The first half of 2022 was dominated by high inflation and the Federal Reserve’s shift to an monetary tightening policy in response. The second half will find those same factors still pushing on stocks – but they’ll be joined by earnings pressure, in the view of Morgan Stanley equity strategist Mike Wilson.

“Indicators suggest margin pressure and earnings growth risk ahead. This view is confirmed by our leading earnings model, which projects a steep fall in EPS growth over the next several months. A key input to this model is the ISM manufacturing PMI, and leading regional Fed manufacturing surveys point to continued downside in the ISM PMI,” Wilson explained.

Wilson’s comments take added meaning in the wake of last week’s Jackson Hole symposium, during which Federal Reserve Chairman Jerome Powell said flat-out that inflation is going to get worse before it gets better – and that the Fed’s policy of monetary tightening will cause further pain.

The upshot is, it’s time to play defense on the stock portfolio. The analysts at Morgan Stanley know this, and they’ve been tagging the classic defensive stocks: dividend payers, with yields high enough to offer some protection against inflation. We’ve pulled the details on two of these Morgan Stanley picks from the TipRanks database; here they are, presented along with the analyst commentary.

Simon Property Group (SPG)

We’ll start by checking out a real estate investment trust, or REIT; these companies have long been leaders among high-yield dividend payers. Simon Property Group is a commercial REIT, focused on retail properties. Simon’s portfolio is heavily weighted toward shopping malls, with 95 such properties. The company also owns 29 premium outlets, and 33 international properties. In addition, Simon owns an 80% stake in the Taubman Group, which is itself a large-scale property owner on the international scene.

Simon’s quarterly revenues showed steady gains ‘after COVID’ and into 1H21. Since 3Q21, the company’s quarterly revenues have averaged $1.3 billion. The current top line, from 2Q22, came in at $1.28 billion. Net income was reported at $496.7 million for the quarter, with a diluted EPS of $1.51 per share. Income was down from the year-ago quarter, when it was reported at $1.88 per diluted share.

A key metric in evaluating a REIT is ‘funds from operations,’ or FFO, as this is usually used to fund the dividend. Simon’s FFO in 2Q22 was listed as $1.09 billion, or $2.91 per diluted share. While down from the year-ago quarter’s $3.24 per diluted share, it was still more than enough to cover the dividend, which was declared on August 1 for $1.75 per common share. The dividend is scheduled for payment this coming September 30. At the current rate, the dividend annualizes to $7 per share, and yields a high 6.8%.

Morgan Stanley analyst Ronald Kamden believes that Simon is well-positioned for gains in tough environment, writing: “We have higher conviction in our thesis that cash flows will be more resilient than anticipated following the pull forward of store closures during COVID. We expect SPG to prove to be along term winner from the shake-up in retail given its strong balance sheet (mid5s debt to EBITDA) and ability to self-fund (re)development costs with FCF generation.”

“Three factors differentiate SPGs portfolio: 1) malls contributed only ~48% of total NOI and the rest of the portfolio is diversified across premium outlets and other retail types, 2) after a 30-35% rationalization in the mall landscape, we estimate only a ~5% hit to total NOI and 3) greater negotiating leverage with tenants post the acquisition of TCO’s higher quality malls which increase their ownership of the most dominant malls in the US from ~30 to ~50,” the analyst added.

To this end, Kamden gives the stock an Overweight (i.e. Buy) rating, and his $131 price target suggests ~27% upside over the next year. (To watch Kamden’s track record, click here)

Overall, this stock has earned a Moderate Buy rating from the Street, based on 13 recent analyst reviews that break down to 5 Buys and 8 Holds. The shares are selling for $103.66 and their $121.85 average price target indicates room for ~18% upside this year. (See SPG stock forecast on TipRanks)

Blackstone Group (BX)

Now let’s shift over and look at Blackstone Group. This an easily recognized name in the financial world; Blackstone is one of the world’s largest alternative investment companies, with its hands in multiple investment areas, including $80 billion in hedge funds, $265 billion in credit and insurance, $276 billion in private equity, and $320 billion real estate. Blackstone operates globally, and holds over $941 billion in total assets under management.

This portfolio generated $7.5 billion in net accrued performance revenues for Blackstone in 2Q22, or $6.18 per share, up 11% from the year-ago quarter. The company also reported a 45% year-over-year gain in free related earnings, to $1 billion, and an impressive 86% y/y gain in distributable earnings, which reached $2 billion in the quarter.

That last is important for return-minded investors, as it funds the dividend. Blackstone paid out its last common share dividend on August 8, at $1.27 per share – fully covered by the $1.49 per share in distributable earnings – and repurchased 1.9 million shares during the second quarter. In all, between Q2 dividends and share repurchases, Blackstone returned some $1.9 billion to its shareholders in the quarter. The $1.27 dividend annualizes to $5.08 per common share, and yields a respectable 5.3%.

Analyst Michael Cyprys, in his coverage for Morgan Stanley, writes of Blackstone: “Prefer diversified, high quality BX as a core holding in Alts for investors looking for exposure to the group… We see a best-in-class franchise, brand, unrivalled product capabilities/breadth and retail TAM expander that’s set to transform the earnings profile to 75% FRE by 2026e from current ~50%. We see BX as a long-term winner with upcoming fundraising super-cycle catalyst, while fee-related performance fees can hold up better than market fears.”

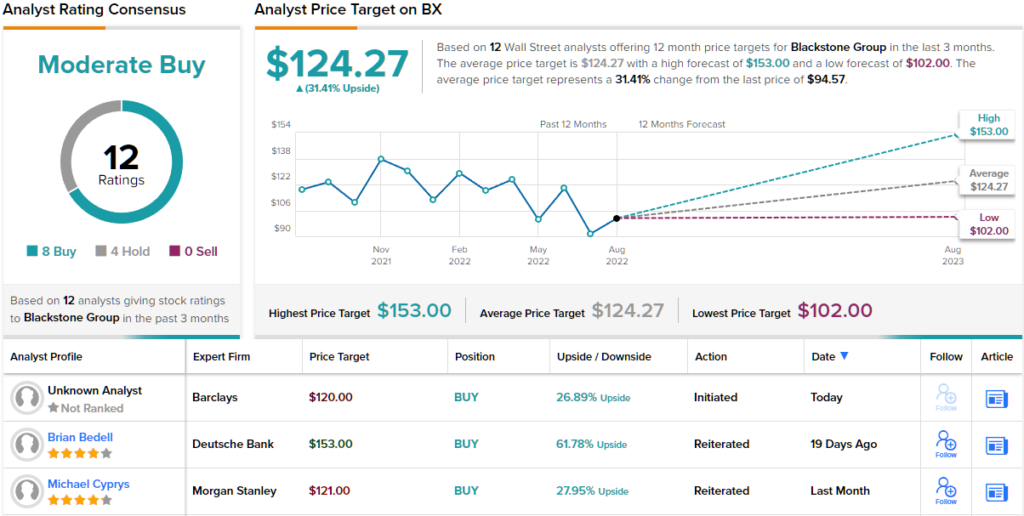

Putting his stance into quantifiable numbers, Cyprys gives the stock a price target of $125, suggesting a 31% one-year upside potential, along with an Overweight (i.e. Buy) rating. (To watch Cyprys’ track record, click here)

All in all, with 8 recent Buy reviews on record, and 4 Holds, Blackstone gets a Moderate Buy from the analyst consensus. The stock is selling for $94.57, and its average price target of $124.27 implies ~31% upside for the year ahead. (See BX stock forecast on TipRanks)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.