Dividend investing has always been popular, and for good reason. Dividend stocks offer a wide range of advantages for return-minded investors, but two of the most significant are a reliable income stream and an inflation-beating yield. Taken together, these advantages can form the base of a truly sound portfolio.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The majority of dividend stocks pay out on a quarterly basis, but turning towards those with a monthly payment schedule allows investors to better plan their income streams to meet their needs. When it comes to yields, they are still calculated based on the annualized rate of the dividend, so even a small monthly payment, multiplied by 12, can result in a high annual yield.

But not all dividend stocks are created equal, and some offer better opportunities than others. This is where Wall Street’s analysts come into play.

Diving into the TipRanks database, we have homed in on two monthly-payment dividend stocks that not only boast a market-beating dividend yield of at least 13% but also qualify as ‘Strong Buys’ according to the analyst consensus. Let’s take a closer look.

Dynex Capital (DX)

We’ll start with Dynex Capital, a real estate investment trust company that focuses on mortgage loans and securities. Dynex allocates its resources to both agency and non-agency mortgage-backed security (MBS) instruments and also has exposure to the commercial MBS market. The company’s portfolio also contains a sizable portion of mortgage loans, including both securitized single-family residential and commercial mortgages dating back to the ’90s.

Dynex adheres to several simple strategic points in building its portfolio. The company is committed to capital preservation and disciplined allocation of that capital, using risk management techniques to maintain long-term returns. Furthermore, the company has always been committed to maintaining the dividend as a healthy component of those returns. Finally, and of key importance to dividend investors, Dynex keeps its sights set on maintaining stable and acceptable returns over the long term.

In the last quarter reported, 2Q23, Dynex’s bottom line came in with a net income per diluted share of 96 cents. This EPS exceeded expectations by $1.25 and compared favorably to the 81-cent EPS loss reported for 1Q23. Additionally, Dynex reported $561.5 million in ‘cash and unencumbered assets’ available at the end of Q2, with $300.1 million in cash, representing a 7.5% increase from Q1.

The company’s combination of a positive net income and solid cash assets on hand fully covered the monthly dividend payment, which was last declared in August at 13 cents per common share and paid on September 1. The dividend annualizes to $1.56 per share, providing an attractive yield of 13%.

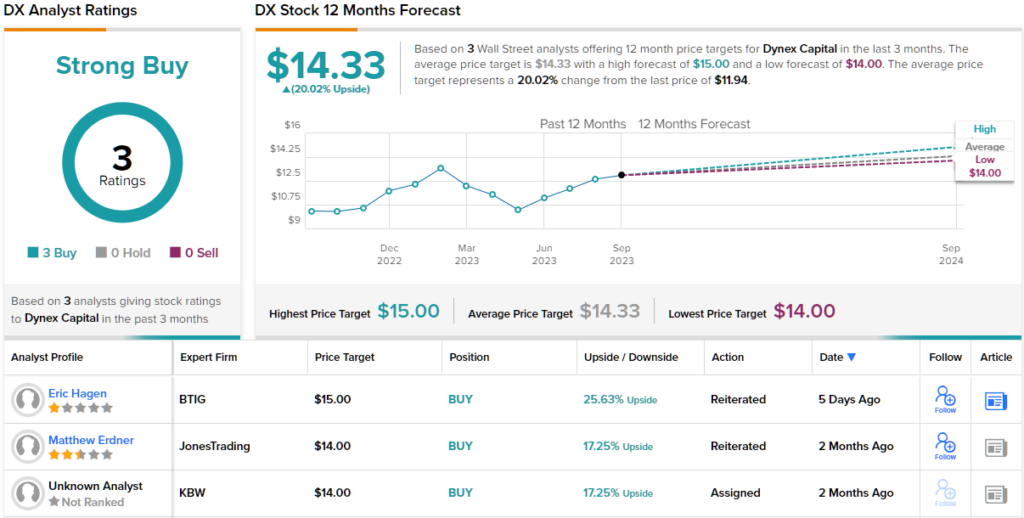

Covering the stock for BTIG, analyst Eric Hagen points out the company’s solid return profile – and the fact that the dividends are fully covered by income and assets.

“Our expectation [is] for DX’s dividend to remain stable at these spread levels, or even a little wider, followed by the opportunity to capture some capital appreciation (book value upside) when mortgages eventually tighten versus interest rates. Having strong conviction for spreads to tighten is admittedly a moving target (tethered mostly to realizing lower interest rate volatility), although we expect stock valuation could improve quickly when that visibility comes into better focus… We think the real value being captured along the way is managing and preserving a very healthy and transparent liquidity position, which we expect to remain in excess of $400 million, or more than half its capital base,” Hagen opined.

Hagen uses these comments to support his Buy rating on DX stock, and his $15 price target points toward an upside potential of ~26% in the coming months. Adding in the dividend, and the total return on this stock is a solid 39% for the year ahead. (To watch Hagen’s track record, click here)

Overall, all three of the recent analyst reviews on Dynex are positive, making the Strong Buy consensus rating unanimous. The shares are selling for $11.94 and their $14.33 average price target implies a 20% one-year upside. (See DX stock forecast)

Ellington Financial (EFC)

The next high-yield dividend stock we’ll look at is Ellington Financial, another mortgage REIT. This firm works in the acquisition and management of financial assets, with particular attention to such mortgage-related assets as MBSs and equity investments in commercial and residential mortgage loans. The company reported having $9.4 billion in total assets under management as of June 30 of this year.

The AUM is only part of Ellington’s story. The firm reported a solid balance sheet in its release of the 2Q23 financial results, the last such results reported. Total assets on the balance sheets came to $14.3 billion, $194.6 million in cash and another $343.3 million in other unencumbered assets. At the end of the quarter, the company had a book value per common share of $14.70; it’s important to note that this book value is down approximately 35 cents per common share from the December 2022 and March 2023 readings.

In a metric of special importance to dividend investors, Ellington reported adjusted distributable earnings of 38 cents per common share for Q2. While profitable, this was 5 cents per share lower than had been expected. Despite the miss on earnings, Ellington has maintained its monthly dividend payment at 15 cents per common share, or 45 cents per share quarterly. The annualized dividend payment, of $1.80 per common share, yields 14.4% at current share prices.

Analyst Crispin Love, covering Ellington for Piper Sandler, points out that the firm is taking steps to diversify its portfolio and expand into new territory. He writes of the company’s interests going forward, “A key catalyst for Ellington over the next several quarters could be loan acquisition opportunities to buy both performing and non-performing loans. We believe Ellington could be a bidder for the Signature CRE loans as the company has the expertise and the purchases would be consistent with the company’s history (especially following the Great Financial Crisis). On recent earnings calls, management commented that it would be interested in participating in the FDIC loan sales assuming that the transactions would be accretive to EFC. In addition to potentially participating in FDIC loan sales, EFC has been vocal about a desire to buy CRE loans from banks.”

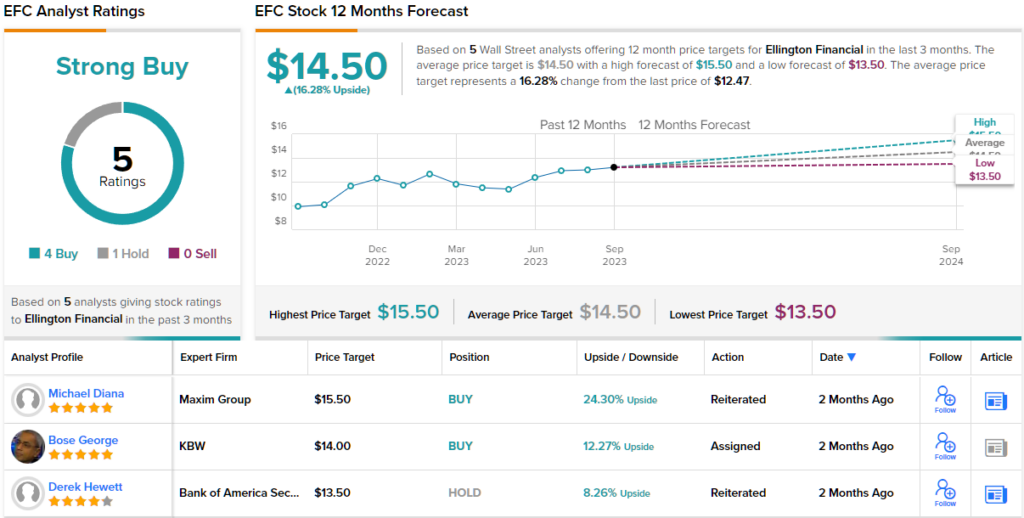

It’s clear from his Overweight (i.e. Buy) rating, and his $15 price target, that Love does see Ellington’s potential acquisitions as accretive. His price target implies a 20% upside potential on the one-year time horizon. Add in the dividend yield, and the stock’s total yield on the one-year time frame climbs as high as 33%. (To watch Love’s track record, click here)

Overall, there are 5 recent analyst reviews on record for Ellington, and their 4 to 1 breakdown favoring Buy over Hold gives the stock a Strong Buy consensus rating. The shares are priced at $12.47 and have an average price target of $14.50, suggesting a 16% one-year upside. (See EFC stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.