Persistent inflation and an escalating war in the Middle East are putting pressure on the stock market while giving investors an impetus to find safe havens. The S&P 500 has lost more than 3.5% so far this month, as nervous investors held back from stocks.

But not all stocks are losing traction in the face of these headwinds. Some stocks offer investors an array of supportive factors, strengths that can see them through a wide range of powerful difficulties. The Smart Score tool, from TipRanks, adds clarity to the stocks. The tool gathers voluminous data on every publicly traded company and uses it to compare the stocks to a set of eight factors that are known to predict future outperformance.

The result is exactly what investors need to find the right stocks in a tough environment: a simple score, on a scale of 1 to 10, that shows investors at a glance how a stock is likely to move in the near term. The higher the score, the better the stock’s odds of appreciating; a ‘Perfect 10’ indicates shares that deserve deeper consideration.

The ‘Perfect 10s’ frequently bring their own independent confirmation – these are also the stocks that Wall Street’s analysts frequently give high ratings. We’ve followed that line and have looked up the details on 2 top-scoring stocks that have plenty of opportunities – per the pro market watchers. Here’s a closer look.

GE Aerospace (GE)

The first stock we’ll look at is GE Aerospace, the inheritor of the GE ticker after the breakup of the venerable General Electric Corporation. The larger parent company, which had its hands in many pots and was one of America’s best-known corporate names and a long-lived multinational conglomerate, announced at the end of 2021 that it would split into three separate entities, to focus on healthcare, energy, and aerospace. GE Aerospace retains the ticker and the high-end aerospace and defense industries of its predecessor.

The split of General Electric into three companies was officially completed earlier this month. On April 2, GE Aerospace announced that it had completed the spinoff of the energy assets and businesses into GE Vernova and that GE Aerospace had begun operation as an independent publicly traded firm, focused on its role as a global leader in aerospace propulsion, systems, and services.

GE Aerospace’s primary business is the development and production of high-end engines, including jets and turboprops to meet the needs of both the commercial and military aviation sectors, as well as turbine engines for industrial and maritime purposes. GE Aerospace’s products include the engines for the F-35 fighter, as well as the GEnx engines used on Boeing’s 787 Dreamliner.

Looking at financial results, we find that GE last reported quarterly results for 4Q23. In that quarter, GE had a top line of $19.4 billion, up 15% year-over-year and $1.85 billion better than had been expected. At the bottom line, GE’s non-GAAP EPS of $1.03 was 13 cents per share better than had been expected. The company reported $21.7 billion in orders in the quarter, up 8% year-over-year and indicative of solid business demand. GE is predicting high-single-digit revenue growth in its 1Q24 report, which is due out on April 23. That report will cover the company’s last quarter of operations prior to its final split.

Shares in GE have posted sharp gains recently, and the stock is up more than 54% so far this year. These gains cap a 12-month period which has seen GE shares rise approximately 103.5%. The gains have come as investors worked to understand the value of GE Aerospace as a standalone entity and show an optimistic consensus on the stock.

Goldman Sachs analyst Noah Poponak sums up that positive sentiment, and gives his own upbeat outlook, in his post-split note on GE. Poponak writes, “We expect GE Aerospace will continue to benefit from strong commercial aerospace end-market demand. We expect both narrowbody and widebody production rates to ramp through the end of this decade, supported by near-record level backlogs at both Boeing and Airbus. Both OEMs are currently delivering well below supply. As they eventually ramp-up to meet demand, we believe they will build even larger installed bases of engines, which should drive decades of high margin aftermarket. The short-term hurdles to delivering that the aircraft OEMs have faced, means extensions of existing assets which drives more engine aftermarket before retirement.”

For the Goldman analyst, this adds up to a Buy rating with a $190 price target implying a 21%-plus upside for the year to come. (To watch Poponak’s track record, click here)

Poponak’s Wall Street peers clearly agree with the bullish take here. The stock has 16 recent analyst reviews, that include 14 Buys to 2 Holds for a Strong Buy consensus rating. The stock is selling for $156.76 and its $169.93 average target price suggests an 8.5% increase over the next 12 months. (See GE stock forecast)

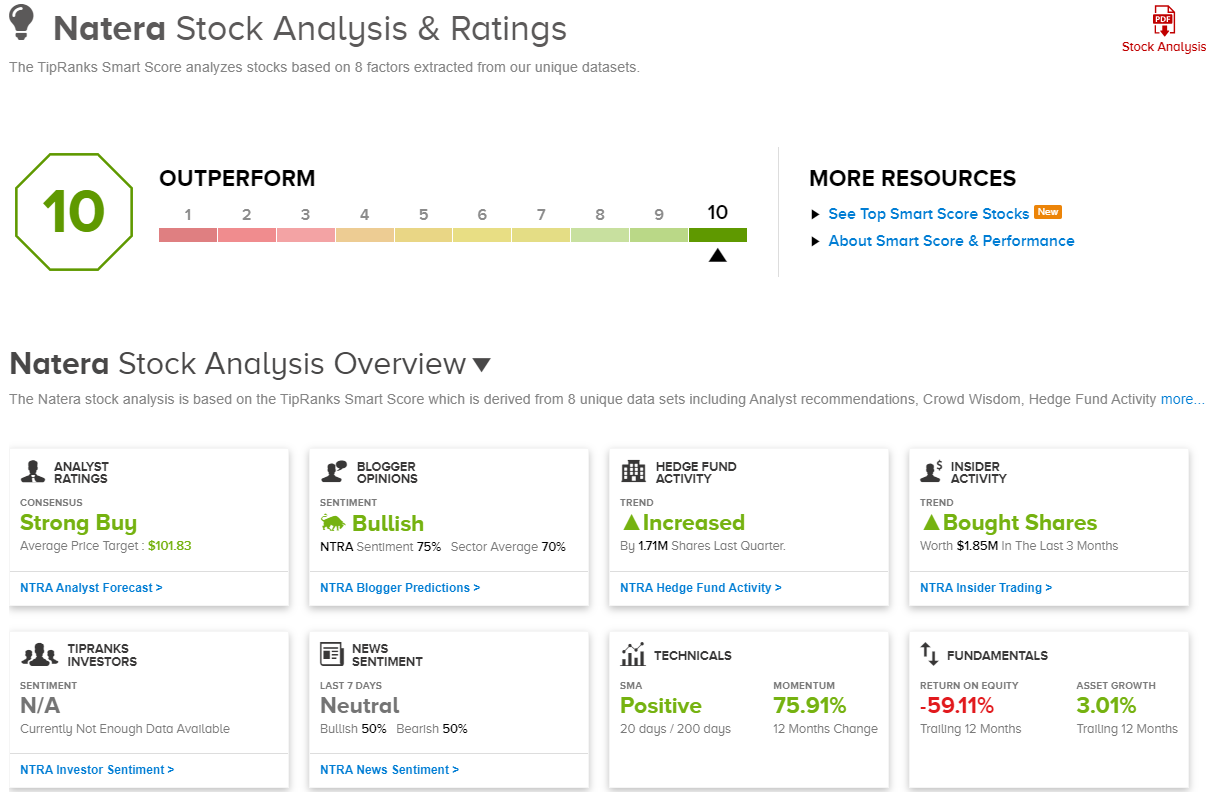

Natera (NTRA)

The second stock we’ll look at is Natera, a firm in the biotech sector. Natera’s work is the development and commercialization of cfDNA, or cell-free DNA, testing kits. These are DNA test kits designed to be minimally invasive, using the fragments of DNA that occur naturally as free-floating entities in the bloodstream. Natera has put together a line of diagnostic kits that can use these fragments in genetic testing.

This is a rich field, for a company that can pull it off successfully. There are many types of DNA that can be found in the bloodstream, from multiple sources including tumors, pregnancies, or the individual’s own cells. Natera’s cfDNA technology can capture and measure these fragments for a variety of genetic factors, and the company utilizes them for genetic testing purposes. Natera’s line-up of commercially available kits focuses on oncology, women’s health, and general organ health. They have proven particularly applicable to cancer diagnostics and treatment development and to organ transplantation and follow-up procedures.

Natera’s tests are subject to rigorous clinical testing, one notable trial being the ALTAIR study, a circulating tumor DNA (ctDNA) treatment escalation arm of the CIRCULATE-Japan adaptive trial platform, which is evaluating the company’s Signatera test for colorectal cancer. This is a serious cancer, but one that is amenable to treatment with early detection. Natera expects to release topline results from ALTAIR during the third quarter of this year.

On the financial side, Natera’s earnings and revenues have been trending upwards in recent quarters. The company’s last report, from 4Q23, showed a top line of $311 million, a figure that compared well to the company’s $300 million preannouncement, beat the analyst estimates by well over $23 million, and was up 43% year-over-year. The bottom line, a 65-cent per share loss, was negative – but was still 6 cents per share better than had been anticipated.

We should note here that NTRA shares have been outperforming the broader markets. The 12-month gain of 85%, and the year-to-date gain of 50%, have both strongly outpaced the S&P 500’s increases over the same periods.

This sets up a strong background for Craig-Hallum analyst William Bonello’s look at Natera. The analyst particularly notes Signatera as a reason for optimism here, and writes, “In nearly 25 years of following the diagnostic industry, we have rarely seen a company execute so effectively, on so many fronts, in such a short period of time… While our positive outlook is far more about the long-term opportunity than it is a trade-around-the-news call, we do acknowledge that there are potential catalysts that could drive the stock, perhaps the most important being: (1) Potentially positive updates to clinical guidelines for 22q and for carrier screening. (2) Top line data readout from the ALTAIR study. (3) Continued upside to numbers as guidance does not reflect increased volume from any guideline changes; additional positive coverage decisions for Signatera; benefit from biomarker legislation that mandates commercial coverage for Medicare covered tests.”

All told, Bonello rates NTRA as a Buy, and his $117 price target shows his confidence in a 29.5% share appreciation over the course of the next year. (To watch Bonello’s track record, click here)

The Strong Buy consensus rating on Natera’s stock is unanimous, based on 13 recent positive analyst reviews. The shares are priced at $90.32 and their $101.83 average price target suggests a one-year gain of 13%. (See NTRA stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.