Advertising stocks have been recovering. Meta Platforms (NASDAQ:META) stock has soared over the past year, with big rebounds in revenue and earnings growth. Alphabet (NASDAQ:GOOG) (NASDAQ:GOOGL) rebounded nicely, too. Still, both firms lost market share in 2022 and had multiple quarters that featured net income declines. META also reported revenue declines in 2022. However, one AdTech company, Perion (NASDAQ:PERI), thrived while others struggled back in 2022. The company is still growing now, which has prompted me to take a bullish stance on this stock.

This “stock to watch” even achieved double-digit revenue growth in 2023 while getting close to a 20% net profit margin.

High Growth, Low Valuation, and Zero Debt

Perion is a small-cap stock that offers a rare combination of growth, value, and fiscal strength. The company closed out the third quarter with a 17% year-over-year revenue increase. Perion operates in several high-growth advertising segments, such as connected TV and digital out-of-home advertising. Both segments are projected to achieve double-digit compounded growth rates over several years.

A sluggish 2023 stock performance has resulted in a compelling 9.5x forward P/E ratio and a 0.43 PEG ratio. The valuation gets even better when considering enterprise value instead of market cap. While Perion has a $1.38 billion market cap, the company only has an enterprise value of around $850 million.

There’s only one way for a company’s enterprise value to be less than its market cap. A corporation must have a cash position that is greater than its total debt. Perion has a 0% debt-to-equity ratio. The firm closed out the quarter with $197.8 million in cash and cash equivalents, along with $253.9 million in short-term bank deposits.

Perion is sitting on a lot of cash that it can use to acquire more advertising companies. The company recently acquired Hivestack for $100 million to improve its digital out-of-home advertising. Hivestack has many corporate clients who will now be introduced to Perion’s multi-channel advertising solutions.

This won’t be the last acquisition. Perion CEO Tal Jacobson mentioned in a press release that the company will continue to pursue additional acquisitions.

Why Perion Slumped in 2023

The growth rates, valuation, and lack of debt make Perion look compelling, but investors didn’t agree in 2023. The stock is down by 13% over the past year. Investors can appreciate the long-term potential of this stock by zooming out to the 795% gain over the past five years.

Perion’s slump wasn’t driven by financials or an excessive valuation. There are only two reasons I can think of that explain why Perion wasn’t a winner in 2023. The first reason is that Perion is based in Israel. Many corporations based in Israel saw their stock prices plunge at the start of the conflict. Perion’s stock price fell by almost 20% in October when the conflict started.

The second reason is the unfounded fear of Perion and Microsoft (NASDAQ:MSFT) breaking up. The partnership allows Perion to generate revenue through Bing’s search engine. The contract is set to expire this year.

Spruce Point Capital Management sounded the alarm of Perion’s “extreme dependency” on the contract. However, Perion has diversified into multiple revenue streams.

If the companies don’t come to an agreement, it’s definitely a setback for Perion. Microsoft makes up roughly 45% of Perion’s total revenue. However, it’s not a knockout blow by any means, especially with the low valuation. The stock is priced as if an agreement with Microsoft has already fallen through.

Furthermore, Perion and Microsoft have a good relationship that dates back to 2010. The company has agreed on new contracts multiple times while extending the length of each contract. The agreement in 2020 stretched for four years. The two companies had previously reached a three-year agreement in 2017.

Perion was named Microsoft Advertising’s 2021 Supply Partner of the Year, which indicates the relationship is still strong. A new agreement in 2024 and calming tensions in the Middle East can send Perion stock skyrocketing.

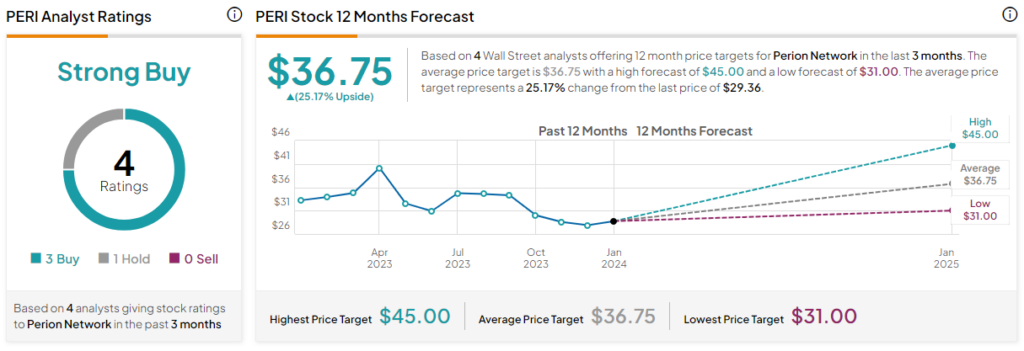

Is PERI Stock a Buy, According to Analysts?

Perion doesn’t receive as much coverage because it’s an under-the-radar stock. Among the four analysts who rated the stock, three of them rated it a Buy, while one analyst rated it a Hold, giving it a Strong Buy consensus rating.

Perion received a $45 price target from Oppenheimer in October 2023. That is the highest price target so far. The average PERI stock price target of $36.75 implies upside of 25.2% from the current price.

The Bottom Line on Perion Stock

Perion has the financials, growth verticals, and valuation to generate meaningful returns for long-term investors. Despite gaining market share while other advertising companies pulled back, Perion still trades at a 10x forward P/E ratio. Plus, the company continued to demonstrate robust financial performance, even though its stock price stayed flat.

The stock’s greatest weakness is its obscurity. However, investors are likely to bid up the price of this stock as it continues to report strong earnings growth. It’s baffling to see the stock down over the past year, but the underperformance offers an opportunity to buy shares before they potentially take off.