It’s been a forgettable past year for shares of Salesforce (NYSE:CRM) and its CEO Marc Benioff. With big layoffs, macro headwinds, and slowed growth weighing on sentiment, questions linger as to whether activist investor involvement can help the cloud giant return to its former glory in a hostile environment for tech. Despite the headwinds and sagging share price, I remain bullish as a handful of activists look to extract value amid the firm’s journey to improve its margins.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Activists are Right to Push for Change

Benioff may be a smart top boss, but it hasn’t all been smooth sailing for the cloud-based SaaS (Software-as-a-Service) pioneer over the past few years. In a span of around five years, two co-CEOs (Bret Taylor and Keith Block) stepped up alongside Benioff, only to step down soon after. In the case of Taylor, it was incredibly soon after.

Such moves do not inspire my confidence in the company’s succession plans. Further, I think activism is needed to help the software behemoth that may have wandered too far off the trail.

It isn’t just co-CEO exits that I find troubling. In December, the untimely departure of Slack founder Stewart Butterfield left a pretty bad taste in the mouths of investors as shares crumbled to multi-year lows. Tableau CEO Mark Nelson also stepped down, marking the third big resignation in just a few days.

Salesforce’s Slack and Tableau acquisitions didn’t come cheap. However, I was willing to give the cloud giant the benefit of the doubt. After all, Salesforce wasn’t just acquiring popular platforms and their customers but also the talent working hard at each acquired firm.

Now that Butterfield and Nelson have departed alongside thousands of other employees amid Salesforce’s corporate restructuring, the firm has shed quite a bit of talent. Whether the leaner, low-rate-world version of Salesforce can continue to grow while improving profitability metrics remains to be seen.

Morgan Stanley (NYSE:MS) analyst Keith Weiss seems to think Salesforce’s earnings could receive a jolt following mass layoffs and activism. In a recent note, Weiss sees a “significant opportunity” for the company to “improve efficiency,” with expectations for growth to “return to at least market growth” of 13% alongside “non-GAAP operating margins nicely above 30%.”

I think Morgan Stanley is right about Salesforce as it looks to go from full-on growth mode to margin-enhancement mode with a bit of help from three well-known activists. There seems to be quite a bit of locked-up value that may need the help of an outsider to squeeze out.

More Gains Could be Ahead for CRM Stock

Salesforce stock has been on a roll so far this year. With potential catalysts (activists and a greater margin-centric focus) in sight, 2023 may be the year the firm regains investors’ faith. Year-to-date, Salesforce stock is up 27%. Sure, the broader basket of tech stocks is up considerably on the year. However, I think the hope produced by activists is a bigger contributor to CRM stock’s steep ricochet off the bottom.

Even after its significant bounce off December’s lows, CRM stock is still 45% away from its late-2021 peak. Such levels may not be as far out of sight as they seem, especially if activists Starboard and Elliot Capital Management have their way.

Undoubtedly, the acquisition of Slack was met with investor distaste back in 2021. The deal was expensive ($27.7 billion), seemingly untimely, and acted as quite an overhang on the stock.

Still, I think there’s a good chance activists pressure Salesforce to divest some of its past acquisitions, including Slack, to unlock value. However, given how far tech valuations have plunged over the past year, it’s doubtful that Salesforce will get anything in the ballpark of $28 billion.

Regardless, the fate of Slack (and possibly Tableau) could be up in the air as activists look to disrupt Salesforce’s original plans. In any case, the recent departures of top bosses from both acquired firms could imply big changes up ahead for Slack and Tableau.

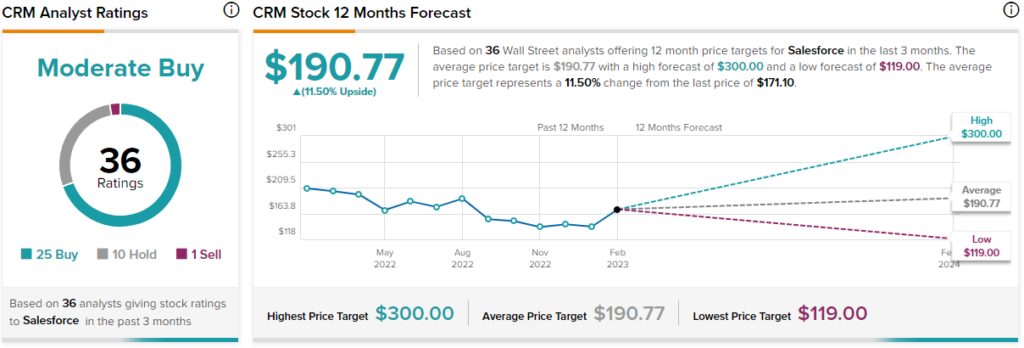

Is CRM Stock a Buy, According to Analysts?

Turning to Wall Street, CRM stock comes in as a Moderate Buy. Out of 36 analyst ratings, there are 25 Buys, 10 Holds, and one Sell recommendation.

The average Salesforce stock price target is $190.77, implying an upside of 11.5%. Analyst price targets range from a low of $119.00 per share to a high of $300.00 per share.

The Bottom Line on Salesforce Stock

After the latest round of employee exits, I think activist investors are right to step in to lend a helping hand. Investors seem to applaud the activism, given the stock’s January jump.

At this juncture, expectations are quite muted, with a looming recession likely to pave the way for more rocky quarters. As activists look to work their magic, the stage may be set for positive surprises, with or without significant divestitures.