The semiconductor chip industry presents investors with a difficult landscape to navigate. A combination of strong headwinds and economic-structural supports are buffeting the industry in contradictory directions, and for at least the near-term the best investment choices aren’t necessarily clear.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Take the headwinds first. Some of the strongest revolve around China, the world’s second-largest economy and a major consumer of semiconductor chips. The country was under strict anti-COVID lockdown policies until just recently, which crimped both supply and distribution chains, while also tamping down industrial and technical production. While the logistic issues are easing as the Chinese government backs off from ‘zero-COVID,’ the Biden administration has taken a hard line on tech trade with China, placing restrictions on Chinese purchases of chips and technology from US companies.

The industry could have navigated those issues – but it’s also facing a general demand shortage right now. As pandemic restrictions ease around the world, demand for remote access systems has fallen – and that was a big driver of chip consumption in 2020 and 2021.

On the positive side, the world’s economy is still digitizing, and semiconductor chips are still an essential product. New and established technologies – such as electric and/or autonomous vehicles, 5G broadband, and the regular improvements to smartphone, tablet, and computer devices – still consume chips at a voracious rate. And that means that investors can find opportunities to buy in.

So let’s look at some chip stocks. Using the TipRanks platform, we’ve pulled up the latest scoop on three that are showing a trio of attributes that should attract investor interest: a Buy-rating, double-digit upside potential for the coming year, and recent love from some 5-star analysts. This all adds up to some hot buys in a hot industry. Here are the details.

Monolithic Power Systems, Inc. (MPWR)

Based out of Kirkland, Washington, Monolithic Power Systems bills itself as the ‘fastest growing power semiconductor company.’ Its product lines include power modules, power converters, battery management, motor drivers, sensors, and inductors for electronic systems found in a range of applications, including the automotive, IoT, optoelectronics, biomedical, cloud computing, and telecom sectors. Monolithic’s products are found as key components in the offerings of numerous OEMs throughout the economy, and the company’s diversified approach has led to steady gains in both the top and bottom lines over the last several years.

In the most recent quarter reported, Q3 of 2022, Monolithic showed an impressive 53% year-over-year increase in revenue, from $323.5 million to $495.4 million. Sequentially, this was a 7.5% gain. At the bottom line, the GAAP net income came in at $124.3 million, or $2.57 per share. The GAAP EPS was up 78% y/y. By non-GAAP measures, the EPS of $3.53 showed a 71% y/y increase.

This company hasn’t just given investors a return through revenues and profits; Monolithic also keeps up a reliable dividend payment. The payment is currently set at 75 cents per common share, and the company has been increasing it steadily for the past 9 years. At its current rate, the dividend annualizes to $3 per share, although the yield is a modest 0.75%.

In his coverage of this stock for Credit Suisse, analyst Chris Caso notes both structural and historical reasons for optimism on the shares. He writes, “We feel MPWR’s sustainable advantage is driven by two factors. One is their proprietary BCD process, which has historically demonstrated that MPWR can provide more efficient power management products in smaller footprints. The other advantage is MPWR’s smaller size, making them a bit more nimble – and design wins in sizeable areas such as server power and EV have the ability to significantly move the needle at MPWR’s size.”

“Our estimates are below consensus through 1H23, as we are simply taking a more conservative view toward market conditions. This doesn’t frighten us. The stock rose in 1H19 even as consensus estimates came down, as the buy side was (again) ahead of the sell-side, and investors took the opportunity to buy one of the highest quality names in the space when it was on sale,” the 5-star analyst went on to add.

Taking this view forward, Caso rates MRWR as Outperform (a Buy), with a $475 price target to suggest a one-year share price gain of 24%. (To watch Caso’s track record, click here.)

This chip company has picked up 11 recent analyst reviews and they are all positive – backing up a Strong Buy consensus rating. The stock is selling for $383.29 and its average price target of $454.27 implies an 18% potential upside on the one-year horizon. (See Monolithic Power’s stock forecast at TipRanks.)

Analog Devices, Inc. (ADI)

Next up is Analog Devices, a company known for its product lines in signal processing and data conversion chips. Analog offers a wide product portfolio, with chips and devices applicable to amplifiers, RF and microwave systems, processors and microcontrollers, power management, audio products, industrial ethernet solutions, interface and isolation, power monitors, and clock and timing systems. The company’s customer base, more than 100,000 strong, is primarily B2B. Analog has leveraged its diversified products and large customer base to generate some $12 billion in annual revenues.

A look at Analog’s last quarterly report tells the story. In its release, for Q4 of fiscal year 2022, the company had a top line of $3.25 billion, up 39% y/y, and well above the forecast of $3.16 billion. At the bottom line, Analog showed an adjusted EPS of $2.73, for a 58% y/y gain – and again, a significant beat of the forecast, by almost 6%.

The company’s gains were driven by strong performance in all four main segments of the business – the automotive, communications, consumer, and industrial. Automotive led the way, with 49% y/y growth.

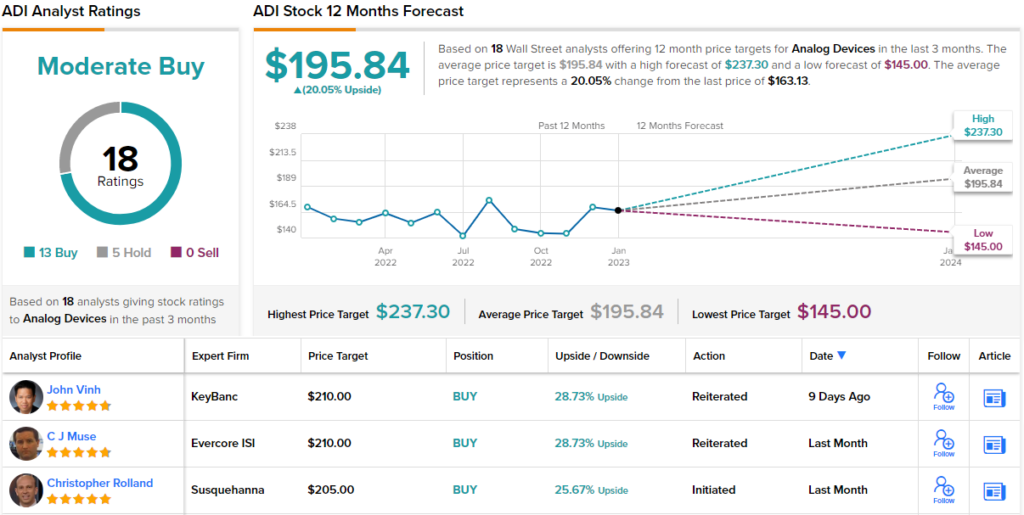

This stock caught the eye of Susquehanna analyst Christopher Rolland, who pointed out numerous supportive factors for an upbeat rating. “ADI, particularly with their acquisitions of Linear and Maxim, has become one of the great analog catalog companies in the industry,” the 5-star analyst said. “Additionally, they have become the “anti-Texas Instruments,” leaning into distribution, “value creation” incentives, dual-sourced third-party manufacturing, and analog innovation (e.g., wireless BMS). Opportunities around electric vehicles (BMS), communications (5G RF), and specialty analog (medical, instrumentation, aerospace) should help maintain industry-leading margins and growth.”

These comments highlight a Positive (Buy) rating on the stock, while Rolland’s $205 price target implies a one-year upside potential of 26%. (To watch Rolland’s track record, click here.)

Analog Devices gets a Moderate Buy consensus rating from the Street, based on 18 recent analyst reviews that include 13 to Buy and 5 to Hold. The shares have an average price target of $195.84, suggesting a 20% upside from the current trading price of $166. (See Analog Devices’ stock forecast at TipRanks.)

GlobalFoundries, Inc. (GFS)

We’ll wrap up our list of chip stocks with GlobalFoundries, a California-based firm that offers both chip manufacturing and design services to contract customers in a series of industries, including IoT, automotive, computing, and wired networking. As its name suggests, GlobalFoundries operates around the world, and its operations include chip foundries, design centers, and R&D facilities.

2022 was GlobalFoundries’ first full calendar year as a publicly traded company, and its last financial release, for 3Q22, was its fifth since entering the public markets. GFS has showed only gains in its public releases; the top line in 3Q22 was $2.07 billion, up 4% sequentially, 12% y/y, and 21% since its first public quarterly report.

At the bottom line, net income came in at a record $336 million, while adj. EPS came in at 67 cents, compared to 7 cents in 3Q21 and 58 cents in 2Q22. In short, there’s a global need for silicon semiconductor chips, and GlobalFoundries is leveraging that need to generate solid gains in revenues and profits.

Baird’s Tristan Gerra has noticed that, too, and he takes a bullish view of Global Foundries. The 5-star analyst outlines several reasons why this company occupies a sound position for future gains: “GF is skillfully navigating the current waters, notably with a near-exit from PCs (from 25% exiting 2020 to 2% currently) and moving into fast-growth markets, combined with pricing discipline. GF’s capacity is oversubscribed for 2022 and 2023. LTAs already account for 75% and 51% of 2024 and 2025 capacity, respectively. Additional LTAs are expected to come online, embedding modest price increases for 2023 and highlighting GF’s ability to offer differentiated solutions. GF’s exposure to China is small at less than 10%, with no impact from the U.S. export restrictions.”

Taking this stance to its logical end, Gerra puts an Outperform (Buy) rating on the shares, and his $100 price target implies an upside of 80% for the next 12 months. (To watch Gerra’s track record, click here.)

The Strong Buy consensus rating on GFS shares is based on 10 recent analyst reviews, with a 9 to 1 breakdown favoring Buy over Hold. The stock is selling for $55.55 and the $75.09 average price target indicates a potential gain of 35% over the coming year. (See GlobalFoundries’ stock forecast at TipRanks.)

Subscribe today to the Smart Investor newsletter and never miss a Top Analyst Pick again.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.