Shares of Shopify (NYSE: SHOP) have cratered 77.5% this year amid the broader market sell-off. Investors have been concerned about Shopify’s slowing growth rates and profitability, as well as its ability to navigate tough market conditions in the days ahead.

However, Roth Capital Partners analyst Darren Aftahi continues to believe that SHOP’s topline results could very well meet expectations. Let us look at the reasoning behind the analyst’s expectation.

The analyst recently did a channel check for SHOP where he surveyed merchants on SHOP throughout June and early July for second quarter trends.

A Slowdown in Business for SHOP Merchants

Shopify’s e-commerce platform helps merchants sell their products and offers tools that enable them to grow and manage their businesses.

Analyst Aftahi’s survey indicated that merchants on Shopify saw their businesses grow by 23% year-over-year versus last quarter’s survey for 1Q22, which indicated a growth of 27% year-over-year – a deceleration in growth.

The analyst is of the view that even with soaring inflation, Shopify is “likely the best-positioned e-commerce/retailer in the space due to its multi-prong approach with both online and in-store applications serving businesses of all sizes, especially with the growth of its Plus network.”

Consumption Pullback Likely to Lower SHOP’s Growth Outlook

Aftahi believes that if retail spending and consumption continue to slow down as a result of inflationary pressures, it could lead to “a lower outlook for growth.”

However, the analyst believes that even if such a deceleration happens, it is likely to be offset by SHOP’s expansion in international markets, which according to Aftahi, has yet to feature “ancillary services, acting as lower hanging fruit that could keep SHOP’s topline growth near or above 20% y/y in FY23.”

Moreover, Aftahi pointed out that while SHOP’s heavy investments in research and development, data, and marketing were compressing operating margins, “we believe the potential risk of earnings compression is limited as our model already considers similar investment trends in FY23, and any upside from a more normalized spend rate (sub 50% OpEx as a % of revenue) would likely see FY22 be a trough in terms of losses.”

Indeed, in Q1, SHOP’s adjusted operating income came in at $31.9 million versus $210.8 million in the same period a year ago as the company “bolstered our R&D, data and sales teams and stepped up performance marketing in both North America and internationally.”

SHOP Benefits from Deliverr Acquisition

Analyst Aftahi also sees the $2.1 billion Deliverr acquisition as a success. Deliverr, founded in 2017, is a fulfillment technology provider.

The analyst believes that this acquisition is likely to strengthen Shopify’s “logistics, fulfillment, and warehousing capabilities for merchants as it looks to offer a full suite of logistic services to merchants.”

Analyst Aftahi, however, remains sidelined on the stock with a Hold rating and a price target of $40 on the stock. The analyst’s price target implies an upside potential of 30.4% at current levels.

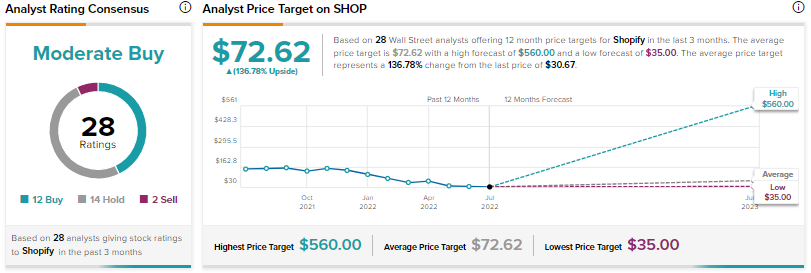

Overall, Wall Street analysts are cautiously optimistic about Shopify with a Moderate Buy consensus rating based on 12 Buys, 14 Holds, and two Sells. The average Shopify price target of $72.62 implies an upside potential of 136.8% at current levels.

Conclusion

While analyst Aftahi is optimistic about SHOP’s topline results, it is still unclear how much the rising inflation will affect SHOP’s Q2 results.

Interestingly, investors continue to be very positive about the stock as indicated by the TipRanks Crowd Wisdom tool. This tool indicates that top investors on TipRanks have increased their holding of Shopify stock by 13% in the past 30 days.