Big-box retailer Target (NYSE:TGT) saw its shares rise by about 3% on Wednesday, as investors cheered the company’s better-than-anticipated second-quarter earnings. However, Q2 FY23 sales declined and lagged expectations, reflecting the impact of multiple headwinds, including culture wars over pride month displays and macro pressures. The company lowered its full-year sales and earnings guidance to reflect further trouble.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Target’s Sales Remain Under Pressure

Target’s Q2 FY23 overall revenue declined 4.9% year-over-year to $24.8 billion, with comparable sales down 5.4% against analysts’ expectation of a 3.7% drop. In particular, comparable store sales fell 4.3%, while comparable digital sales declined 10.5%.

Management said that trends in discretionary categories continued to be weak due to macro challenges and softened further in Q2 FY23. Amid high inflation, consumers have been directing their dollars toward food and essentials.

Traffic at Target’s stores and its sales were also hit by the backlash for the company’s Pride month assortment, which was launched in mid-May. Target pulled some items from display after employees at several stores received threats from some shoppers. However, the decision to remove certain merchandise didn’t go down well with the LGBTQ+ community, which called for a ban on the retailer. Alcoholic beverage giant Anheuser-Busch InBev (NYSE:BUD) was also caught in the LGBTQ+ controversy due to a marketing campaign related to its Bud Light brand.

Another aspect impacting Target’s performance is retail theft or “shrink.” Management said that while shrink in the second quarter was consistent with their expectations, it was well above the sustainable level at which the company expects to operate over time. During the first five months of this year, Target’s stores saw a 120% rise in theft incidents.

While the impact of the LGBTQ+ controversy is expected to fade, Target’s higher exposure to discretionary categories compared to peers like Walmart (NYSE:WMT) might continue to weigh on the company’s top line, as macro challenges impact consumer spending.

Moreover, spending patterns might get impacted in the days ahead by the end of the student loan moratorium on August 30. The end of the student loan moratorium is expected to have a $10 billion impact on consumers’ wallets, as per some estimates cited by a Wall Street Journal report.

The impact of macro uncertainty reflects in Target’s revised guidance. The retailer now expects full-year comparable sales to decline by about mid-single digits and EPS in the range of $7 to $8. The company had previously expected a low single-digit decline to a low single-digit increase in comparable sales and EPS between $7.75 and $8.75.

Is Target a Buy or Hold?

Despite Wednesday’s gain, TGT stock is down about 14% year-to-date.

Following the Q2 print, Baird analyst Peter Benedict lowered his price target for TGT to $165 from $190 but reiterated a Buy rating on the stock. The analyst said that stronger earnings performance offset the sales shortfall. He added that Target’s ability to deliver a 25% earnings upside despite softer-than-anticipated sales gives “some comfort” about its longer-term margin recapture opportunity.

Also, Goldman Sachs analyst Kate McShane lowered the price target for TGT to $168 from $185 and reaffirmed a Buy rating. The analyst views the Q2 performance as a “clearing event,” that shifts the focus to the margin recovery opportunity over the next year. Nonetheless, McShane acknowledged that some investor concerns remain with regard to market share and ongoing weakness in discretionary goods spending.

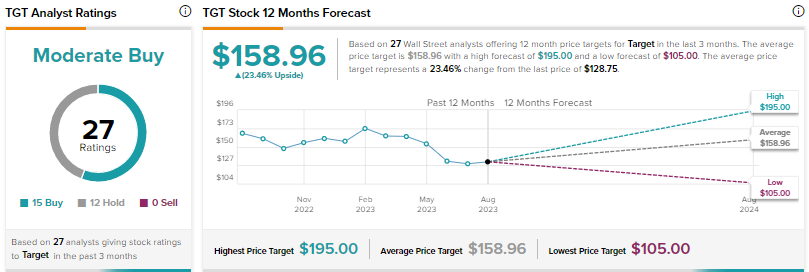

Overall, Wall Street is cautiously optimistic on Target, with a Moderate Buy consensus rating based on 15 Buys and 12 Holds. The average price target of $158.96 implies 23.5% upside.

Conclusion

While Target impressed investors with its fiscal second-quarter earnings performance, concerns about the continued weakness in the company’s sales could weigh on investor sentiment in the days ahead.