August has proven to be a challenging month for stocks; however, the trend throughout this year has been bullish, with the S&P 500 rising 16%.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

According to RBC’s technical strategist Robert Sluymer, this upward trajectory is not a fleeting blip; rather, he views it as indicative of a prolonged secular bull market cycle – one that might lead the S&P to reach a peak near 14,000 in the mid-2030s.

Sluymer supports this perspective by closely examining the S&P’s cyclical pattern dating back to the Great Depression era. He highlights two periods of secular gains, lasting 16 to 18 years, in the 1950s and 1960s and in the 1990s and 2000s. These periods of gain were separated by periods of generally sideways movement. In Sluymer’s view, we’re now exiting a downtime, and the market is primed for a long-term surge.

“The long-term secular trend for US equity markets remains positive with an underlying 16 to 18 year cycle supportive of further upside,” Sluymer says in a recent note, and adds, “We recommend longer-term investors stay the course and remain optimistic about the evolving market cycle that bottomed in Q4.”

If the market is set to keep pushing forward, investors will be presented with more opportunities, and RBC analysts have an idea where those will manifest themselves best. Amongst their choices, they see two names that have the potential to double over the coming months. Let’s take a closer look.

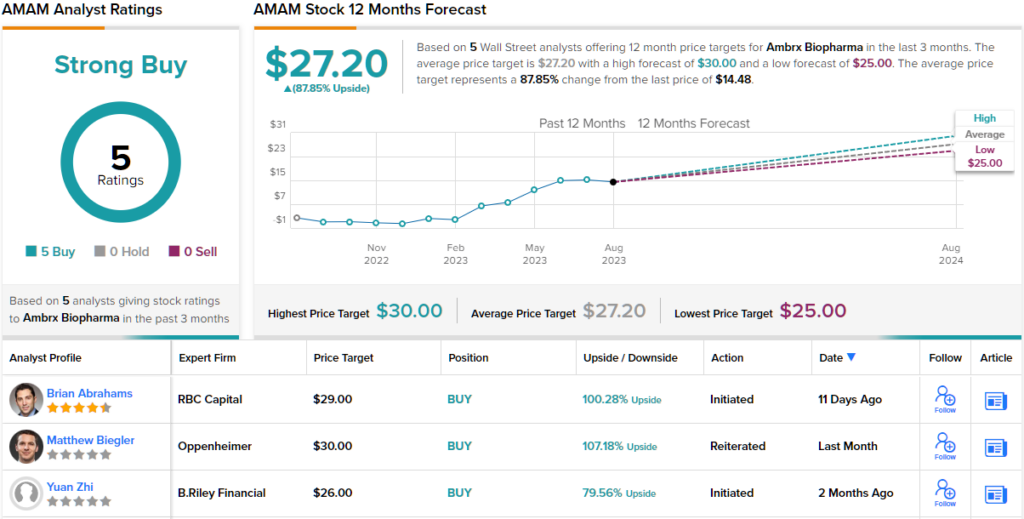

Ambrx Biopharma (AMAM)

We’ll start in the biopharmaceutical sector, where Ambrx is working with antibody-drug conjugates to develop precision-engineered biologics. The company’s research is focused on targeting various cancers, especially breast cancer and prostate cancer. By using antibody-drug conjugates, Ambrx aims to develop specific treatments against these targeted diseases while avoiding effects on healthy cells and tissues.

The company’s two leading drug candidates are worth a closer look. The more advanced of these, and the one farthest along in clinical trials, is ARX788. This antibody-drug conjugate (ADC) targets HER2 receptors and is being studied as a potential treatment for breast cancer, gastric GEJ cancer, and other solid tumors. The drug has been granted FDA Fast Track status for its study against HER2+ metastatic breast cancer and Orphan Drug status for gastric cancer. In March of this year, Ambrx announced positive results from the pivotal Phase 3 trial of ARX788 against HER2+ metastatic breast cancer, with the drug meeting the primary efficacy endpoint.

ARX517, the company’s other main research program, is in clinical investigation as a treatment for advanced prostate cancer. Prostate cancer is a serious condition with 1.4 million new cases annually and represents a significant unmet medical need. ARX517 is the subject of a Phase 1 clinical trial and recently received Fast Track designation from the FDA for the treatment of metastatic castration-resistant prostate cancer.

Covering Ambrx for RBC, 5-star analyst Brian Abrahams sees potential in both of these programs, noting, “We believe lead drug ARX517 has shown early promise in a potentially blockbuster metastatic castrate-resistant prostate cancer (mCRPC) space, and see meaningful upside potential on broader de-risking of ‘517 with the next data cut 4Q23. Additionally, we believe ARX788 may have underappreciated prospects as a differentiated Her2-targeted metastatic breast cancer (mBC) agent… While shares may no longer be completely under the radar, we see opportunity for add’l. appreciation…”

For Abrahams, this adds up to an Outperform (i.e. Buy) rating, and a price target of $29 to point toward a 100% upside potential for the year ahead. (To watch Abrahams’ track record, click here)

Overall, AMAM shares boast a Strong Buy consensus rating – and it is unanimous, based on 5 positive analyst reviews set in recent weeks. The shares are trading for $14.48 and the $27.20 average price target implies ~88% one-year gain from that level. (See Ambrx stock forecast)

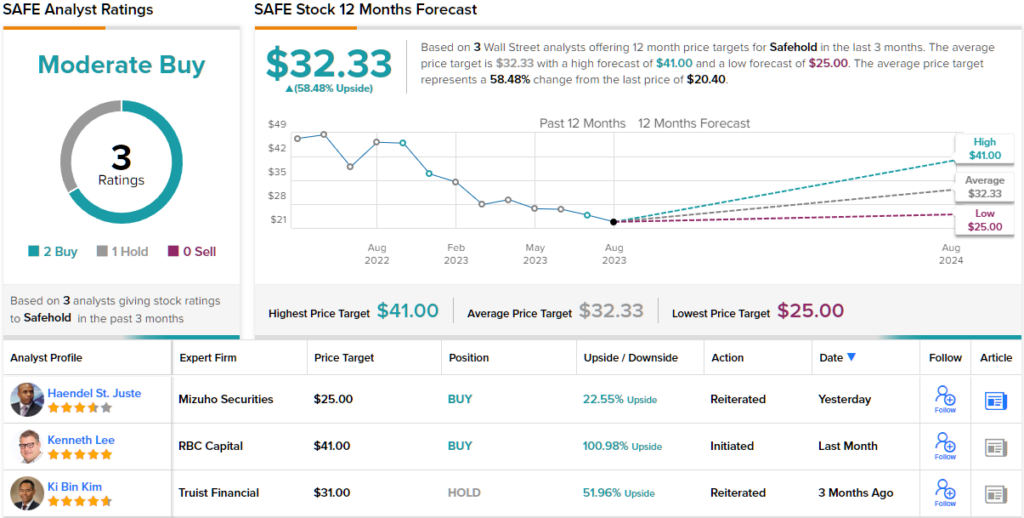

Safehold Inc. (SAFE)

Next up is Safehold, a unique company in the real estate investment trust landscape. Safehold offers its clients long-term ground leases as an alternative to simple fee purchases. Ground leases allow leaseholders to enter properties with smaller initial capital outlays and smaller loans, enabling them to concentrate on maximizing the lease’s potential. Long-term tenants in ground lease transactions have the right to build on properties, make improvements to the holdings, and realize gains from those improvements. However, these improvements revert to the landowner at the end of the lease agreement.

Safehold operates across the US, with a $6.2 billion ground lease portfolio in 30 leading US urban markets. These markets include high-growth areas such as Orlando, Atlanta, Nashville, Houston, Dallas, and Phoenix. The company’s portfolio comprises 14.9 million square feet of multifamily residential space, 13.2 million square feet of office space, as well as smaller ventures into hotels, life science spaces, and mixed-use properties. By the end of 2022, Safehold had completed over 130 ground lease transactions.

The first quarter of 2023 marked the completion of Safehold’s merger and consolidation with iStar, a substantial player in real estate finance and investment. The merger involved Safehold merging into iStar, resulting in iStar becoming the surviving corporation under the Safehold name. This merger, completed entirely in stock, took effect on March 31.

Fast-forwarding to more recent developments, Safehold reported its 2Q23 results just last week. The company’s revenue amounted to $85.7 million, marking a 32% year-over-year increase and surpassing forecasts by $2.35 million. On a non-GAAP basis, the bottom-line earnings were reported at 35 cents per share, matching the consensus estimate.

This year, many REITs have felt the effects of the rising interest rates in the U.S, and Safehold is not an exception. However, RBC’s top analyst, Kenneth Lee, sees the current headwinds creating a positive entry point for long-term investors.

“In our view, there could be long-term upside to shares from secular growth in the nascent ground lease market and recent merger with iStar may remove many structural hurdles for some investors in owning the stock. We believe sharply rising rates may have negatively impacted GL portfolio value, but if rates have peaked, this could be an attractive entry point for shares,” Lee opined.

Lee quantifies his stance with an Outperform (i.e. Buy) rating on SAFE, and his $41 price target implies a one-year gain of 101%. (To watch Lee’s track record, click here)

Looking at the consensus breakdown, 2 Buys and 1 Hold have been published in the last three months. Therefore, SAFE gets a Moderate Buy consensus rating. Based on the $32.33 average price target, shares could climb 58% higher in the next year. (See Safehold stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.