The markets have been hot these past six months. The pace of inflation is cooling off, the Federal Reserve is expected to dial back its own pace of interest rate hikes, tech stocks are booming on the strength of AI, and in all, the S&P gave five consecutive months of gains through the end of July.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

But did we just see a black swan?

Fitch cut the US government’s credit rating yesterday, from AAA to AA+, saying that the Federal government’s fiscal situation is likely to deteriorate significantly over the next three years, and specifically noting, “The repeated debt-limit political standoffs and last-minute resolutions have eroded confidence in fiscal management.”

After the announcement, stocks slumped, and now the word on everyone’s lips is ‘debt.’ The credit rating cut serves as a stark reminder to investors that the US government carries over $31 trillion in debt, and during the last debt ceiling fight, the White House warned that the stock markets could crash if the government were to default.

In response to the uncertainty, investors are looking for safer options, and defensive stocks are garnering attention. High-yield dividend stocks emerge as an attractive choice, offering some degree of protection against share depreciation by providing a steady income stream.

Against this backdrop, some Wall Street analysts have given the thumbs-up to two dividend stocks yielding 12%. Opening up the TipRanks database, we examined the details behind these two to find out what else makes them compelling buys.

Dynex Capital (DX)

First up is Dynex Capital, a real estate investment trust (REIT) with a focus on mortgage loans and securities. The company invests in these assets on a leverage basis, putting its resources into both agency and non-agency mortgage-backed securities, as well as commercial mortgage-backed securities. Dynex also maintains a set of ‘legacy’ investments in its portfolio, securitized single-family residential and commercial mortgage loans which the company originated during the 1990s.

Dynex follows some simple rules in its portfolio management, using a combination of disciplined capital allocation and comprehensive risk management to generate long term total returns with a healthy dividend component. As a REIT, Dynex is required by regulatory authorities to return profits directly to shareholders, and dividends make a convenient mode of compliance.

That dividend is paid out monthly, at a current rate of 13 cents, or 39 cents per quarter. The last dividend payment, for July, was sent out on August 1; the annualized rate of $1.56 gives a solid yield of 12%.

Dynex backs its dividend with deep pockets and plenty of liquidity. The company finished 2Q23 with over $561.5 million in cash and equivalent liquid assets, and saw its book value increase during the quarter by 40 cents, to $14.20 per share. Of interest to investors, Dynex generated a total economic return of 79 cents per share.

Among the bulls is Jones Research analyst Matthew Erdner who sees fit to rate Dynex shares as a Buy, with a $14 price target. Based on the current dividend yield and the expected price appreciation, the stock has ~21% potential total return profile.

Erdner’s comments back up his stance; he writes of the stock, “DX continues to trade at a discount to book and is cheap in comparison to agency peers. We believe DX will trade closer to agency peers as capital is deployed at wider spreads and higher coupons. Realized hedge gains, the amortization of which is taxable income, will be supportive of the dividend in 2023 and beyond, even as net interest income (NII) and traditional EAD measures remain under pressure due to higher financing costs.”

Turning now to the rest of the Street, other analysts also like what they’re seeing. 3 Buys and no Holds or Sells have been assigned in the last three months, making the consensus rating on DX a Strong Buy. Shares are priced at $12.85, and the $14.33 average price target suggests it will gain 11.5% heading into next year. (See DX stock forecast)

Chicago Atlantic Real Estate Finance (REFI)

The second stock on our list is another REIT – but one with a ‘twist,’ a particular niche that deserves a closer look. Specifically, Chicago Atlantic is the real estate lender of choice for the burgeoning cannabis sector in the US. This is not a simple niche to occupy. Cannabis, while legal for medical or recreational use in 38 states, it remains an illegal controlled substance under Federal law, a situation that puts constraints on Chicago Atlantic’s cross-state operations.

The company copes with this making a keen study of the cannabis industry’s regulatory barriers, and streamlining its operations to both maintain compliance with various state laws and maximize efficiency. Chicago Atlantic’s loan portfolio, as of the end of Q1 this year, contained commitments to $328.1 million in funding, across 24 companies. This total includes $313.9 million in current loans and $14.2 million future funding. Of the total, 88% bear a variable interest rate.

This portfolio generated $14.9 million in top-line revenue during Q1, a total that was up 51% year-over-year and beat the forecast by $476,000. The bottom line, an EPS of 60 cents per share, was 9 cents better than had been expected. The company will announce its 2Q23 results on August 9, and analysts are expecting to see a GAAP EPS of 54 cents based on total revenues of $15.08 million.

Of particular interest to dividend investors, Chicago Atlantic last declared its common share dividend payment on June 16 for the second quarter. The payment went out on June 30, at a rate of 47 cents per common share; at this rate, the dividend annualizes to $1.88 per share and gives a forward yield of 12.5%.

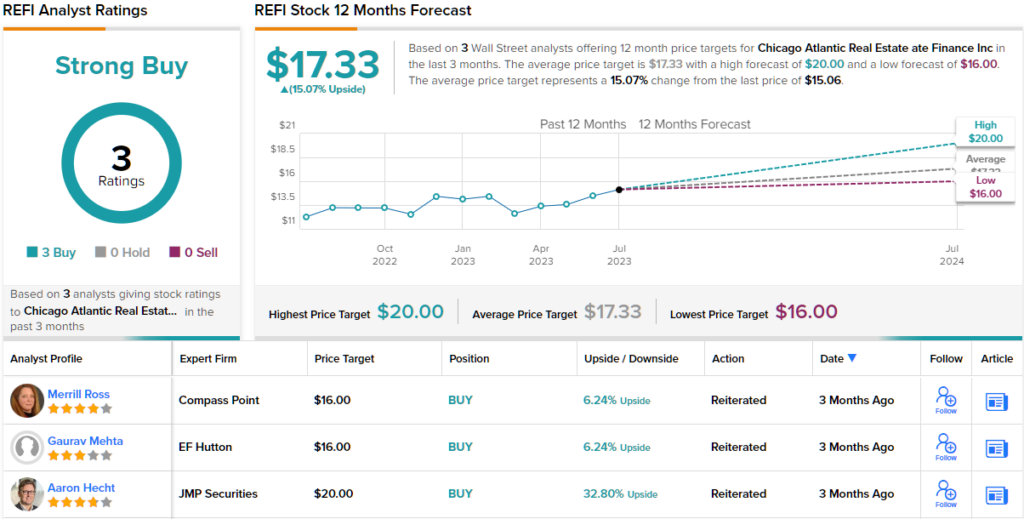

This unique REIT’s overall quality caught the eye of JMP analyst Aaron Hecht, who sees it as a solid choice for investors wanting to ‘get in’ on the expanding cannabis industry.

“The cannabis industry has felt headwinds associated with stagnant Federal regulation, declining plant prices, and limited access to capital. However, we believe REFI’s high underwriting standards, which focus on local market dynamics, cash flows, and asset coverage, materially improve the risk profile. REFI is also the only remaining pure-play cannabis mortgage REIT available in U.S. public markets… We believe capital markets availability will improve over time and we remain buyers of REFI,” Hecht wrote.

Looking ahead, Hecht gives REFI stock an Outperform (i.e. Buy) rating, with a $20 price target that implies a one-year upside potential of 32%. (To watch Hecht’s track record, click here)

Overall, REFI gets a Strong Buy consensus rating from the Street’s analysts, a sentiment that’s unanimous, as shown by the 3 positive analyst reviews on file for the stock. REFI is selling for $15.06, and its $17.33 average price target suggests that a one-year gain of 15% lies ahead. (See REFI stock forecast)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.