RH (RH) operates as a holding company that operates the business through its subsidiary Restoration Hardware, Inc. It offers furniture, lighting, textiles, decor, outdoor and garden products, and more.

The company has multiple distribution channels, including galleries, source books, and websites. We are bullish on the stock.

RH’s Large Price Decline

Following the company’s most recent earnings call, the price of the stock fell substantially. The reason was due to the CEO’s pessimistic tone, which spooked investors.

The CEO explained that since the start of the war in Ukraine, demand for products has softened. In addition, he went on to say that historically speaking, the Federal Reserve has created recessions more times than not during a rate hiking cycle.

In essence, the CEO is not too confident that the Federal Reserve will be able to pull off a “soft landing,” meaning raising rates without causing a recession.

However, there are a few things investors shouldn’t forget about RH. To begin with, the company is still expecting 5-7% growth in revenue for Fiscal Year 2022. Furthermore, RH expects to maintain its operating margin between 25-26%, essentially in line with Fiscal Year 2021, which was 25.6%.

This demonstrates that the firm is quite resilient despite the expected headwinds. In addition, the company has a measurable competitive advantage.

Competitive Advantage

There are a couple of ways to quantify a company’s competitive advantage using only its income statement. The first method involves calculating the earnings power value (EPV).

Earnings power value is measured as adjusted EBIT after tax, divided by the company’s weighted average cost of capital. The next step, finding the reproduction value (the cost to reproduce the business), can be measured using a company’s total asset value. If the earnings power value is higher than the reproduction value, then a company is considered to have a competitive advantage.

The calculation is as follows:

EPV = EPV adjusted earnings / WACC

$6,530 million = $542 million / 0.083

Since RH has a total asset value of $5,540 million, we can say that it does have a competitive advantage. In other words, assuming no growth for RH, it would require $5,540 million of assets to generate $6,530 million in value over time.

Another way to quantify a competitive advantage is by looking at a company’s gross margin because it represents the premium that consumers are willing to pay over the cost of a product or service. An expanding gross margin indicates that a sustainable competitive advantage is present.

If an existing company has no edge, then new entrants would gradually take away market share, leading to decreasing gross margins as pricing wars ensue to remain competitive.

Taking a look at RH, we can see that its gross margin has expanded in the past several years. As a result, its gross margin indicates that it has a competitive advantage.

Profitability

When looking at profitability, we like to focus on free cash flow rather than earnings. “Earnings” are paper profits that have the potential to be very misleading, which is why we look at FCF first.

Most financial specialists appear to be fixated on earnings. This is particularly true for institutional investors who tend to jump ship when they see the smallest profit miss.

In the last 12 months, RH has recorded $477 million in free cash flow, indicating that the company doesn’t have to rely on outside capital to continue funding its growth.

More importantly, its free cash flow has been trending up in recent years. Its FCF was $163.8 million just three years ago. To us, this means that the company’s free cash flows are reasonably predictable.

Efficiency

RH needs to hold onto a lot of inventory in order to keep the business running. Therefore, the speed at which inventory can be moved and converted into cash is an important factor in predicting its success.

To measure its efficiency, we will use the cash conversion cycle, which shows how many days it takes to convert inventory into cash. It is calculated as follows:

CCC = Days Inventory Outstanding + Days Sales Outstanding – Days Payables Outstanding

RH’s cash conversion cycle is 84 days, meaning it takes the company 84 days for it to convert its inventory into cash. In the past several years, this number has trended downwards from a peak of 156 days in 2017, indicating that the company’s efficiency has improved.

However, its cash conversion cycle is above the sector average of 32 days. Nevertheless, it doesn’t necessarily mean that RH is less efficient. Given that the company sells very high-end products, it’s only natural that it would take longer to move inventory when compared to businesses that sell to the average consumer.

Valuation

RH has seen a big pullback and valuation contraction. It is currently ~56% off its all-time highs. So, how does it look from a valuation standpoint now?

Analysts estimate that its EPS will drop 2% in Fiscal 2023 (ending January 2023) and grow 9.6% in 2024. This implies forward P/E multiples of 12.8 and 11.7, respectively.

Compared to high-multiple tech stocks, these P/E multiples look like a steal. However, RH’s sector typically tends to have much lower multiples due to its non-recurring revenue and cyclical nature. Therefore, this is something you have to consider.

When looking at RH’s peers, such as Williams-Sonoma (WSM) and Haverty Furniture Companies (HVT), who are trading at 9.2 and 6.3 times next year’s earnings, respectively, you can see that RH actually trades at a premium.

Nonetheless, RH has a solid history of growth and has more room to grow, as it has global expansion plans that can bolster growth for many years to come.

In the most recent earnings call, RH’s CEO stated: “Our plan to expand the RH ecosystem globally multiplies the market opportunity to $7 trillion to $10 trillion.” Needless to say, that’s a big market opportunity, and RH only needs a fraction of that to make loads of cash.

Although the valuation could be better, because of its growth potential, RH’s valuation is somewhat justified. For this reason, we have a small position in the stock at current levels.

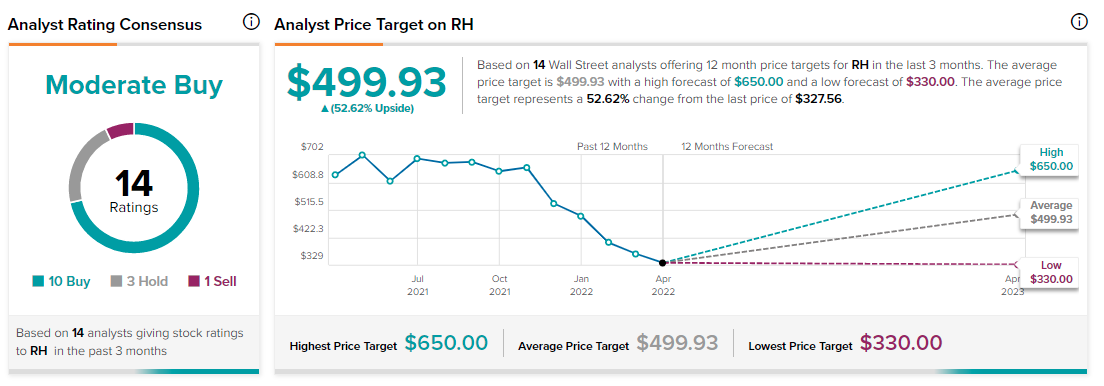

Wall Street’s Take

Turning to Wall Street, RH has a Moderate Buy consensus rating based on 10 Buys, three Holds, and one Sell rating assigned in the past three months. The average RH price target of $499.93 implies 52.6% upside potential.

Final Thoughts

RH is a strong business that is expected to be profitable despite the headwinds. In addition, analysts expect strong upside potential from here.

We are bullish on the stock, but because it is a bit more expensive than its peers, we only have a small position at the moment.

Discover new investment ideas with data you can trust.

Read full Disclaimer & Disclosure