Even taking some recent dips into account, the S&P 500 remains near its record-high level – so why is one prominent market watcher sounding the alarm?

In a recent note, B. Riley’s chief investment strategist Paul Dietrich lays out the warning case for investors, drawing attention to several signs that indicate a cloudy future. Several of these are technical factors, while others are more anecdotal in nature. Among the latter, Dietrich cites recent large-scale stock sales from the likes of Jeff Bezos, Jamie Dimon, and Mark Zuckerberg, as well as the $168 billion cash pile built up at Berkshire Hathaway.

“When the smart money is selling out as the market is hitting record highs,” Dietrich says, “they are telling us something.” The strategist goes on to elaborate, painting a picture of difficult times ahead: “I still believe there is a strong possibility the economy will go into a mild recession this year. That means it is possible we could see a total drop from the current overvalued stock market of -49%.”

That’s a big decline. In an environment like this, the natural inclination for investors is a shift toward defensive plays, the classic move being high-yield dividend stocks. These equities will provide a sound income stream, even if markets turn down, and the high yield will ensure a return that beats the rate of inflation.

The Street’s analysts have not been shy about suggesting dividend stocks to buy – and for investors seeking high yields, of at least 9%, these two choices may be right.

International Seaways (INSW)

We’ll start with a shipping company, International Seaways. This is an owner-operator of oceangoing tanker vessels, the big ships that transport crude oil and other hydrocarbons around the world and form a vital link in the global energy supply chain.

International Seaways has a fleet of 77 vessels, which includes 13 VLCCs and 13 Suezmaxes, the largest of the tanker types that ply the seas. The VLCCs weigh in with a dry weight tonnage (DWT) of approximately 300,000 tons, while the Suezmax vessels are between 150,000 and 160,000 tons. The rest of the company’s fleet is composed of the smaller Aframax, LR, and MR ship types.

The fleet itself is considered modern. The oldest vessels date back to 2007, but most are considerably younger. Several of the VLCCs were built in 2023, and four ships in the LR class are currently under construction, with service deliveries scheduled for 2025 and 2026. The company’s fleet works under the charter system and moves crude oil, petroleum products, and other chemicals around the world. International Seaways has an active program to modernize its fleet and to optimize it for efficient operations.

At the end of February, this mid-cap (market cap of $2.63 billion) shipping company reported its financial results for 4Q23 and beat analyst expectations. The firm’s revenue came to $250.73 million, down almost 26% year-over-year but also $12.81 million ahead of the forecast. The bottom-line earnings, the non-GAAP EPS of $2.18, beat the estimates by a dime.

For dividend investors, this company offers some solid inducements to buy in. The stock pays out a regular common share dividend, which was declared in February and paid out in March at a rate of 12 cents per common share. The forward yield of this, based on the annualized payment of 48 cents per share, is decidedly modest at just under 1%. But – the company also pays out a special dividend, adjusted as needed to match management’s capital return goals. The last special dividend was declared for $1.20 per share and was paid out on March 28. With the special div, the total estimated forward yield comes to 9.8%.

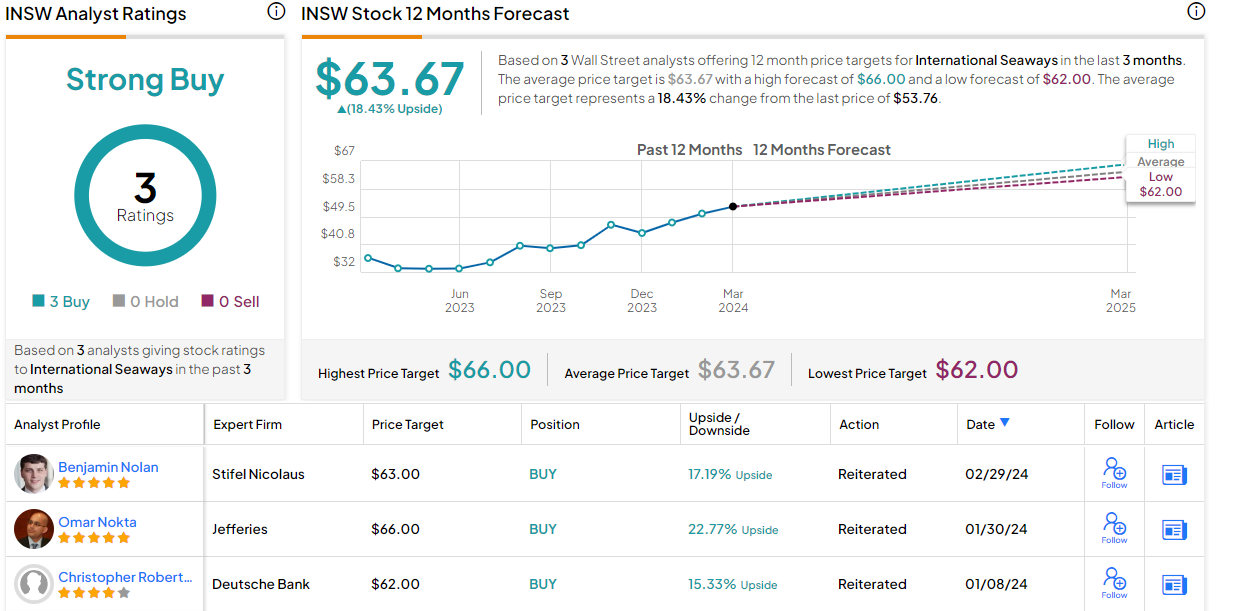

Stifel’s 5-star analyst Benjamin Nolan lists several advantages that INSW shares offer investors, starting with its general strong position and including its reliable dividend: “Things are going very well at International Seaways; strong market fundamentals are fueling strong earnings which in turn has allowed the company to strengthen the balance sheet, increase shareholder returns, and renew its fleet. We expect this dynamic to continue and INSW shares should drift higher as net income is generated.”

These comments support Nolan’s Buy rating on the stock, while his $63 price target points toward a one-year upside of 17%. Together with the dividend yield, the total return may hit as high as ~27% in the coming year. (To watch Nolan’s track record, click here)

While there are only 3 recent analyst reviews here, they point toward a stock to buy – they are unanimously positive, for a Strong Buy consensus rating. The shares are trading for $53.76 and have an average target price of $63.67, together suggesting an 18.5% gain on the one-year horizon. (See INSW stock forecast)

Rithm Capital (RITM)

From the seaways, we’ll shift our focus to dry land, where Rithm Capital works as a REIT, a real estate investment trust. These companies bring real properties into the stock market, by buying, owning, managing, and leasing a wide range of real estate investments; they will also invest in mortgages, mortgage-backed securities, mortgage servicing rights, and other assets related to the real estate market. Due to tax regulations and compliance procedures, REITs typically pay out a high-yield dividend and are well-known as dividend champions.

That said, Rithm Capital invests in a wide range of assets, including residential mortgage loans, consumer loans, business purpose loans, and mortgage servicing rights. In addition, the company also invests directly in commercial real estate and in single-family rental homes. Together, this adds up to a highly diverse portfolio, with $35 billion in assets and $7 billion in total equity.

This past March, Rithm declared its common share dividend for an April 26 payment. The dividend, of 25 cents per share, annualizes to an even $1 and gives an estimated forward yield of 9.2%. In addition to the dividend payment, Rithm has also approved a $200 million buyback of common stock shares.

The company’s dividend was supported by positive earnings. Rithm reported for 4Q23 an ‘earnings available for distribution’ total of $247.4 million, which came out to $0.51 per common share – a figure that was double the actual dividend paid out per share. We should note that the company’s revenues were down year-over-year, at $626.79 million, by almost 18%.

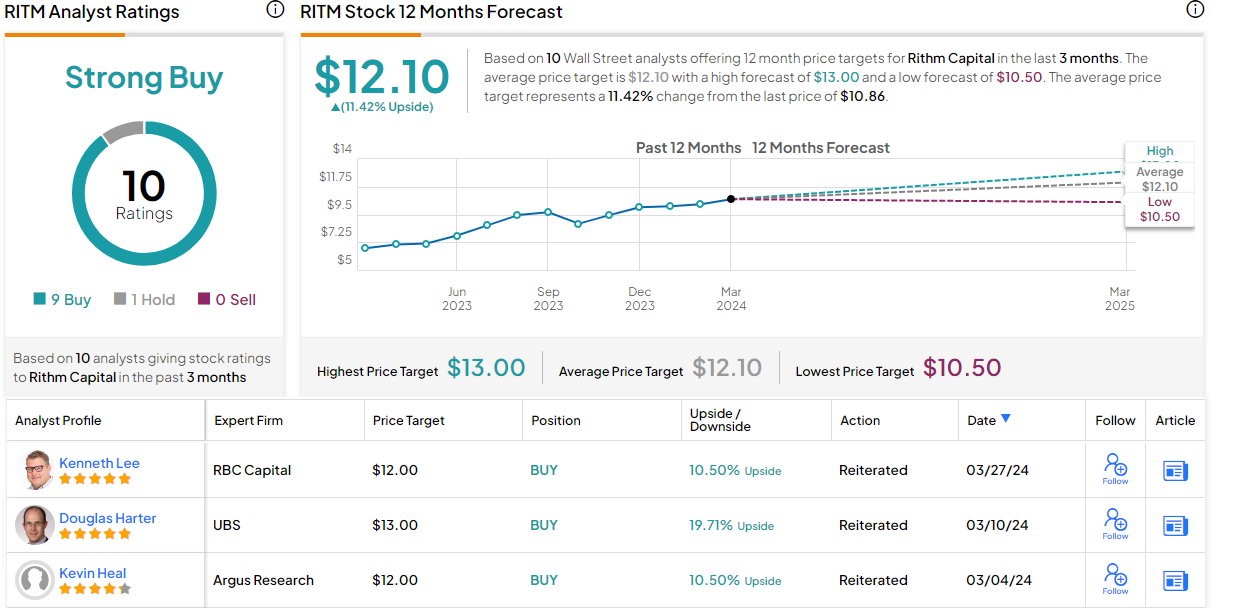

The revenue drop did not prevent BTIG analyst Eric Hagen from taking an upbeat stance here. Hagen gives a list of reasons why investor should buy this stock, but finishes with his belief that Rithm’s high-yield dividend is safe, saying, “Owning RITM stock today represents the opportunity to capitalize a de-novo asset manager before it gets birthed from the existing infrastructure in the mortgage REIT… We especially see potential value if shareholders are also given the opportunity to own any vehicles spun out of RITM, or made more accessible for investment as a result of changes to the corporate structure. It’s all admittedly amorphous to back into with a sum of the parts right now, but we’re comfortable saying it’s worthy of upside if an asset manager has a sustainable capital structure which fosters growth, and the vehicles beneath it are also in a position to scale-up, especially if there are inexpensive targets to acquire in order to scale-up quickly. While we wait for it to come together, we’re getting a 9.5% (at the time of writing) dividend yield which we think is stable in both higher- and lower-rate scenarios.”

Hagen goes on to rate the shares as a Buy, with a $13 price target suggesting a 20% gain in the next 12 months. Add in the dividend, and the total return could reach as high as 29%. (To watch Hagen’s track record, click here)

The 10 recent analyst reviews on this stock break down 9 to 1 in favor of Buy over Hold, for a Strong Buy consensus rating. The shares have a trading price of $10.86 and their $12.1 average target price indicates potential for an 11.5% upside over the next year. (See RITM stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.