Despite talk of soft demand trends, sales of electric vehicles, EVs, are up 50% year-to-date in the US for 2023, and are up 25% year-to-date in China, the world’s largest automotive market. Still, there remains considerable discussion and concern regarding affordability and pricing, the capacity of the grid to support charging needs, and the availability of raw materials such as lithium and rare earth metals.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The combination has seen Big 3 automakers start to scale back their EV goals – although not to abandon them altogether. There are considerable social and political pressures to switch from fossil-fueled vehicles to EVs, and those pressures continue to support the EV market. For investors, this keeps multiple options open, including both vehicle manufacturers and those auto parts suppliers specialized for the EV segment.

The strength of specialized parts suppliers has caught the attention of Goldman Sachs’ Mark Delaney, a 5-star analyst who holds a position among the top 5% of Wall Street’s stock pros. In a recent note on US autos, and particularly the EV segment, Delaney writes, “We continue to see the best investment opportunities among the tech enablers in our broader ‘supplier’ coverage, and we note that a handful have both higher content on EVs vs. ICE vehicles and sell to a majority of EV OEMs (thus being relatively agnostic to the EV market share wars among OEMs).”

Delaney goes on to choose 2 auto-tech names that investors should consider and makes a case to buy into them now. To find out whether the rest of the Street is thinking along the same lines, we’ve also pulled up their details from the TipRanks platform; here they are, along with Delaney’s comments.

Don’t miss

- ‘Time to Hit Buy,’ Says Bank of America About These 2 Stocks

- Oppenheimer Expects the S&P 500’s Advance to Continue Into 2024 — Here’s Why These 2 Stocks Might Be Worth Buying

- Insiders Load Up on These 2 ‘Strong Buy’ Stocks — Here’s Why You Should Pay Attention

TE Connectivity (TEL)

We’ll start with TE connectivity, a company that has built its name and reputation on the strength of its electronic and digital hardware; specifically, TE specializes in the design, manufacture, and distribution of sensor and connector devices. TE’s products are found a in a variety of applications, from data communications to 5G telecom to aerospace to … the auto industry.

In the auto business, TE has product lines designed for EVs. The company’s connectors and sensors are found in battery systems, electric drivetrains, charging pathways, and auxiliary systems, and are known in the industry for their high quality. In particular, TE can design connector products capable of handling the high voltage loads of automotive batteries.

The company’s overall business is huge. TE boasts a $40-billion-plus market cap, the firm manufactures over 236 billion individual products annually, realized $16.3 billion in total sales last year, and has invested over $715 million into R&D work over the years.

At the beginning of this month, TE released its financial results for the fiscal fourth quarter (September quarter). At the top line, revenue was reported at $4 billion, while down 7.3% from the year-ago period, the figure came in $25 million above the forecast. At the bottom line, TE’s $1.78 non-GAAP earnings per diluted share was 2 cents better than the estimates.

Behind those headline numbers, TE also reported solid cash flows. Cash from operations was listed as $1.1 billion for fiscal Q4, and the free cash flow came to $945 million. Both values were company records.

These results, particularly the free cash flow, caught Delaney’s eye. “With backlog remaining near record levels, price-cost initiatives supporting improved margins, and TE benefiting from its higher content per unit for AI and EVs, we believe the company is well positioned to grow EPS and FCF going forward,” the analyst wrote. “For instance, the company attributed all of the upside in the communications segment to early traction with AI projects (vs. previous expectations for the segment to be flat qoq), and AI design wins are now ~$1.3 bn (up from ~$1 bn last quarter). FY23 FCF conversion was very strong at >110% of non-GAAP net income, and the company expects ~100% FCF conversion in FY24.”

Looking ahead, Delaney rates TEL shares as a Buy, and he gives the stock a $175 price target to imply a 31.5% one-year upside. (To watch Delaney’s track record, click here)

Overall, TE’s Strong Buy consensus rating is based on 5 recent reviews that include 4 Buys to 1 Hold. The $143.75 average price target suggests a 9% gain in the year ahead. (See TEL stock forecast)

Aptiv PLC (APTV)

The next stock on our list was born in the auto industry. Aptiv is a corporate descendant of Delphi, which was long known as a major player in Detroit’s automotive scene. Delphi spun off its powertrain and auto parts segments back in 2017, and rebranded its automotive tech platforms, on-road computing and networking, and software architecture business as Aptiv. Since then, the company has focused on developing deep software and systems integration to enable autonomous and/or connected vehicles. The company has a global footprint, with ops in 48 countries employing over 200,000 people in 11 technical centers and 131 manufacturing facilities.

Aptiv’s work is particularly applicable to EVs, as its software architecture is capable of monitoring battery and electric drive trains in real time, and its connection technology can handle everything from high-tech sensors to data transfers to safety-critical vehicle systems to high-voltage EV power couplings. Aptiv’s electrical distribution systems, originally designed to feed high-speed data transmissions from vehicle sensors to an onboard computer, are equally impressive at monitoring and controlling EV battery and electric motor powertrains. The company’s history gives it a unique ‘technology culture’ preadapted for developing the new control systems that EV powertrains will require.

When we turn to the numbers, we find that Aptiv beat the forecasts across the board in its 3Q23 financial release. The company’s $5.1 billion top line was up 11% year-over-year and came in $20 million ahead of the forecast. The bottom line, a non-GAAP earnings-per-share of $1.30, was 7 cents better than had been expected. So far this year, Aptiv has brought in $15.1 billion in sales, up 18% from this time last year, and has generated $1.27 billion in cash from operations.

For Delaney, the key here is Aptiv’s solid position in the auto industry, a position based on a sound history and facing good prospects for the future. Delaney writes, “While we appreciate that the company’s growth over market was slow in 3Q (which Aptiv attributed to the strike, customer exposure, and program timing) and that a slower EV industry production growth rate would be a headwind all else equal, we believe that Aptiv remains well positioned for growth.”

The analyst goes on to quantify his stance on this stock, giving some details behind his thinking: “Our positive view is based on Aptiv’s strong bookings/backlog, content growth opportunities and diverse customer exposure. We also believe Aptiv’s margins can improve over time, consistent with the improved 2023 profitability, growth in software (e.g., Wind River), and as it fully offsets COVID costs (we believe still ~$150 mn in 2023) and the UAW strike.”

These comments back up Delaney’s Buy rating, and his $128 price target suggests the shares have a 60% upside in the next 12 months.

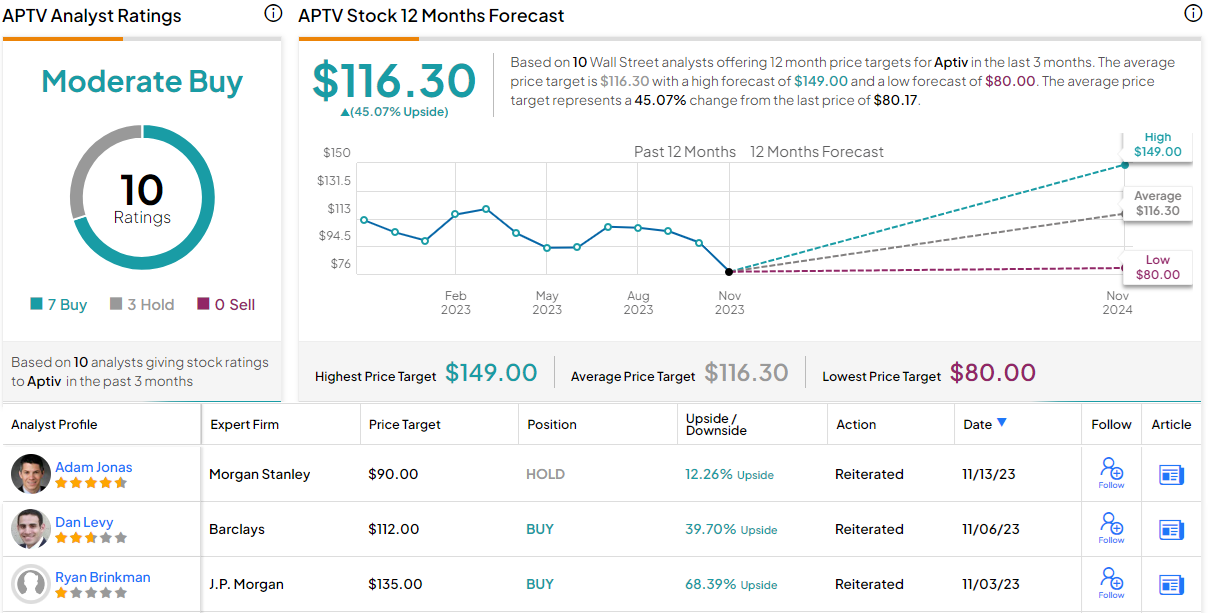

Aptiv has picked up 10 recent analyst reviews, with a 7 to 3 breakdown of Buys versus Holds, for a Moderate Buy consensus rating. The forecast calls for one-year upside of 45%, considering the average price target currently stands at $116.30. (See APTV stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.