Information technology, IT, has become a vital part of the modern business world. Since the 1990s, IT has grown in leaps and bounds – it’s no longer just about clambering under the desks to plug in an ethernet cable and has become huge business. According to Statista, revenue in the IT Services sector is expected to reach $1.364 trillion in 2024.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Big business, however, isn’t always right for every business. Doing IT right takes time and effort that could be spent on a company’s core pursuits. Hence, the rise of IT services firms, specialists in IT and related fields. IT services companies can focus strictly on the technology side, because that is their core business. For example, AI is transforming the way we interact with the digital world, and IT services firms are positioning themselves at the forefront of the new wave.

Mizuho analyst Dan Dolev tackles these developments in a recent note. “Over the last decade,” says the analyst, “the IT Services market has meaningfully grown its share of global $4-5tn IT spend, outpacing GDP growth at an accelerated pace. We expect continued focus on digital transformation, cloud adoption and the boom in AI services to drive a forecasted ~9% CAGR through 2027. The emergence of GenAI has created controversy regarding the value proposition of IT Services operators. We expect AI Services to become a sizable opportunity for the IT Services space, driving ~$450bn in spend by 2027 or ~20% of the estimated $2.1tn total IT Services spend in 2027.”

Dolev follows that with specific recommendations on two IT service stocks, ones that he describes as doing the ‘pick and shovel work’ work of the AI transition. Using the TipRanks platform, we’ve also looked up how Wall Street views these names right now. Let’s dive in.

EPAM Systems (EPAM)

We’ll start with EPAM Systems, an IT services firm that bills itself as ‘reimagining businesses through a digital lens.’ The company got its start back in 1993, as a software engineering specialist; today, EPAM offers strategic business and innovation consulting, to bridge the gap between physical and digital capabilities.

EPAM’s current work is solving problems. The company offers a wide range of services, including strategic planning, engineering, cloud services, cybersecurity, and data analytics – and it applies these to its customers’ main needs. EPAM’s experts will work with their clients to identify the real problems and to deliver answers quickly, at any scale required. More than 280 of EPAM’s customers come from the Forbes Global 2000 list, and the company has activities in more than 50 countries around the world.

In a recent announcement that gives a good example of the services EPAM offers, the company revealed last month a set of new tools, retail media accelerators for use with Google cloud. This package, developed in partnership with Google cloud, is designed to put retailers on a path toward greater efficiency and scalability.

No company is fully immune to global events, not even problem solvers. EPAM’s stock took a hard hit in early 2022, when Russia invaded Ukraine. The resulting war involved Belarus as well as Ukraine and Russia, and EPAM, which drew nearly 60% of its workforce from those three countries, could not avoid the fallout. While EPAM has been able to maintain profitable earnings since then, the company’s stock has yet to regain its pre-war levels.

Turning to EPAM’s financial results, we find that the company is scheduled to release its 4Q23 numbers in mid-February – but for now, we can look back at the Q3 figures.

Revenue in Q3 came to $1.15 billion. This was down 6% from the prior-year period, but it beat the forecast by $10 million. At the bottom line, EPAM reported its non-GAAP EPS as $2.73. Like the revenue figure, this was down year-over-year (by 37 cents per share), but was up compared to the estimates, beating the forecast by 17 cents per share.

In his coverage of EPAM for Mizuho, analyst Dolev notes the company’s high potential for expansion this year and next. He writes, “EPAM has had a difficult ’23 with weak demand due to clients’ cost optimization focus. However, we expect growth inflection in ’24 as its clients return to investing in its core innovative technology offerings and next generation technologies such as generative AI. Moreover, EPAM benefits from a strong category mix with nearly 75% of its categories in Application Implementation & Managed Services, which are expected to grow high-single-digits over the next 5-years (e.g. custom application implementation, which is expected to grow at ~9% 5-year CC CAGR). We expect EPAM’s revenue growth to start accelerating in 1Q24 driving revenues to grow +4.4% in FY24 (roughly in line with consensus) with further acceleration ahead of consensus in FY25 (+15.2% vs. cons. +14.9%).”

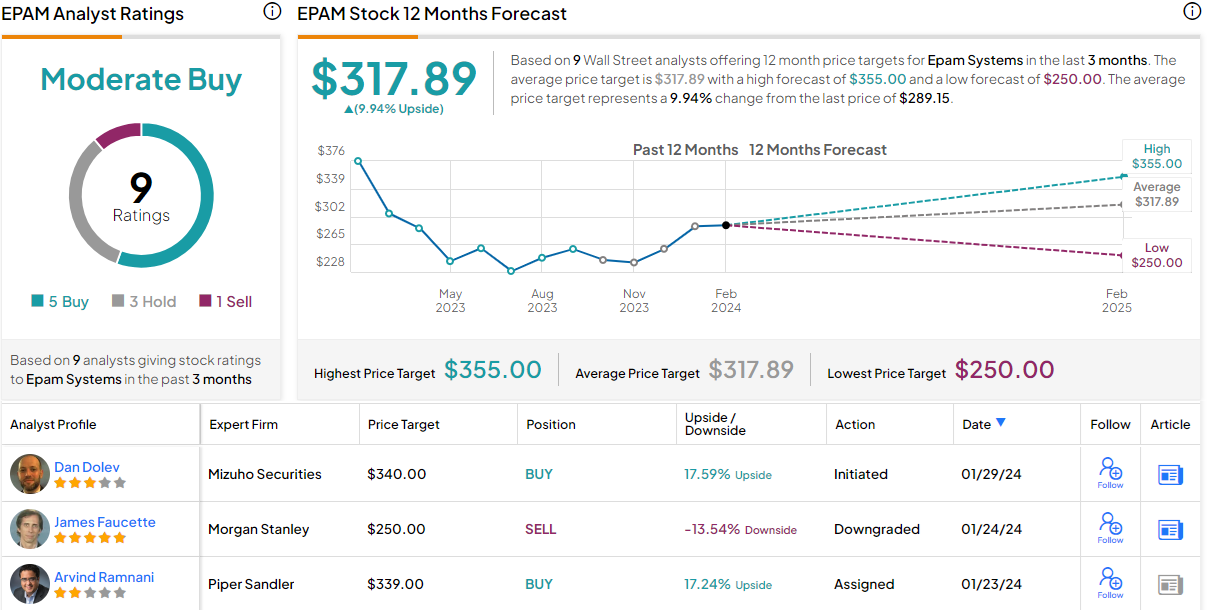

Following these comments, Dolev rates EPAM as a Buy. His $340 price target on the share implies a one-year upside potential of 17.5%. (To watch Dolev’s track record, click here)

Turning now to the rest of the Street, where the stock has 8 additional analyst reviews, and those break down to 4 Buys, 3 Holds, and 1 Sell – for a Moderate Buy consensus rating. EPAM is currently trading for $289.15, and its $317.89 average target price points toward a one-year gain of 10%. (See EPAM stock forecast)

Globant SA (GLOB)

The second stock we’re looking at, Globant, is a global leader in the field of AI services. The firm got its start in 2003 and today has grown into a $10 billion player in the tech world. Globant makes extensive use of AI technology in its tech services and platforms, to transform each client’s business outlook. The company also operates digital media studios, an essential asset for building a presence in today’s online world.

On a note of particular interest, Global is using AI in its digital transformation platforms. The technology is proving especially useful in reinventing the way that software packages are coded and tested.

Globant counts some of the world’s more recognizable names among its customer base, including Google, Electronic Arts, and Santander. The company employs over 27,500 people in 30 countries around the world, and its international nature is clear from its history: Globant got started in Buenos Aires, but today is headquartered in Luxembourg, and its chief clients are located in the US and the UK.

In recent months, Globant has been expanding its footprint. In December, the company announced its acquisition of Iteris, the Brazilian business and tech consultancy firm. The Sao Paolo-based company will bring additional digital capabilities to Globant, and expand the firm’s Brazilian position with 600 employees and an ‘impressive client roster.’ Globant’s management describes Brazil as one of the company’s ‘top bets’ in Latin America. And, in January, Globant opened its first Business Innovation Hub in Berlin. This is a space designed to highlight Globant’s capabilities and expand its German presence while fostering and including local talent.

Turning to the financial side, Globant’s last earnings release, publicized in November for 3Q23, showed revenues in-line with the forecast at $545.3 million, and earnings one cent better than predicted, at $1.48 by non-GAAP measures. For Q4, Globant expects revenue of at least $579 million, amounting to 18% YoY growth, and adj. EPS of at least $1.60. The company will release its 4Q23 results on February 15.

In covering this stock for Mizuho, analyst Dolev takes note of Globant’s AI initiatives, seeing those as key to the company’s positioning and success. He writes, “We believe Globant has taken a leadership position in AI services. Management often cites AI as having its ‘iPhone moment’ and we believe the company is competitively positioned to continue to gain share in next-generation technologies (GenAI, ML, data analytics, etc.). We highlight GLOB’s early AI success with the company seeing $100mn in revenue or ~7% of YTD 2023 revenue in projects with AI components… We expect strong organic growth & top-line execution to continue. Between 2017 – 2019, organic growth neared +22%, over 4x above the weighted average growth of GLOB’s categories. Growth improved to ~33%, widening the excess growth vs. the GLOB’s weighted average category growth.”

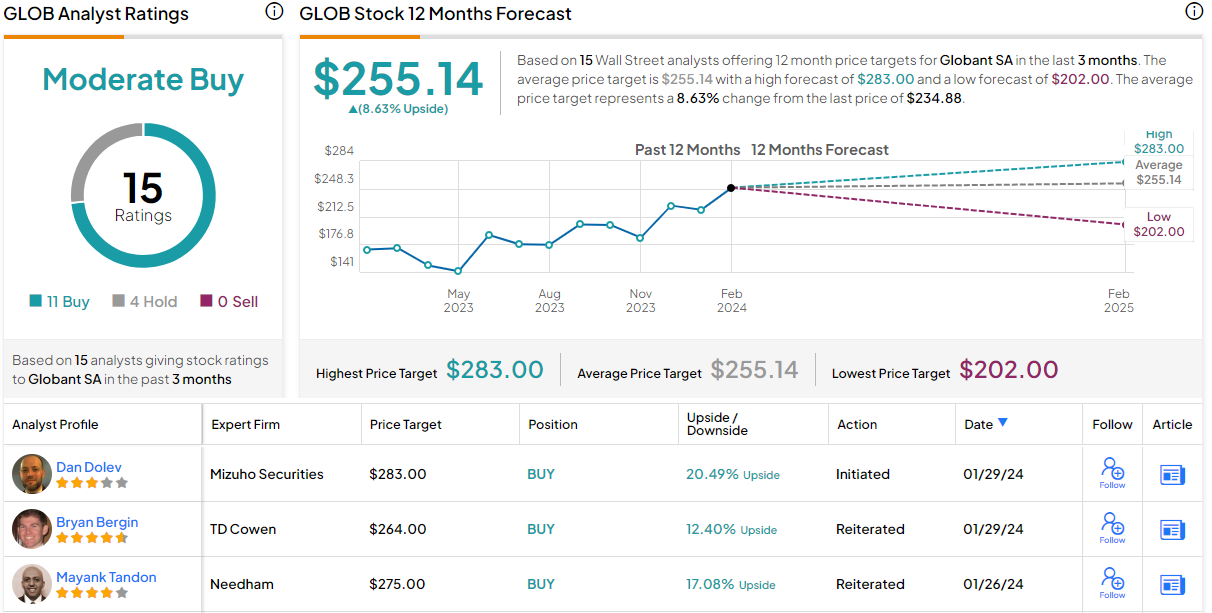

At the bottom line, Dolev gives this stock a Buy rating, with a $283 price target that points toward a 20.5% upside potential for the next year.

On balance, Wall Street is willing to buy in here; the 15 recent analyst reviews include 11 to Buy against 4 to Hold, for a Moderate Buy consensus rating. The $255.14 average price target implies an 8.5% one-year increase from the current trading price of $234.88. (See Globant stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.