After being under pressure due to weak digital ad spending because of macro pressures, increasing competition from TikTok, and the impact of Apple’s (NASDAQ:AAPL) iOS privacy policy changes, social media companies showed strong signs of recovery in the third quarter. However, they warned of unpredictability in Q4 due to the war in the Middle East. With this backdrop in mind, we used TipRanks’ Stock Comparison Tool to place Pinterest (NYSE:PINS), Meta Platforms (NASDAQ:META), and Snap (NYSE:SNAP) against each other to find the most attractive social media stock, as per Wall Street analysts.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Pinterest (NYSE:PINS)

Shares of image-sharing app Pinterest rallied 19% on Tuesday after surpassing analysts’ revenue and earnings estimates for the third quarter. The company’s efforts to deepen engagement and grow monetization delivered the desired results, which reflected in the 8% rise in monthly active users to 482 million.

Revenue increased 11% year-over-year to $763 million, with the company crediting the growth to its “unique differentiators as a visual search, discovery, and shopping platform.” Further, Pinterest’s Q3 2023 adjusted earnings per share (EPS) surged to $0.28 from $0.11 in the prior-year quarter due to higher revenue and disciplined expense management.

Looking ahead, Pinterest expects revenue to rise in the range of 11% to 13% and adjusted operating expenses to decline in the range of 9% to 13%.

Pinterest is enhancing its platform with the deployment of artificial intelligence (AI). It is confident about delivering a mid to high-teens compound annual growth rate (CAGR) in its revenue and expanding its adjusted EBITDA margins to reach the low 30% range over the next three to five years.

Is Pinterest a Buy Now?

In reaction to the impressive Q3 results, Bank of America analyst Justin Post upgraded PINS stock to Buy from Hold and increased the price target to $37 from $32 on Tuesday. Post said that his growth outlook for the company is now “favorable” compared to other social networking rivals.

Other positives highlighted by the analyst included renewed confidence in the company’s new management team and better expense discipline than anticipated, which could drive additional upside in margins and EBITDA.

Also, Post noted that the beginning of the Amazon (NASDAQ:AMZN) deal ramp is getting closer, which is expected to further accelerate PINS’ growth in the first half of 2024. Earlier this year, Pinterest inked a multi-year deal with Amazon, under which the e-commerce giant will be its first partner on third-party ads.

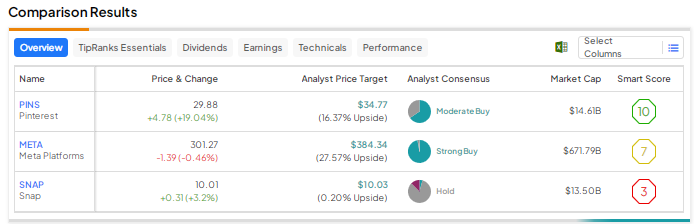

With 19 Buys and 10 Holds, Wall Street has a Moderate Buy consensus rating on Pinterest. The average price target of $34.77 implies 16.4% upside from current levels. Shares have advanced 23% year-to-date.

Meta Platforms (NASDAQ:META)

Last week, social media giant Meta Platforms reported market-crushing third-quarter results, with revenue rising 23% year-over-year to $34.1 billion. This marked a notable acceleration in revenue growth compared to 11% and 3% in Q2 and Q1, respectively, and reflected a solid recovery in digital ad spending.

Moreover, Q3 EPS jumped 168% year-over-year to $4.39, driven by the stellar rise in revenue and robust improvement in operating margin backed by productivity measures.

Despite solid numbers, META shares declined following its Q3 report as the company warned about softness in ad demand at the beginning of Q4 2023 due to the Israel-Hamas war. Also, the company cautioned about a meaningful increase in the Reality Labs division’s operating losses next year due to investments in augmented reality (AR) and virtual reality (VR) products and other strategic investments.

Is META a Buy, Sell, or Hold?

JPMorgan analyst Doug Anmuth explained that Meta shares sold off following Q3 earnings release due to management’s commentary about greater ad volatility in Q4 2023 owing to geopolitical issues. The analyst contends that while Meta’s Q4 revenue guidance is wider than usual due to the ongoing Israel-Hamas war, the high-end of the outlook is strong at $40 billion, which indicates mid-20’s% growth.

Anmuth believes that Meta has a solid product platform and plenty of investment opportunities across AI, Reels, Messaging, Threads, and Metaverse. Noting the company’s strong execution and cost discipline, Anmuth raised his price target for META stock to $420 from $400 and reiterated a Buy rating.

Overall, Meta earns Wall Street’s Strong Buy consensus rating based on 37 Buys and one Hold. At $384.34, the average price target implies 27.6% upside potential. Meta shares have rallied over 150% so far in 2023.

Snap (NYSE:SNAP)

Photo messaging app Snap returned to revenue growth in the third quarter, as the company enhanced its ad-targeting tools with AI. Revenue grew 5% year-over-year to $1.19 billion. The company’s GAAP loss per share increased to $0.23 from $0.22 in the prior-year quarter but was lower than analysts’ estimate of a loss per share of $0.24.

Like larger rival Meta, Snap also cautioned investors about the impact of geopolitical tensions on the fourth quarter. In particular, the company said that it noted pauses in spending from “a large number of primarily brand-oriented advertising campaigns” as soon as the war in the Middle East began.

While Snap did not issue formal guidance for Q4, it stated that its internal forecast implies revenue growth in the range of 2% to 6%.

What is the Target Price for Snap?

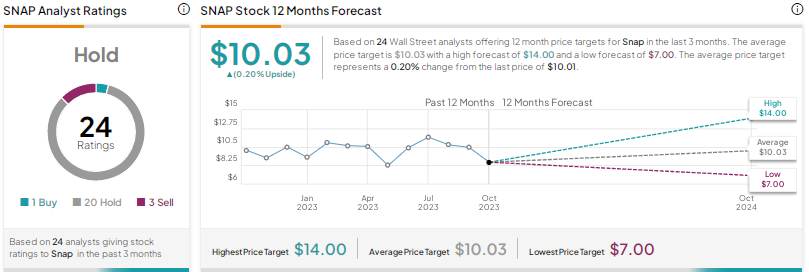

On October 25, Citigroup analyst Ronald Josey raised his revenue and EBITDA estimates for Q4 and 2024 but maintained a Hold rating on SNAP with a price target of $11.

Josey expects the company’s growth to continue to lag peers in Q4 2023. Further, he anticipates that margins will be pressured by the company’s generative AI investments. He added that a slowdown in user growth and growing competition from Instagram, Alphabet (NASDAQ:GOOGL)-owned YouTube’s Shorts, and TikTok might also drag down the stock.

Including Josey, 20 analysts have a Hold rating on Snap stock, while one has a Buy recommendation and three have a Sell rating. The average price target of $10.03 implies that the stock could be range-bound at current levels. Shares have risen about 12% year-to-date.

Conclusion

Wall Street is highly bullish on Meta Platforms due to its massive customer base, AI prospects, and focus on cost efficiency. Despite a solid year-to-date rally, analysts see higher upside potential in Meta stock than Pinterest and Snap.