Taiwan Semiconductor stock (NYSE:TSM) rallied significantly following its Q4 results, which set the stage for accelerating growth. The leading global semiconductor foundry, specializing in manufacturing advanced integrated circuits for a wide range of electronic devices, ended Fiscal 2023 on a seemingly weak note. However, setting aside the temporary impact of the industry’s cyclical nature, Taiwan Semiconductor’s innovative advancements promise strong growth. Accordingly, I remain bullish on the stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Were TSM’s Fiscal 2023 Results Actually Weak?

Upon initially looking at the numbers, TSM’s Q4 and Fiscal 2023 results may seem lackluster. Annual revenues saw a decline of 8.7% to $69.3 billion, accompanied by a 5.2-percentage-point drop in its gross margin to 54.4% and a 6.9-percentage-point decrease in its operating margin to 42.6%. Consequently, earnings per ADR for the year took a notable hit, plummeting by 17.5% to $5.18.

These figures might not inspire confidence. However, a deeper look into the numbers reveals a more encouraging story, as this downturn was within expectations. More importantly, a substantial growth rebound is anticipated from this point onward. Let’s address each aspect, starting with what caused TSM’s results to decline last year.

Essentially, TSM’s gloomy results in 2023 resulted from the semiconductor industry’s cyclical nature. The industry experiences periodic fluctuations in sales, as they are highly correlated to the increasing sales of smartphones, powerful GPUs, and even automobiles that make use of chips.

For example, TSM showcased remarkable growth in smartphone semiconductor sales, experiencing a notable 27% surge quarter-over-quarter in Q4. Additionally, the company saw a commendable 13% uptick in automotive semiconductor sales during this period. However, this positive momentum was more than offset by a downturn in the Internet of Things and Direct Consumer Electronics categories, whose revenues declined by 29% and 35%, respectively.

Such industry-specific cyclicalities are par for the course, impacting the entire semiconductor industry, and TSM, being a major player, is not immune.

Nanometer Advancements Are Far More Important

Given the unpredictable course of the underlying industries TSM serves, what warrants closer attention is the fundamental progress TSM is achieving in advancing chip fabrication. This progress is what eventually enables the company to capitalize on the forthcoming mega trends in technology. Today’s mega trends include high-performance computing (HPC), artificial intelligence (AI), and 5G.

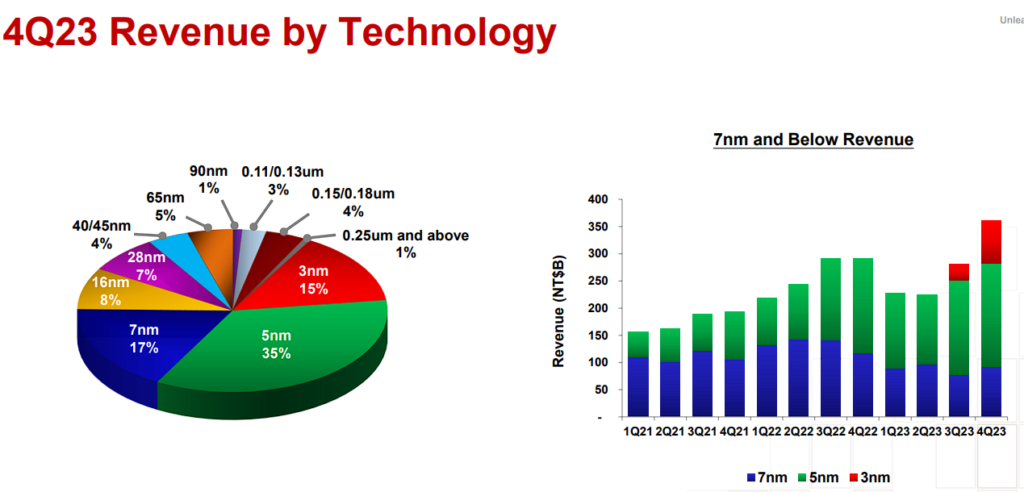

TSM has diligently pursued this path, evidenced by its industry-leading 3-nanometer tech production ramping up. Remarkably, Q4 marked only the second quarter of 3-nanometer chips entering the market, yet they contributed 15% of wafer revenue during that period (refer to the revenue mix pie chart below).

The growing demand and adoption of 3-nanometer chips are vividly illustrated in the accompanying bar chart, where these new innovative chips almost rival the sales of the now-mature 7-nanometer chips.

It’s worth mentioning that one of the reasons TSM’s gross margin declined last year was precisely this ramp-up of 3-nanometer production capabilities. With the 3-nanometer set to see continuous adoption and TSM set to achieve improving unit economics as production revs, both revenues and earnings are set to rebound massively from 2024 onward.

In particular, TSM’s management forecasts that revenues remain well on track to grow by a compound annual growth rate between 15% and 20% over the next several years. Therefore, consensus estimates forecast revenue growth of 23.8% in Fiscal 2024, followed by further growth of 18.7% in Fiscal 2025. Earnings per ADR are also expected to grow by 20% in both years.

Interestingly, Fiscal 2025’s earnings per ADR consensus estimate of $7.72 implies a forward multiple of about 15 at the stock’s current price levels. In my view, that’s not an expensive multiple, given TSM’s one-of-a-kind qualities, mission-critical position in the industry, and long-term growth prospects. Thus, even though the stock rallied notably after the earnings release, I believe that TSM may have further upside ahead.

Is TSM Stock a Buy, According to Analysts?

Regarding Wall Street’s view on the stock, TSM has a Strong Buy consensus rating based on five Buy ratings assigned in the past three months. At $138.60, the average TSM stock forecast implies 16.1% upside potential.

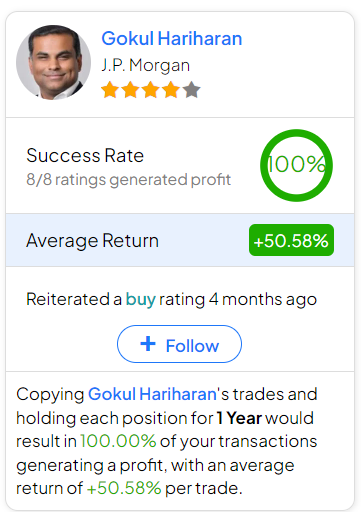

If you’re wondering which analyst you should follow if you want to buy and sell TSM stock, the most profitable analyst covering the stock (on a one-year timeframe) is Gokul Hariharan of JPMorgan (NYSE:JPM), with an average return of 50.58% per rating and a 100% success rate. Click on the image below to learn more.

The Takeaway

In conclusion, while Taiwan Semiconductor’s Fiscal 2023 results may appear lackluster at first glance, they were primarily influenced by the cyclical nature of the semiconductor industry — not company-specific challenges.

Meanwhile, the company consistently progressed in innovating within the industry. TSM’s emphasis on advancing chip fabrication technology, particularly with its 3-nanometer production, has now positioned it for significant growth.

With strong demand for these innovative chips and an optimistic revenue outlook, TSM’s revenues and earnings are well-positioned to rebound in 2024 and beyond. Coupled with the company’s unique qualities and long-term growth prospects, I maintain a bullish stance on TSM, anticipating further upside despite recent highs.