Once the bell rings to bring today’s market action to a close, Qualcomm (QCOM) will take its turn to deliver the quarter’s financials. The chip giant reports against a precarious back drop of weakening worldwide handset demand and geopolitical/recessionary worries impacting investor sentiment.

As such, Deutsche Bank analyst Ross Seymore does not see much potential for a beat-and-raise quarter. “With no clear signs of the Smartphone end-market demand improving and a rising probability of Android inventory issues continuing to push into 1H23,” said the 5-star analyst, “we believe QCOM’s recent track record of delivering solid print/guide will be put to a test in F4Q/F1Q.”

Nevertheless, boosted by its leading market position in the premium/high-end Android segment, a “seasonal” Apple phone ramp, and ongoing durability in diversified segments of Auto & IoT, Seymore anticipates Qualcomm will be able to “withstand the macroeconomic headwinds relatively better than rest of the Smartphone exposed semi peers.”

As for the September quarter (F4Q22) print, Seymore expects revenues to rise sequentially by 5% to $11.41 billion, roughly the same as consensus at $11.43 billion, and at the midpoint of Qualcomm’s forecast for $11.0-11.8 billion. At the other end of the scale, the analyst is calling for PF EPS of $3.15, also at the midpoint of the company’s $3.00-$3.30 guidance and more or less in-line with Wall Street’s $3.16 estimate.

For the outlook, Seymore’s F1Q23 (December quarter) forecast calls for total revenues of $11.77 billion, amounting to a 3% quarter-over-quarter uptick, but below the Street’s $12.09 billion forecast. Likewise for the bottom-line, Seymore sees PF EPS of $3.31, lower than consensus at $3.44.

However, Seymore sums up on a positive note, and highlights why investors should pay attention to this stock: “Overall, despite our very conservative estimates on the Smartphone/macro demand environment partially offsetting significant contribution from a full year of Apple & share gains at Samsung, we believe QCOM’s current valuation (~8-9x P/E), trading at a significant discount to its peers and its 5 yr P/E average remain attractive with multiple drivers of non-handset growth (PC, Auto, XR, 5G).”

Accordingly, the analyst maintains a Buy rating on QCOM shares, although the price target is lowered from $170 to $160, suggesting shares now have room for ~37% growth in the year ahead. (To watch Seymore’s track record, click here)

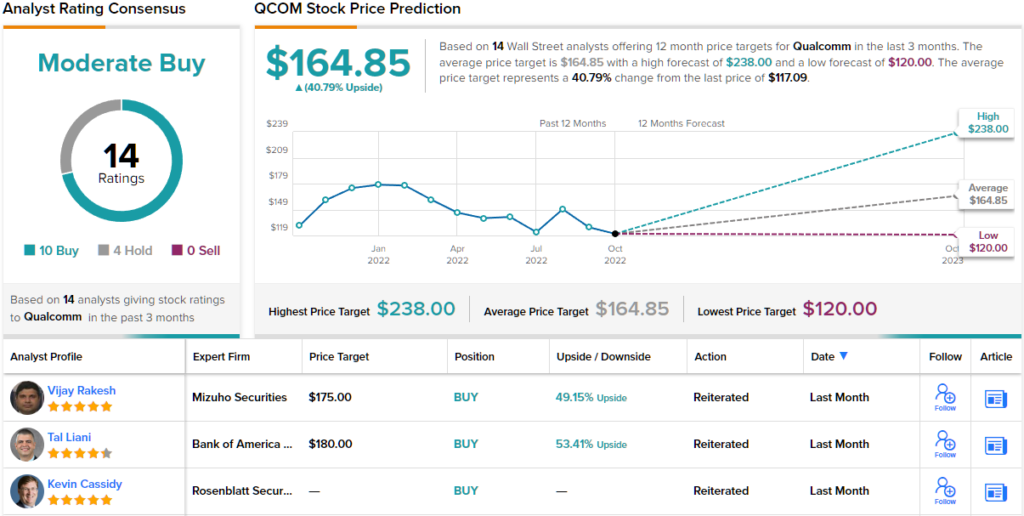

Looking at the consensus breakdown, based on 10 Buys vs. 4 Holds, QCOM stock makes do with a Moderate Buy consensus rating. Going by the $164.85 average target, the shares will climb ~41% higher over the coming months. (See Qualcomm stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.