The key to winning in the stock markets is simple: find the right stocks, the ones that are primed for gains, and load up on them. The only trick is understanding the stock signals, to recognize those upward-bound shares. There are as many signals as there are investors, it seems, so finding some objective measure may help sort through the market’s noise.

The noise is substantial. Thousands of investors deal in thousands of publicly traded shares, resulting in millions of transactions every day – and that wall of data makes a formidable barrier for the retail investor. Fortunately, the TipRanks Smart Score can turn those reams of information into a simple data point that indicates any stock’s likely path forward.

The Smart Score algorithm uses a combination of AI and natural language processing to sort through the data tossed up by the market’s activity, and compares each stock to a set of factors that have been shown to predict future performance. The end result is a single-digit score for each stock, on a scale of 1 to 10, with the ‘Perfect 10s’ indicating shares that are likely to bring gains.

The thing to note here is that the Smart Score predicts future performance and sometimes stocks that have been through a bad patch can still claim that ‘Perfect 10’ rating. Stock prices fall for a myriad of reasons, but can be primed for a recovery, and with this in mind, we’ve decided to give a couple of low-lying ‘Perfect 10’ stocks the closer look that they deserve. According to the TipRanks data, these are equities that have seen declines recently but still retain their high Smart Score rating. Here are the details.

Crescent Energy Company (CRGY)

We’ll start in the energy sector, specifically in the oil and gas production segment. Crescent Energy bills itself as a growth-oriented, differentiated US energy company, with a portfolio of ‘low-decline, cash-flow oriented’ crude oil and natural gas assets. The company’s activities are located mainly in the Eagle Ford formation of Texas and the Uinta Basin of Utah, where Crescent is working both conventional and unconventional mid-cycle assets that feature long reserve life and deep inventory in low-risk, high-return developments.

This portfolio of assets has given Crescent some sound production numbers recently. In the company’s last reported results, from 3Q23, total production came to a company record; at 157 Mboe/d, the Q3 production was up 13% quarter-over-quarter. Of that production, oil alone made up 46%, while all liquids made up 62% of the total volume.

Crescent also generated sound cash flows during the quarter. The company’s operating cash flow came to $189 million, while the levered free cash flow was another company record, of $160 million.

At the top and bottom lines, Crescent realized quarterly revenues of $642.4 million and an earnings loss of 67 cents per share. The revenue figure was down 25% year-over-year, although it came in $42.5 million ahead of the forecast. The 67-cent loss was the GAAP figure; the company’s non-GAAP earnings came to a positive total of $59 million for the quarter.

Dividend-minded investors should find something to like here. Crescent declared and paid out its regular quarterly dividend on December 4, at a rate of 12 cents per share. The annualized rate of 48 cents gives a forward yield of 4.2%, more than enough to beat the current rate of inflation and ensure a real rate of return.

For Truist analyst Neal Dingmann, the outlook here is straightforward and positive. He writes of the upcoming Q4 readout, “We believe 4Q23 like the prior quarter combined solid organic operations with relatively recent accretive added assets will result in a steady ramp in production along with accompanying solid FCF. We forecast the continued two-rig program combined with industry leading baseline production and an occasional accretive deal to drive shareholder returns and value.”

The stock, however, has not gotten off to a good start this year (down by 13% year-to-date), a performance that is undeserved, says the 5-star analyst: “We believe the YTD stock price start is unjustified as the operations in our view remain on target to generate materially sequentially 2024 FCF that will be used to boost shareholder returns beyond the current ~5% dividend yield and/or continue with attractive deals and/or lower leverage.”

These comments back up Dingmann’s Buy rating, and his price target of $23 implies the shares will double in value over the coming year. (To watch Dingmann’s track record, click here.)

Overall, the Strong Buy consensus rating on CRGY is based on 5 recent reviews, including 4 Buys to just 1 Hold. The shares are trading for $11.50 right now, and their $17.60 average price target suggests a 12-month upside potential of 53%. (See Crescent’s stock forecast.)

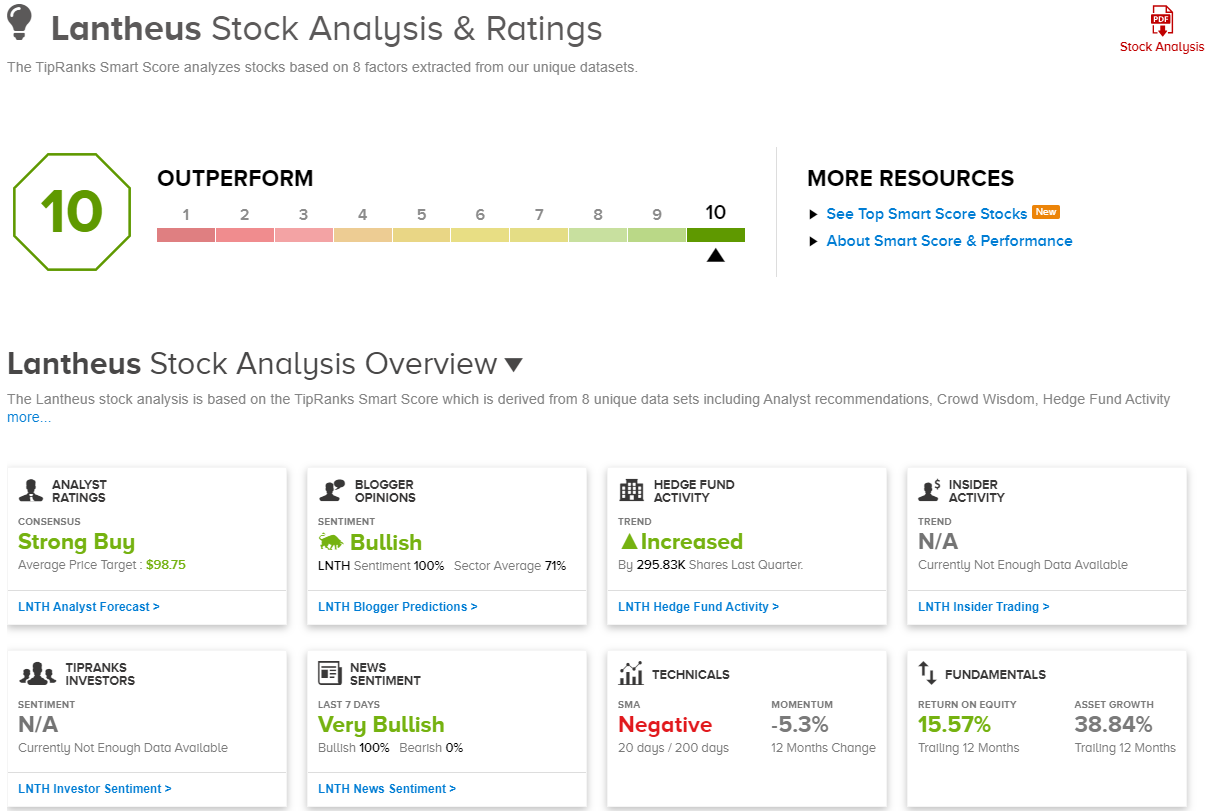

Lantheus (LNTH)

The second stock we’ll look at is a commercial and clinical stage biopharma firm. Lantheus is focused on radiopharmaceuticals, that is, radiation-based products used in the imaging and diagnostic fields, as well as in finding and fighting various cancer or cardiac conditions. The company’s research pipeline features nearly a dozen tracks, targeting multiple cancers, with a particular emphasis on new treatments for prostate cancer.

Lantheus has a diverse portfolio of medical products available, that have been generating profits for the company for the last several years. The company reported global revenue of $319.9 million in its last quarterly report, from 3Q23. This was up more than 33% y/y and came in almost $5.5 million over the estimates.

The company’s leading product, Pylarify, generated more than $215 million of that revenue, or 67% of the total. Pylarify is a radiopharmaceutical treatment for prostate cancer, using radiation as the therapeutic agent in reducing tumors. Lantheus’ second leading product, by revenue, was Definity, an injectable enhancer used in the ultrasound imaging process, particularly in cardiovascular echocardiography. Revenues from Definity came to $67.3 million in Q3.

Since that last Q3 release, Lantheus has seen a serious decline in share value. The stock fell sharply on December 18, losing 27% in just one day, with the catalyst being a disappointing data release from the pipeline. The shares have continued sliding since (down by 30% in total compared to the pre-data readout). Lantheus has been working with POINT Biopharma on a new drug, PNT2002, as a new treatment for metastatic castration-resistant prostate cancer (mCRPC), and on December 18 released topline data from the Phase 3 SPLASH clinical trial. While the drug candidate met its primary endpoint, industry analysts had expected a stronger therapeutic benefit than was shown in the trial.

Nevertheless, when we turn to the analysts, we find that Truist’s Richard Newitter remains upbeat on the company’s long-term value for investors. He says of Lantheus, “Our stock view is unchanged: Ultimately, we still think it will be a grind higher for shares from here, pending further clarity around PNT2002 next steps and more visibility around TPT expiration in 2025+. But at ~$53, shares are trading at <9x ‘24E EPS which we do not believe reflects appropriate credit for pylarify + the ‘core’ business, think are worth at least $76+/shr on their own.”

Newitter, a 5-star analyst, goes on to reiterate his Buy rating on the stock, and his $80 price target points toward a one-year upside potential of 51%. (To watch Newitter’s track record, click here.)

Almost all of Newitter’s colleagues agree here; the Strong Buy consensus rating on this stock is based on 10 recent analyst reviews that feature a lopsided 9 to 1 split between Buy and Hold. The shares are priced at $52.88, and their $98.75 average price target suggests a solid gain of 87% for the coming 12 months. (See Lantheus’ stock forecast.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.