PayPal (NASDAQ:PYPL) has experienced the adverse effects of the 2022 stock market pullback spilling over into 2023 as well, with the stock currently trading at a huge discount (83%) compared to its all-time high a couple of years back. In a world of growing digital transactions, and considering the company’s otherwise strong financial performance, it seems like an attractive opportunity has come to light for investors. I am bullish on PYPL stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Used by over 400 million consumers and merchants around the world, PayPal enables digital payments by assisting consumers and merchants alike to manage and transfer money via its platforms. PayPal offers leading digital wallets, online checkout services, buy-now-pay-later capabilities, transaction processing, and merchant services. The company primarily earns its revenues by charging transaction payment fees. Some of PYPL’s popular services include PayPal (of course), Venmo, Xoom, Braintree, and others.

A Historic Dip for the Stock

A quick look at a longer-term price chart will immediately reveal how much PayPal’s stock has struggled over the past few years. In the trailing three-year period, the stock has lost 72.5% of its market cap despite the company recording strong financial performance. In the past year, PYPL’s stock price has retreated by 38.8%.

After an aggressive run-up for growth stocks following the spread of the COVID-19 pandemic in 2020, PYPL stock reached as high as $310.16. With valuations arguably being overly stretched and macroeconomics taking a turn for the worse in late 2021, PYPL (like most high-flying growth names) had a very rough 2022 and hasn’t been able to recover since.

While this huge drop in stock price seems to have largely corrected the stock’s overvaluation after the COVID-19 run-up, it also appears to have suppressed the stock price below reasonable levels as a result of overreaction in the market, introducing a high likelihood for a value opportunity at current price levels.

Latest Results Did Not Disappoint

For the second quarter of 2023, which represents the company’s latest quarterly filing, PayPal delivered revenue of $7.3 billion (7% increase) and total payment volume of $377 billion (11% increase). Meanwhile, non-GAAP EPS increased by 24% compared to Q2 2022.

PYPL maintains approximately 430 million active consumer accounts and 35 million active merchant accounts (recording, however, a 0.6% decline in active accounts), contributing to over 24 billion payment transactions in 200 markets globally.

Transactions per active account also increased by 12%. PayPal’s highly popular peer-to-peer (P2P) offerings (Venmo, Xoom, etc.) now represent 25% of total payment volume (Venmo’s TPV increased by 8%).

Further, on June 20, 2023, PayPal also announced an exclusive, long-term agreement for a €3 billion replenishing loan commitment under which private funds company KKR (NYSE:KKR) will purchase up to €40 billion of buy-now-pay-later (BNPL) loan receivables originated by PayPal in various countries in Europe.

PayPal’s BNPL offerings are also growing in popularity among customers (35 million BNPL customers) as they become a growing trend in the payment processing industry. They even help promote PYPL as a comprehensive services provider while increasing transaction volume.

Meanwhile, PayPal’s Q3-2023 results release is set for the beginning of November.

Profitability & Cash-Flow-Generating Capacity

Judging by PayPal’s operating and net margins, it could definitely be argued that the company exhibits decent profitability performance. For the second quarter of 2023, PYPL reported a non-GAAP operating margin of 21.4%, up 230 basis points compared to Q2 2022 (GAAP operating margin stands at 15.5%, up 430 basis points from Q2 2022)

On a trailing-12-month basis, the company generated $4.9 billion of free cash flow, keeping up with the firm’s record of strong cash flow generation over the past years.

PYPL has accumulated a $5.5 billion cash stockpile (as of the last filing) while demonstrating cash from operations that consistently surpasses net income for over a decade. This offers a bullish sign regarding the effectiveness of the company’s business model and operating efficiency. Margin expansion remains a priority for the business and also a key value-add factor, going forward.

Large Share Repurchases

Strong free cash flows and moderate capital expenditure requirements have allowed management to allocate excess cash toward share repurchase programs, aiming to enhance shareholders’ returns. PayPal’s share count has decreased by approximately 8% over the past three years, while the company expects to allocate $5 billion to buybacks for Fiscal Year 2023.

Beating Estimates Despite Cautious Sentiment

Despite overall cautious investor sentiment, evidenced by the stock price underperformance, over the past several quarters, PayPal has clearly demonstrated its ability to outperform financial expectations. PYPL has only missed estimates twice in the past eight quarters, indicating management’s ability to overdeliver even in the current challenging market environment.

Management guides for $5 billion in free cash flow for the 2023 Fiscal Year, while EPS growth is expected at 20%. Moreover, its operating margin is expected to widen by approximately 100 basis points.

Consumer Behavior and Slowing Transaction Volume Risks

PayPal’s business model performance relies heavily on strong consumer spending to generate high digital transaction volume. As the company’s revenues are derived from payment transaction fees, growth in the volume of payments (especially digital payments) is the most critical growth factor for the company. That is, especially as competition intensifies within the industry and transaction take-rates (fees charged) are facing downward pressure.

In this context, slowing consumer spending (leading to lower transaction volume) can be perceived as a short- and mid-term risk for the company. While the consumer sentiment index indicates that confidence has recovered from 2022 lows, it is still much lower than its 10-year historical average.

Can PYPL be Both a Growth and Value Opportunity?

Even as revenue growth has slowed over the past few years, analysts still expect the company to grow by high-single-digit percentages for the foreseeable future. For a fintech company that is entering its maturing phase and maintains strong margins and free cash flow capacity despite competitive pressures, the growth prospects going forward appear more than respectable.

At the same time, PayPal trades at a rather inexpensive valuation. PYPL’s 15.1x P/E ratio stands below the market average, seeming very reasonable for the stock. While PayPal trades at higher multiples compared to financial sector averages, it should be mentioned that both its business model and growth attributes contribute to the company being incomparable with large players in the financial sector (with the most prominent being banks).

A look at more comparable peers like Fiserv (NYSE:FI), which trades at a 24.2x P/E, or Block (NYSE:SQ), trading at a 31.7x P/E, further validates the valuation argument. For reference, mega-cap credit card companies like Visa (NYSE:V) and Mastercard (NYSE:MA) trade at P/Es around 30x.

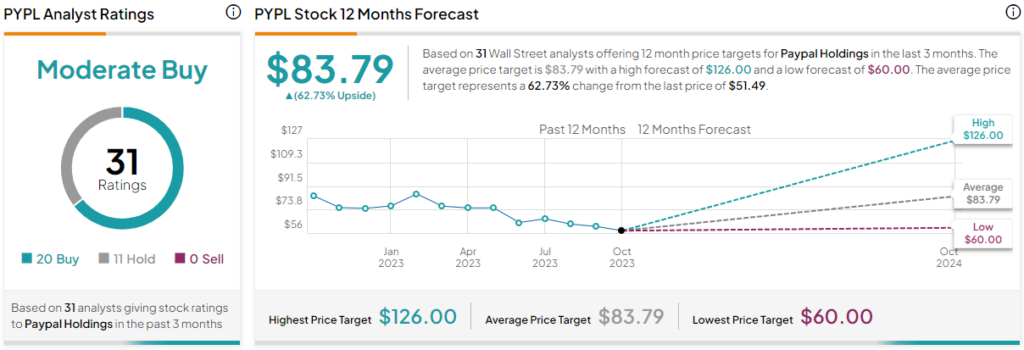

Is PYPL Stock a Buy, According to Analysts?

Turning to Wall Street, PYPL has a Moderate Buy consensus rating based on 20 Buys, 11 Holds, and zero Sell ratings assigned over the past three months. The average PYPL stock price forecast of $83.79 represents 62.7% upside potential, with a high forecast of $126.00 and a low forecast of $60.00.

The Takeaway

After all things are considered, despite its poor stock price performance over the past few years and some discernable risk factors regarding transaction volume and competition, PayPal is well-positioned to recover its gains and maintain a growth trajectory heading into the future. The company’s most desirable attributes include a leading market position, decent growth prospects ahead, profitability and cash flow capacity, as well as a rather reasonable valuation.