Recently, Michael Aaron Zakuta, president and CEO of Plaza Retail REIT (TSE: PLZ.UN), has bought his company’s shares. Could this mean that the company is undervalued and has upside potential ahead? Possibly. Analysts also think that the stock is undervalued, and its valuation suggests the same. Additionally, the stock has a respectable 6.6% dividend yield. Therefore, it seems like a solid investment.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Plaza Retail REIT develops, owns, and manages retail real estate primarily in Atlantic Canada, Quebec, and Ontario.

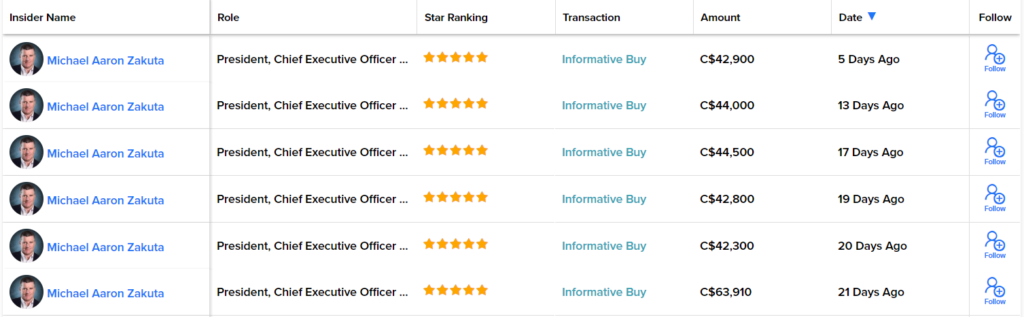

Zakuta’s recent buys are important to note for a few key reasons. First, he is a five-star-rated insider, ranked #231 out of 94,882 insiders on TipRanks, with an average return of 18% per transaction and a success rate of 76% (measured on a one-year basis).

Also, his transactions are classified as “Informative Buys,” which hold more weight than “Uninformative Buys.” His Buys usually come in chunks. He started buying 21 days ago, and his most recent purchase was five days ago.

The total amount bought was just over C$280,000. The recent buys ranged from prices of C$4.15 to C$4.51 per share, with the stock currently trading at C$4.24.

Interestingly, the last time Zakuta made purchases before this month was from May 11 to May 14, 2021, just before the stock saw a strong jump on May 25, 2021. Therefore, his actions should be followed closely by investors.

Is Plaza Retail REIT Undervalued?

It’s quite possible that PLZ.UN stock is undervalued, which would justify the insider buying. An important and easy valuation metric to use for Canadian REITs is the price-to-book ratio. Note that this metric isn’t as useful for American REITs due to accounting differences.

Plaza Retail REIT’s price-to-book ratio is around 0.85x, meaning that it’s trading at a discount to its net worth. This metric alone gives it about 18% upside potential before it reaches 1.0x, which happens to be the stock’s five-year average price-to-book multiple.

However, an important thing to note is that the company’s book value per share has stayed relatively flat over the past 10 years. Therefore, not much extra upside potential should be expected if the stock reaches its book value.

In addition, here’s what we mentioned in a recent article about a different REIT in a similar situation: “One thing to keep in mind is that its book value may potentially drop in the short term because rising interest rates are causing property values to fall, which somewhat justifies the discount. However, there is that margin of safety, and a drop is likely to be temporary in nature, in our opinion.”

Is Plaza Retail REITs Dividend Worth It?

As mentioned earlier, Plaza Retail REIT has a ~6.6% dividend yield that is paid monthly. This is a decent starting yield for risk-averse investors that are looking for consistent monthly returns. However, it isn’t the best for growth investors, especially since its dividend has grown at a compound annual growth rate (CAGR) of only 1% in the past five years.

Nonetheless, its dividend is covered, as its adjusted funds from operations (AFFO) payout ratio is 83% on a trailing-six-months basis.

Is PLZ.UN Stock a Buy or Sell?

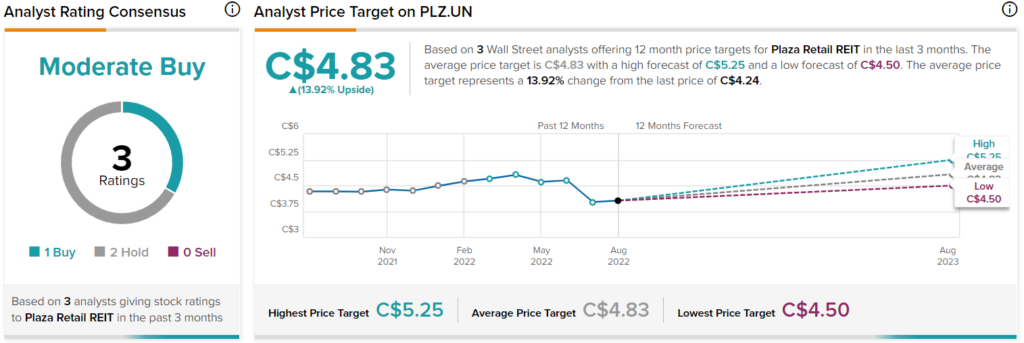

According to analysts, Plaza Retail REIT stock earns a Moderate Buy consensus rating based on one Buy and two Hold ratings assigned in the past three months. The average PLZ.UN stock price target of C$4.83 implies 13.9% upside potential. Analyst price targets range from a high of C$5.25 to a low of C$4.50.

Conclusion: Plaza Retail REIT Seems Like a Solid Play

Plaza Retail REIT has a few things going for it that make it look like an attractive investment. First, its high-rated CEO has been buying up shares at around current prices. Also, it’s trading for less than its net worth, implying about 18% upside potential in that regard. In the meantime, investors would be receiving a respectable 6.6% dividend yield. Finally, analysts expect close to 14% upside potential. While these aren’t mouth-watering numbers, they still make the stock worth looking into.