three Buys and two Holds. Transocean’s average price forecast of $5.26 implies 29.4% upside potential.

Conclusion: Consider Purchasing RIG Stock

In terms of valuation, the company is trading at a premium. It is trading at an EV/EBITDA ratio of around 11x, a little ahead of its five-year historical average of 10.5x. Further, it is trading at a premium to its peer average.

The stock has gained almost 40% in the past month. Nonetheless, given the impressive backlog levels and huge demand for oil, amid the global demand and supply imbalance heightened by the Russia-Ukraine crisis, the stock is expected to do well in the coming quarters.