Iconic Seattle-based coffee company Starbucks Corporation (SBUX) owns and franchises more than 34,600 stores across the globe. The company was notably impacted during the midst of the pandemic as its operations, and opening conditions were disrupted. As a result, revenues in fiscal 2020 came in at $23.5 billion, lower than fiscal 2019’s $26.5 billion. In fiscal 2021, the company’s growth trajectory resumed, with revenues hitting a new all-time high of $29.0 billion.

Starbucks’ recovery momentum endured strong as the company entered fiscal 2022, as it reported the best Q1 results in its history. Yet, shares of the company have struggled lately, having lost one-third of their value over the past year. In fact, Starbucks shares are currently hovering at the same levels they did in mid-2019.

In my view, Starbucks remains a top dividend-growth pick. As a result, the recent pullback could present a fruitful opportunity, especially for dividend growth investors who would previously avoid the stock due to its risk profile.

Besides Starbucks’ financials and dividend growth prospects remaining strong, in fact, the dividend yield is currently hovering close to 2.5%, which is at the high-end of the stock’s historical range.

I remain bullish on Starbucks.

Driving Through Difficulties

Starbucks reported fiscal Q2 2022 results retained the company’s recovery momentum. Revenues grew 15% year-over-year to $7.6 billion. Results were mainly powered by 17% revenue growth in the U.S., and excellent performance across its vast global location portfolio.

The company’s results also demonstrate its brand’s strength, despite the underlying challenges. These include the invasion of Ukraine, macroeconomic tensions, concerns over consumers’ purchasing power, and elevated inflation levels. While one could wonder how these factors could affect Starbucks’ results, remember that Starbucks’ coffees are considered a high-end product in the industry, and they are being priced at a premium. Thus, any weakness in consumers’ purchasing power could easily be reflected in the underlying numbers.

Impressively, the case appeared to be completely the other way around in its latest results. Despite the revenues growing over last year’s already recovered numbers, sales volumes actually grew in light of higher pricing.

Specifically, North America delivered revenues of $5.4 billion for the quarter, suggesting a year-over-year increase of 17%. The increase included a 12% gain in comparable-store sales comprising of a 7% advance in average ticket and a 5% rise in transactions.

As management mentioned during the earnings call, the company’s average ticket reached an all-time high, powered by strategic beverage pricing and another record-breaking quarter of food attached to beverage sales. Food sales, in fact, grew 25% year-over-year. Besides this indication that the consumers’ purchasing power remains strong, it also highlights Starbucks’ brand value and its ability to meaningfully raise prices that are accretive to results.

Even so, inflationary forces offset the company’s price increases. Operating margins declined by a significant 520 basis points. This decline included sweetened store partner wages and new partner training. The lapping of prior year government subsidies also contributed to the drop. Earnings per share grew 3.6% to $0.58, partially boosted by a lower share count, nonetheless.

Valuation & Dividend Growth

Due to the uncertainty around additional mobility restrictions and lockdowns in China resulting from the government’s strict zero-COVID policies as well as advancing inflationary headwinds, the company did not provide specific guidance. However, consensus EPS estimates for fiscal 2022 point towards $2.87.

This implies a P/E of 27.6 at the stock’s current price levels, which is admittedly a pricy multiple in a rising-rates environment. However, one has to consider two factors that could justify it. Firstly, revenue growth remains in the double-digits. Secondly, margins are likely to expand higher once inflation eases. These two factors combined should result in an EPS CAGR north of 20% in the coming years, according to analysts.

Robust EPS growth in the coming years should also allow for Starbucks’ vigorous dividend growth momentum to be sustained.

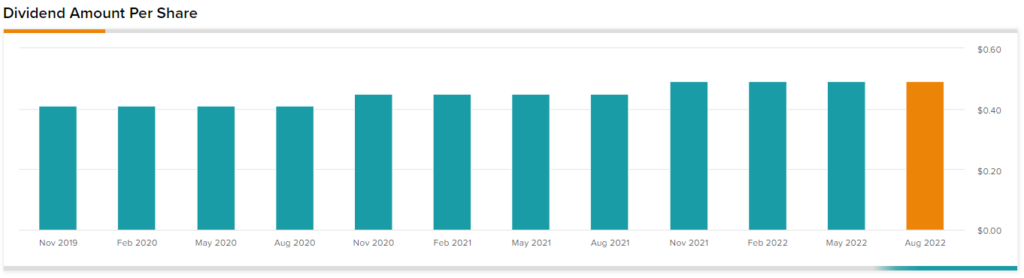

Starbucks’ five-year DPS CAGR currently stands close to 15%. The most recent increase back in September was by 8.9% to a quarterly rate of $0.49. According to management’s guidance, this implies a payout ratio close to 68%. The ratio appears to be somewhat worrying. However, we stress that this is due to the ongoing contraction in margins and that is it likely to normalize from next year.

Wall Street’s Take

Turning to Wall Street, Starbucks has a Moderate Buy consensus rating based on 12 Buys and nine Holds assigned in the past three months. At $93.62, the average Starbucks price target implies 18.09% upside potential over the next 12 months.

Conclusion

Starbucks is presently trading at the same levels it did more than three years ago. However, multiple advancements have occurred since, including the company’s revenues breaching new all-time high levels. While inflationary pressures are squeezing this year’s profitability, the company’s pricing power is being proven to be fantastic.

Shares could appear somewhat expensively priced, though the valuation is likely to normalize once margins return to their historical average. In the meantime, Starbucks’ yield is standing at the high end of its 10-year range and the company’s dividend growth prospects remain. Hence, dividend-growth investors may want to consider Starbucks for their portfolios.